RV ownership opens up freedom on the road, but insurance costs can quickly eat into your budget. At Leslie Kay’s, Inc., we know that finding cheap RV insurance online doesn’t mean sacrificing the protection you need.

This guide walks you through proven strategies to cut your premiums while keeping solid coverage in place.

Finding the Best RV Insurance Quotes Online

Shopping for RV insurance online puts you in control of your costs, but only if you approach it strategically. RV insurance costs $200 to $3,500+/yr in 2026, though you can find coverage as low as $125 per year for liability-only policies or around $594 per year for travel trailers and $1,052 for motorhomes, according to Progressive data. The wide range exists because insurers price policies differently based on your RV type, driving history, location, and coverage selections.

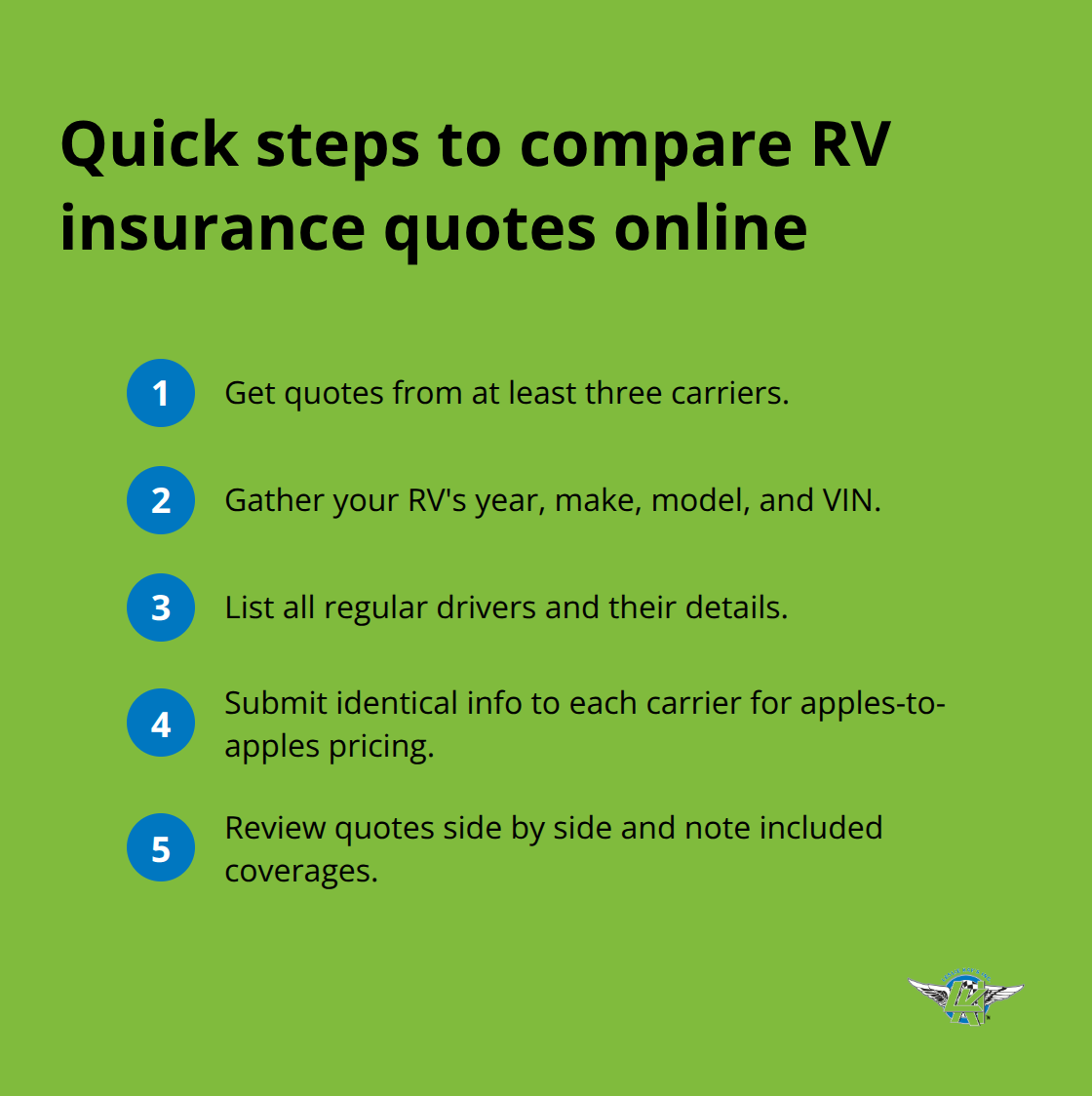

Compare Quotes from Multiple Carriers

Start with quotes from at least three different carriers-Progressive, Foremost, and Safeco are major players in the RV market. When you request a quote online, have your RV’s year, make, model, and VIN ready, plus information about all drivers who regularly operate the vehicle. This speeds up the process and produces accurate pricing.

