Your RV is more than a vehicle-it’s your home on wheels. Standard insurance policies treat all RVs the same, which means you’re either overpaying for coverage you don’t need or missing protection for what matters most.

At Leslie Kay’s, Inc., we believe your insurance should match how you actually travel. A customizable RV insurance policy adapts to your lifestyle, whether you’re a full-timer exploring year-round or a seasonal adventurer hitting the road on weekends.

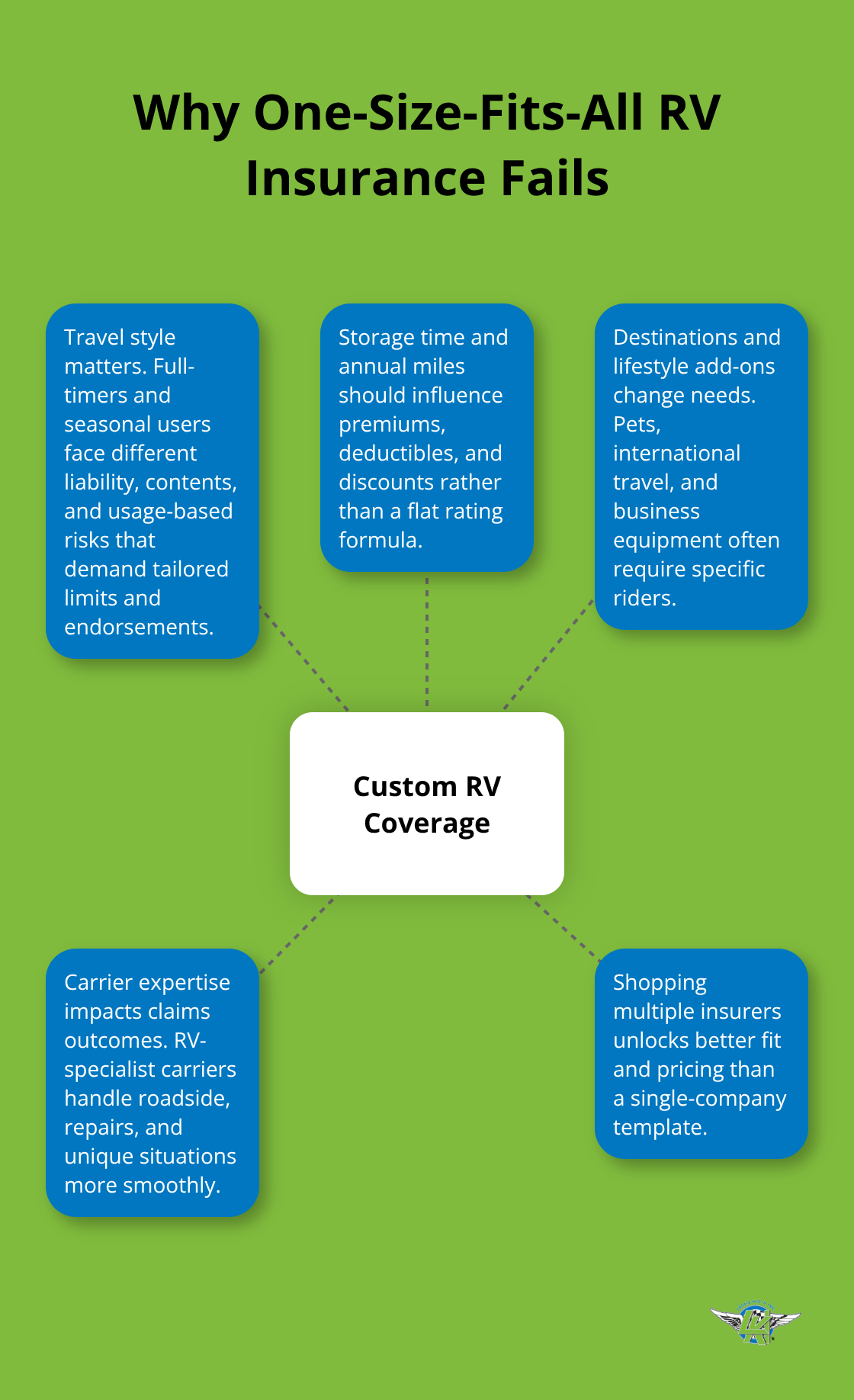

Why Standard RV Insurance Falls Short for Modern Travelers

The RV industry has exploded in recent years. RV shipments reached 430,000 units in 2023, according to the RV Industry Association. Yet most insurance carriers still rely on outdated templates designed decades ago when RV ownership looked completely different. A full-timer living year-round in their motorhome faces entirely different risks than someone who parks their travel trailer in storage nine months per year. Standard policies ignore these distinctions and force you into coverage that either wastes money or leaves dangerous gaps. The problem isn’t that standard policies are bad-it’s that they treat a weekend warrior and a nomadic adventurer identically, which makes no sense.

You end up paying for protections you’ll never use or missing coverage for scenarios you actually face.

Where Standard Policies Leave You Exposed

Most standard RV policies cover the basics: liability, collision, and comprehensive. What they typically miss are the realities of your specific travel style. If you full-time, you need expanded liability coverage because your RV is your primary residence-campsite associations can sue you for injuries on your property. If you travel seasonally, you pay for year-round coverage while your RV sits dormant. Personal belongings inside your RV rarely receive adequate coverage limits under standard policies. A laptop, drone, or high-end camera equipment might exceed the policy’s contents limit by thousands of dollars. Vacation liability coverage, which protects you if someone gets injured at your campsite while you’re parked, isn’t automatically included. Permanent attachments like awnings, satellite dishes, and antennas need separate coverage that standard policies often overlook. Water damage from sudden events receives coverage, but gradual leaks or delamination don’t-yet these rank among the most expensive RV repairs.

