Your standard auto insurance policy won’t protect your ATV. Most carriers exclude off-road vehicles entirely, leaving you exposed to serious financial risk.

At Leslie Kay’s, Inc., we know that a custom ATV insurance policy designed for your specific riding needs makes all the difference. This guide shows you exactly what coverage matters and how to find the right protection for your lifestyle.

Why Standard Auto Insurance Won’t Cover Your ATV

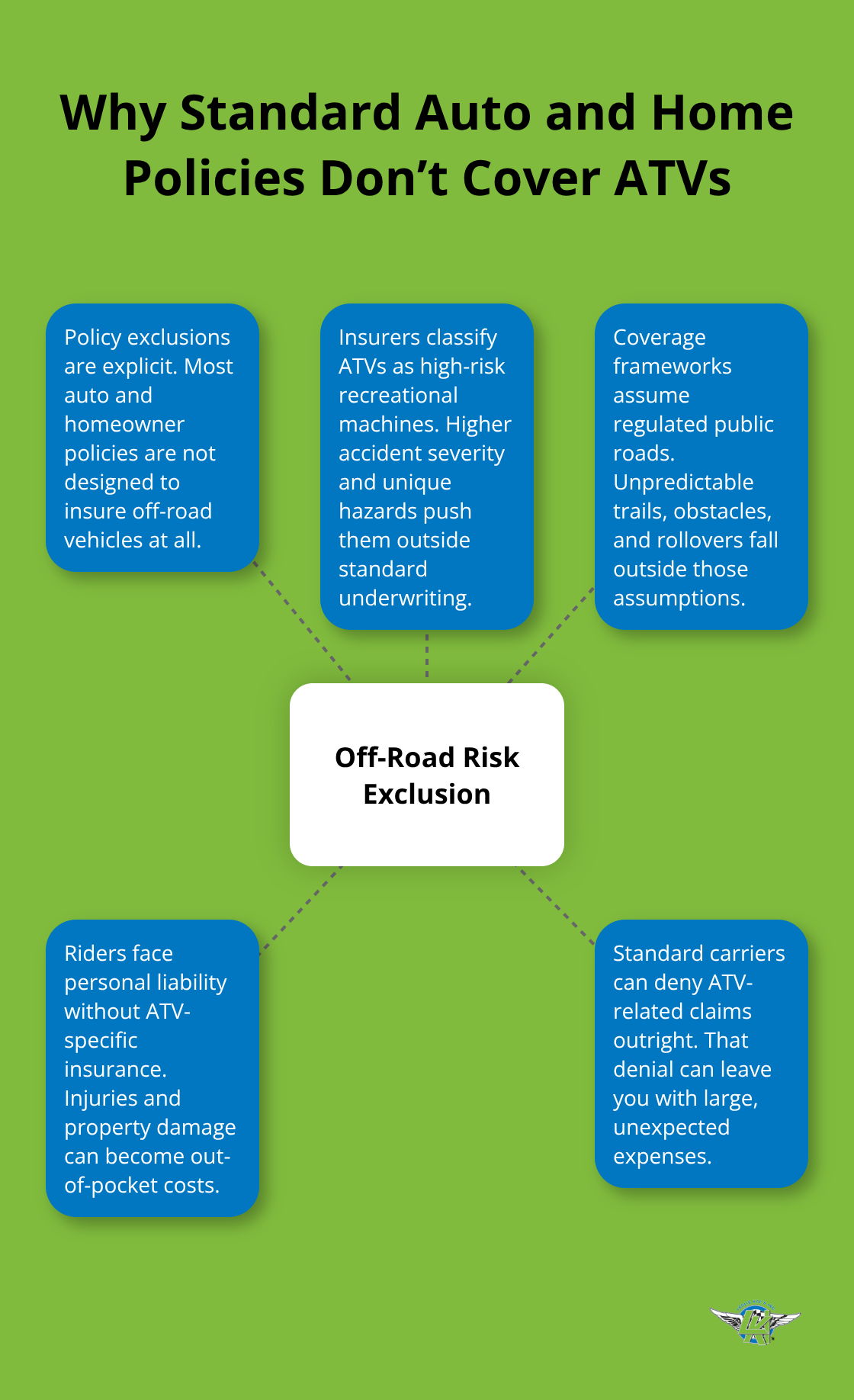

Auto and Homeowner Policies Exclude Off-Road Vehicles

Your homeowner’s or auto insurance policy almost certainly excludes ATVs entirely. This isn’t an oversight-it’s deliberate. Standard carriers classify ATVs as high-risk recreational vehicles and refuse to cover them under policies designed for street-legal vehicles.