Most insurers deliver quotes within minutes, allowing you to compare recreational vehicle insurance rates from multiple providers without leaving your home.

Stack Discounts to Cut Your Premium

Discounts represent the fastest way to lower what you pay, and insurers stack them generously. Multi-policy bundling-combining your RV, auto, and home insurance with one carrier-typically saves around 5% on your auto policy alone, with additional savings on the RV coverage itself. Paying your full annual premium upfront rather than monthly installments often qualifies you for a paid-in-full discount. A clean driving record covering the past three years without tickets or accidents qualifies you for safe-driver discounts with most carriers. If your RV has factory-installed anti-lock braking systems (ABS), mention this when quoting; some insurers reward this safety feature. Original owner status sometimes qualifies for discounts as well. Ask directly about every available discount during your quote process-agents won’t always volunteer them unless you ask.

Adjust Deductibles and Coverage Limits Strategically

Your deductible choice dramatically impacts your monthly or annual cost. Raising your deductible from $500 to $1,000 typically reduces premiums by 15-25%, depending on the insurer and your location. However, only increase your deductible if you can comfortably pay that amount out of pocket after an accident-otherwise you shift risk rather than manage it. Coverage limits matter equally. Liability coverage protects others if you cause injury or property damage; most states mandate minimum limits, but these minimums rarely match the actual cost of a serious accident. Comprehensive and collision coverage protects your RV itself. Travel trailers require comprehensive and collision regardless of whether you’ve financed them, while motorhomes follow auto-insurance logic with these coverages becoming optional if paid in full. Personal property coverage inside your RV is separate; if you carry expensive electronics, cameras, or tools, match your personal effects limit to their actual value. Skip optional add-ons like total loss replacement, roof protection, and vacation liability initially-you can add them later if needed-but never skip liability, which is legally required for motorhomes in nearly every state.

Know When to Add Optional Coverages

Once you’ve locked in your core coverage, consider which optional add-ons fit your situation. Emergency expenses coverage pays for lodging, food, and rental cars if your RV becomes unusable on the road, reducing disruption costs significantly. Pet injury coverage reimburses veterinary costs if a pet is injured in an RV incident, offering extra family peace of mind. Vacation liability provides additional protection if someone is injured at your RV site, especially when camping or staying at parks. Total loss replacement can replace a totaled RV with a similar model, which may be worth the extra premium for newer or higher-value RVs. Roof protection covers roof damage from wear, tear, or malfunctions and proves valuable for older or frequently used RVs. These additions cost more upfront but address real gaps in standard policies-the decision depends on your travel frequency and the value of what you carry.

Your coverage choices directly shape what happens next: understanding how your RV type, usage patterns, and driving record influence your final premium.

What Costs More to Insure: Your RV Type or How You Use It?