How Standard Rating Formulas Miss Your Reality

Insurance carriers use standard rating formulas that don’t account for how you actually use your RV. Someone who travels 50 days per year has different accident risk than someone who travels 200 days per year, but standard policies charge similar rates. Storage discounts exist with most carriers, but you have to know to ask for them. Full-timers often qualify for accident forgiveness coverage, which prevents rate increases after your first at-fault accident, yet carriers won’t volunteer this option. The real issue is that carriers profit from one-size-fits-all approaches-they require minimal underwriting and can process policies quickly without understanding your lifestyle. Your coverage should reflect whether you explore Mexico, stay within the continental United States, travel with pets that need medical coverage, or live in your RV as your primary address. Standard policies make you fit their template; customizable policies fit your life. This is where carriers that shop multiple insurers (rather than pushing their own limited options) make all the difference in finding protection that actually matches your travel patterns.

What Coverage Actually Changes Between Full-Timers and Seasonal Travelers

Full-Timer Liability and Loss Assessment Needs

Full-time RV living and seasonal travel demand fundamentally different insurance structures, yet most carriers treat them identically. A full-timer living year-round in a motorhome needs full-timer’s liability coverage, which protects against injuries or property damage claims from people on or near your property. Campsite associations frequently pursue liability claims when someone gets injured on the grounds where your RV is parked, making this coverage non-negotiable for permanent residents. You also need loss assessment coverage, which shields you from unexpected bills if the RV park or campground association faces a lawsuit.