The U.S. Consumer Product Safety Commission reported ATV injuries that explain why insurers treat off-road riding as a separate risk category. When you ride without proper ATV insurance, you become personally liable for any injuries, medical bills, or property damage you cause. A single accident could cost tens of thousands in medical expenses or property claims-and your standard policy will deny the claim outright.

Off-Road Activities Fall Outside Standard Coverage Terms

Most general liability policies explicitly exclude recreational off-road use. Your auto insurance covers you on public roads with safety regulations, traffic laws, and predictable conditions. ATV riding happens on unpredictable terrain with different hazard profiles. Rollovers, collisions with obstacles, and falls occur regularly in off-road environments that standard auto underwriters won’t touch. If you cause an accident and your insurer discovers you were riding an ATV, they can deny your claim and potentially cancel your entire policy. This creates a dangerous gap where riders think they’re protected but actually have zero coverage when they need it most.

Custom Equipment and Modifications Require Separate Protection

Standard policies don’t cover ATV-specific equipment or aftermarket accessories. If you’ve added a winch, upgraded suspension, installed custom seats, or invested in quality protective gear, that equipment isn’t protected under home or auto insurance. Many riders spend thousands customizing their ATVs for specific terrain or riding styles, but those investments disappear if theft or damage occurs. ATV insurance policies with comprehensive coverage and OEM endorsements specifically protect these additions. The OEM endorsement ensures repairs use original manufacturer parts when available, which matters significantly if your ATV has custom modifications that need replacing. Without this coverage, you absorb the full cost of replacing specialized equipment out of pocket.

Understanding these gaps is the first step toward real protection. The next section shows you exactly what coverage types matter most for your riding situation.