RV Type Sets Your Baseline Premium

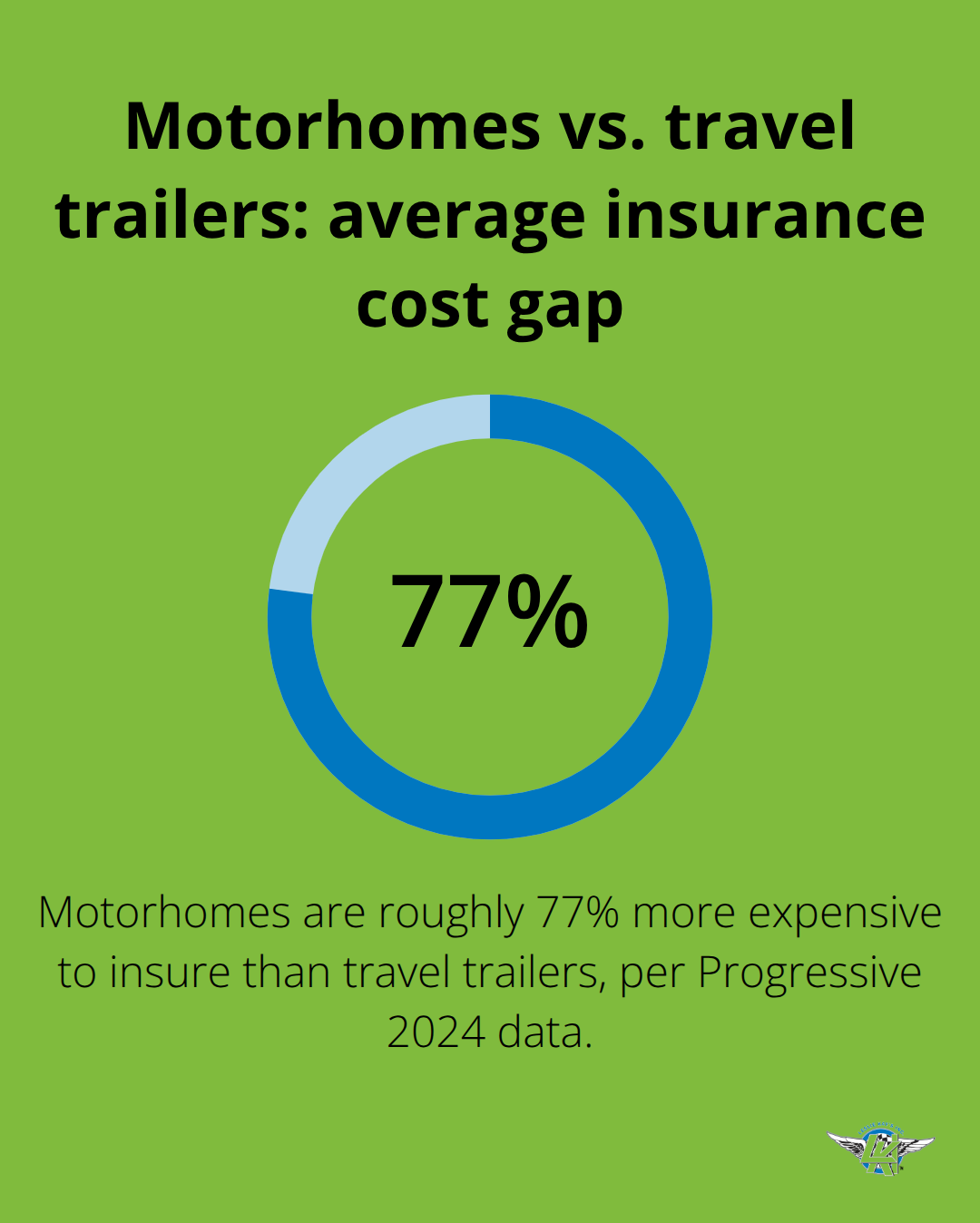

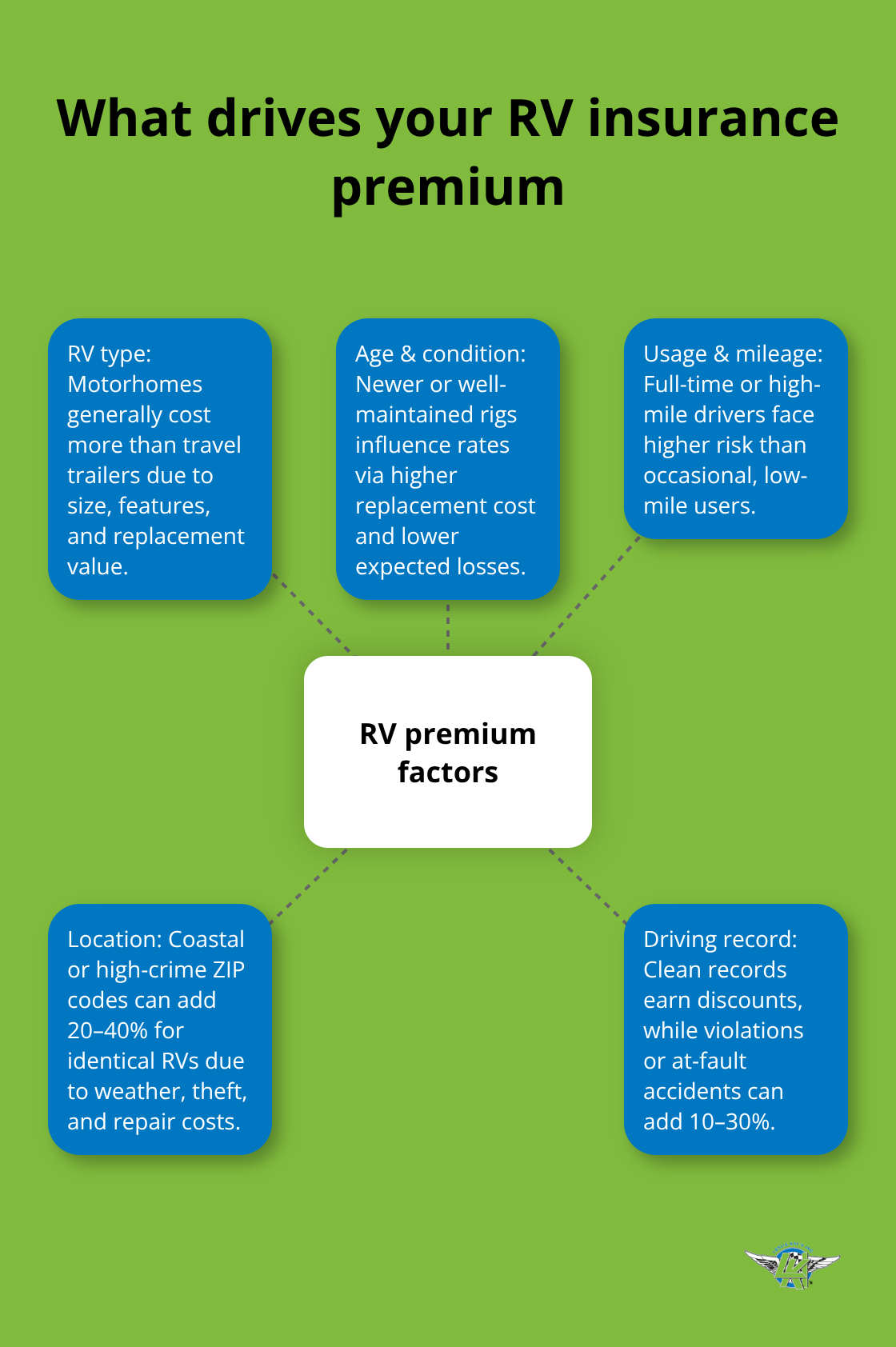

Your RV’s category determines the baseline cost, and motorhomes cost significantly more than travel trailers. According to Progressive data from 2024, travel trailers average around $594 per year while motorhomes run about $1,052 annually, making motorhomes roughly 77% more expensive to insure.

Class A motorhomes push costs even higher due to their size, luxury features, and replacement value. A brand-new Class A motorhome worth $200,000 will cost far more to insure than a used travel trailer worth $35,000, simply because replacing it after a total loss would devastate your finances.

Age and Condition Impact What You Pay

The RV’s age matters equally. Newer RVs command higher premiums because their replacement cost is higher, but they often include factory safety features that qualify for discounts. Older RVs sometimes cost less to insure monthly, but if your lender financed the purchase, you’ll still need comprehensive and collision coverage, eliminating the savings advantage. RV condition also influences pricing. A well-maintained five-year-old motorhome with no water damage or structural issues costs less to insure than a neglected model of the same age, though insurers rarely ask directly about maintenance history during quoting. Instead, they assess risk through the vehicle’s age, mileage, and claims history associated with that specific RV.

Usage Frequency and Location Reshape Your Premium

How frequently you use your RV and where you travel reshape your premium dramatically. Full-time RV residents who live in their motorhome or travel trailer annually need specialized full-time RV insurance that includes optional coverages providing protection if you use your RV as your permanent residence, pushing premiums higher than recreational-use policies. Part-time users who spend 30 days per year in their RV pay substantially less because the vehicle spends most of its time parked safely at home. Mileage matters too. An RV driven 2,000 miles annually faces far lower accident risk than one driven 15,000 miles yearly, and insurers factor this directly into pricing.

Your location determines whether you face severe weather, high theft risk, or expensive repair costs in your region. Coastal areas and high-crime ZIP codes typically cost 20–40% more than rural regions for identical RVs.