Personal Belongings Coverage Limits Matter Most

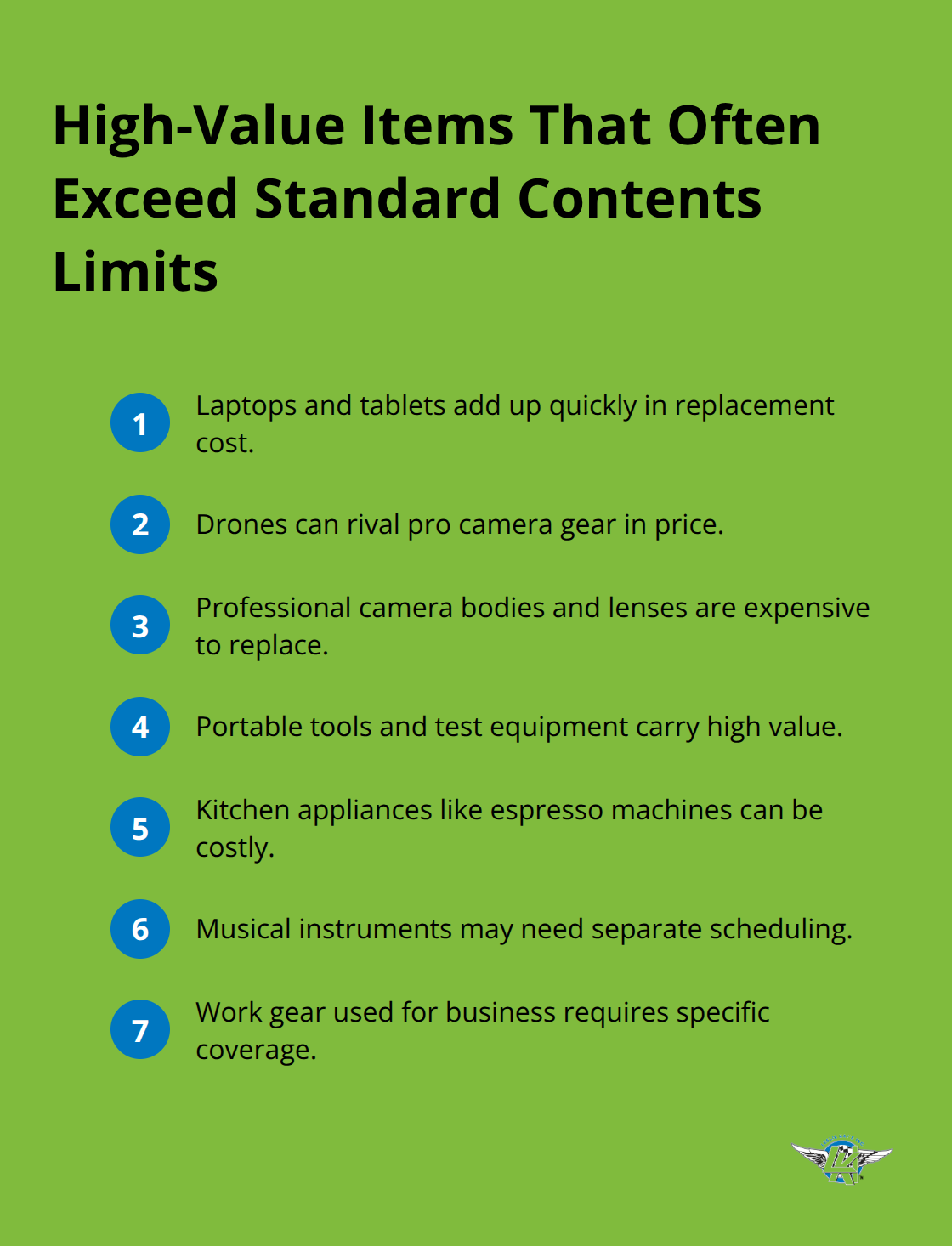

Personal effects coverage becomes critical because full-timers keep thousands of dollars in belongings inside their RV-electronics, clothing, tools, kitchen equipment. A standard policy might cap contents coverage at $1,500 to $2,500, leaving you exposed if a fire destroys your possessions. Electronics like laptops, drones, tablets, and cameras accumulate quickly for full-timers and frequently exceed standard policy limits. Many carriers cap personal effects replacement at $2,500 to $3,000, yet a single drone costs $1,000 to $2,500 and a quality camera setup runs $2,000 to $5,000.

Request specific coverage limits for high-value items and confirm whether your policy covers items used for work, since remote workers traveling full-time in RVs need business equipment protection.

Seasonal Travelers Prioritize Storage and Vacation Liability

Seasonal travelers should prioritize storage discounts since their RV sits unused for months. Many carriers offer discounts specifically for RVs in storage during off-season months, potentially reducing your premium by 10 to 15 percent if you’re not traveling November through March. Vacation liability coverage matters more for seasonal users who park at different campsites throughout the year, protecting you if a guest injures themselves at your campsite while you’re stationary. Permanent attachments like awnings, satellite dishes, and roof-mounted antennas need dedicated coverage under both scenarios, but full-timers face higher replacement costs since these fixtures withstand constant use and weather exposure.

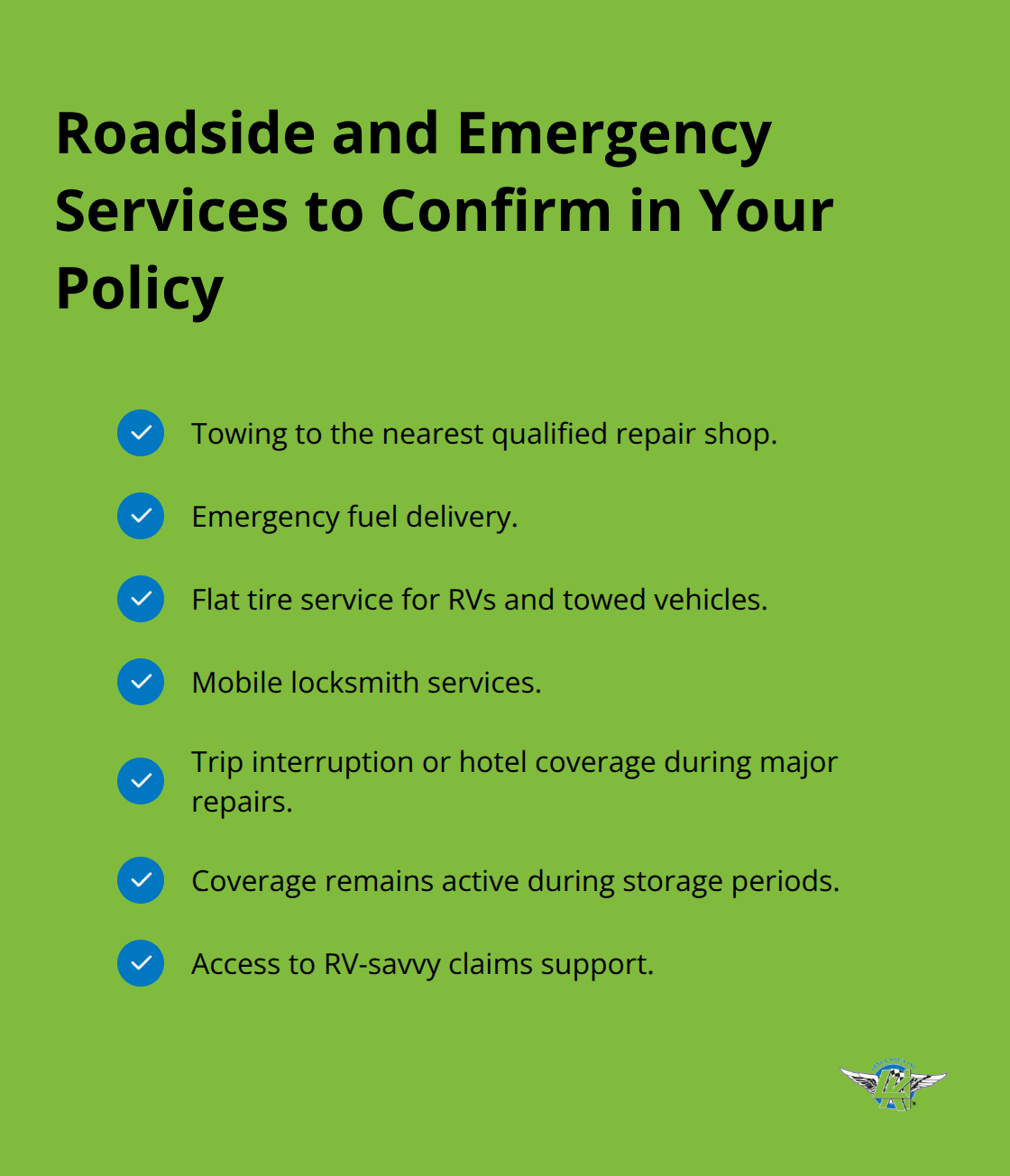

Roadside Assistance and Emergency Services

Roadside assistance and emergency services separate quality carriers from basic ones. Mechanical breakdown insurance covers unexpected failures, while specialty RV insurers handle the unique demands of roadside emergencies. Flat tire repairs, engine failures, and fuel delivery costs accumulate rapidly when you’re stranded hours from a repair facility. Confirm whether roadside coverage includes towing to the nearest repair shop (not just to a home address), emergency fuel delivery, and locksmith services. For full-timers especially, emergency accommodation coverage that pays for hotel stays while your RV undergoes major repairs protects your lifestyle continuity. Seasonal travelers should verify that coverage remains active during storage periods, since theft and weather damage don’t stop when you’re not traveling.

The distinctions between full-timer and seasonal coverage reveal why shopping multiple carriers matters. Each insurer weights these protections differently, and finding the right match requires an agency that understands both travel styles and can compare options across the market.

How We Build Policies That Actually Fit Your Travel Style

We at Leslie Kay’s, Inc. approach RV insurance differently than carriers locked into their own limited templates. Most insurance companies force you to accept what they offer, but we shop multiple carriers to find the specific protections that match your lifestyle. When you call or request a quote, you’re not getting pushed toward one company’s standard policy-you’re getting access to options from specialty RV insurers who understand the difference between a full-timer’s needs and a weekend traveler’s coverage.

Multiple Carriers Give You Real Choices

GEICO offers specialized RV coverages including Pest Shield Coverage and Roof Advantage Coverage for motorhomes under six years old, which pays to repair or replace a roof for weather-related damage with a $250 deductible. Progressive frequently appears in RV community discussions as another option worth comparing. Good Sam Insurance Agency represents multiple insurers in the National General Group, shopping a network of specialty RV carriers to find competitive rates. We at Leslie Kay’s, Inc. compare these options against your actual travel patterns, not to fit you into whoever pays the highest commission. A full-timer needs different carrier expertise than someone parking seasonally, and the wrong carrier choice leaves you exposed when you file a claim.

Understanding RV-Specific Risks