Driving Record: Your Most Controllable Cost Factor

Your driving record remains the single most controllable cost factor. Three years without accidents or tickets qualifies you for safe-driver discounts with most carriers, while even one at-fault accident or ticket can increase your premium by 10–30% depending on severity. A DUI conviction will spike your rates dramatically or result in outright denial from some insurers. If you’ve filed multiple claims in the past five years, expect higher premiums regardless of who was at fault, since insurers view frequent claimants as higher risk.

These cost drivers interact constantly-a newer motorhome in a high-risk ZIP code with a spotty driving record will cost substantially more than an older travel trailer in a rural area with a clean record. Understanding which factors you control and which you don’t shapes your next move: selecting the right coverage strategy for your specific situation.

Concrete Steps to Cut Your RV Insurance Costs

Safety upgrades and smart payment strategies deliver the fastest premium reductions available to RV owners right now. Installing factory-standard or aftermarket safety features directly lowers what insurers charge because these modifications reduce accident risk and claim severity. Anti-lock braking systems rank first on insurer priority lists-mention ABS during your quote if your RV has it factory-installed, as many carriers offer discounts for this single feature. Backup cameras, collision avoidance systems, and tire pressure monitoring systems also qualify for discounts with Progressive and other major carriers, though discount amounts vary by insurer and state. GPS tracking systems appeal to insurers because they aid in theft recovery; some carriers offer 10-15% reductions when you install one. The investment in these features typically pays for itself within two to three years through premium savings alone, especially if you’re insuring a motorhome that might cost $1,052 annually according to Progressive data.

Complete an RV Safety Course

RV safety courses represent another direct path to lower premiums without spending thousands on equipment. Completing an accredited RV safety course qualifies you for driver-training discounts with most carriers, typically reducing your premium by 5-10%. The Recreational Vehicle Safety Institute and similar organizations offer online courses covering RV-specific hazards like weight distribution, brake management, and backing techniques-skills that demonstrably reduce accident rates. A $100-150 course investment pays dividends immediately on your renewal.

Choose Your Payment Method Strategically

Payment method choices reshape your costs dramatically. Paying your full annual premium upfront rather than monthly installments qualifies you for paid-in-full discounts that range from 3-8% depending on your carrier, effectively returning $15-80 annually on a $1,000 policy. If upfront payment strains your budget, increasing your deductible from $500 to $1,000 typically reduces your annual premium by 15-25%, according to industry standards. The math works only if you maintain an emergency fund covering your deductible-raising it to $2,500 might save 30-40% but becomes reckless if an accident would force you into debt.

Combine Multiple Strategies for Maximum Savings

These three levers-safety installations, formal training, and strategic payment or deductible choices-address the cost problem directly without reducing actual protection when applied correctly. A motorhome owner who installs a GPS tracker (10-15% savings), completes a safety course (5-10% savings), and pays annually (3-8% savings) can stack discounts to achieve 18-33% total reductions on their premium, transforming a $1,052 annual cost into roughly $700-860.

Final Thoughts

Finding cheap RV insurance online comes down to three interconnected decisions: comparing quotes across carriers, stacking discounts strategically, and choosing coverage that matches your actual risk. Installing safety features like GPS trackers or ABS systems, completing an RV safety course, and paying your premium annually or adjusting your deductible can combine to reduce your costs by 18-33% without sacrificing protection. A motorhome owner paying $1,052 annually can realistically reach $700-860 through these concrete actions.

Cutting costs only matters if your coverage actually protects you when something goes wrong. Liability coverage remains non-negotiable because it’s legally required for motorhomes in nearly every state and protects your personal assets if you cause injury or property damage. Comprehensive and collision coverage protect your RV itself, especially critical if you’ve financed the purchase or own a newer model with high replacement value. Personal property coverage inside your RV should match the actual value of electronics, tools, and belongings you carry.

The balance between affordability and adequate protection isn’t a compromise-it’s the entire point. Skipping liability coverage to save $50 annually exposes you to financial ruin if an accident occurs. We at Leslie Kay’s, Inc. specialize in helping RV owners find this balance by shopping multiple carriers to deliver customized policies at competitive prices, with hands-on claims support and seven-day-a-week service. Contact us to compare quotes and lock in coverage that protects your RV and your finances without unnecessary expense.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.