Our advisors understand the specific risks that generic insurance agents miss because they’ve worked with thousands of RV owners and seen where claims actually fail. When comprehensive coverage excludes gradual wear, delamination, and mold-which it does across most carriers-you need an advisor who explains this gap upfront and helps you plan for maintenance. Mechanical breakdown insurance becomes critical if your motorhome’s engine fails at 80,000 miles, yet most standard auto policies won’t touch it. We help you identify which coverage additions matter most for your budget and travel frequency.

Permanent attachments coverage protects awnings, satellite dishes, and antennas that can cost $2,000 to $5,000 to replace after storm damage. Personal effects replacement coverage should match your actual belongings-if you carry $8,000 in electronics and tools, a $2,500 limit is worthless. We work with carriers offering full replacement cost coverage that reimburses you to replace your RV if totaled or stolen within the first five model years, which protects your investment far better than actual cash value policies that depreciate rapidly.

Support When You Need It Most

Our seven-day-a-week support means when you’re stranded in an unfamiliar state with a mechanical failure or accident, you reach someone who knows your specific policy, not a call center reading a script. We handle claims support and help you navigate what’s covered versus what falls under maintenance responsibility, which saves thousands in disputes with carriers who deny claims based on technicalities.

Final Thoughts

Your RV represents a significant investment and a lifestyle choice that demands protection matching your actual travel patterns. A customizable RV insurance policy isn’t optional-it’s the only approach that makes financial sense when your needs differ fundamentally from other RV owners. Full-timers, seasonal travelers, and weekend adventurers face completely different risks, yet standard policies charge similar rates while leaving critical gaps.

The right policy covers the specific scenarios you’ll actually face, whether that’s loss assessment claims from campground associations, personal belongings worth thousands of dollars, or mechanical failures that strand you hours from home. It includes coverage additions that matter for your travel frequency and destinations, not the ones that pad an insurer’s profit margins. It reflects whether you explore Mexico, travel year-round, or park seasonally.

We at Leslie Kay’s, Inc. shop multiple carriers to find the specific combination of coverages that matches your lifestyle and budget. Contact us today to explore how a customizable RV insurance policy protects what matters most.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.