What Liability, Collision, and Comprehensive Coverage Actually Protect

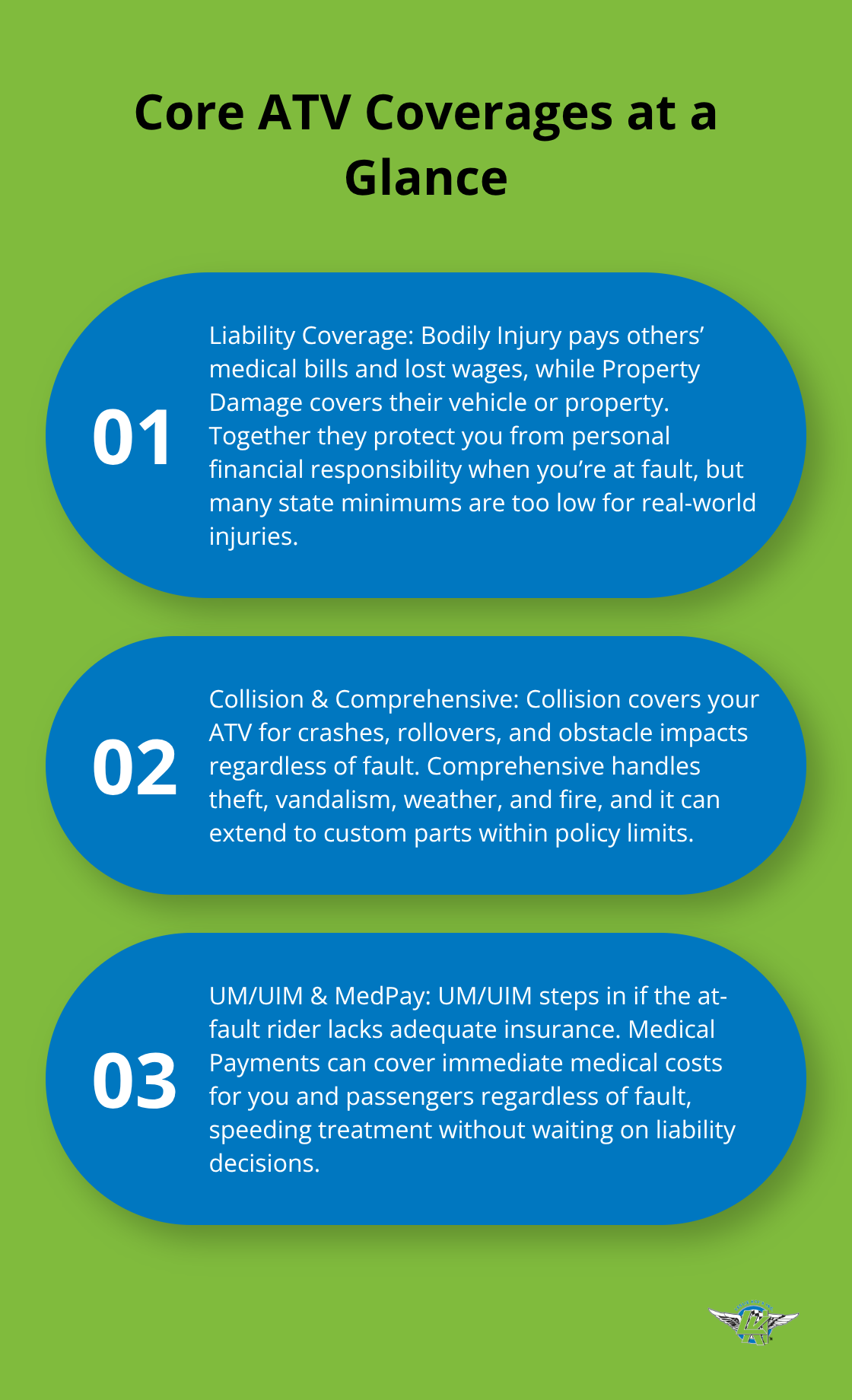

Liability Coverage Shields You from Financial Responsibility

Liability coverage is non-negotiable for ATV riding, and state law often requires it. Bodily Injury Liability pays medical bills and lost wages when you injure someone else in an accident, while Property Damage Liability covers damage to their vehicle or property. These two coverages work together to shield you from personal financial responsibility when you’re at fault. Most states set minimum liability requirements, but those minimums are dangerously low-often $15,000 to $25,000 combined. A single serious injury can exceed $100,000 in medical costs within days, leaving you personally liable for the difference if your policy limits fall short.

Collision and Comprehensive Coverage Protect Your ATV

Collision coverage protects your ATV itself when you crash, roll over, or hit an obstacle, paying for repairs regardless of who caused the damage. Off-road terrain creates collision risks that road riders never face-rocks, trees, and uneven ground cause impacts constantly. Comprehensive coverage handles theft, vandalism, weather damage, and fire-critical protection if you store your ATV outdoors or park it at trailheads. ATV theft remains a persistent problem in rural areas, making comprehensive coverage a practical investment. Comprehensive also covers custom parts and equipment up to your policy limit, which protects those expensive modifications you’ve already invested in.

Uninsured Motorist and Medical Payments Coverage Close Critical Gaps

UM/UIM coverage can cover injuries to you and damages to your bike if you’re hit by a driver with no insurance or not enough coverage for the injuries. This coverage pays your medical bills and vehicle repairs when you’re hit by an uninsured rider-a scenario that happens more often than most people assume. Many casual ATV riders carry minimal or no insurance at all, leaving you exposed if they cause your accident. Medical Payments coverage is optional but practical (it covers medical expenses for you and your passengers immediately after an accident, regardless of fault, without requiring you to prove liability first). This speeds up treatment and removes the waiting period while fault is determined.

Matching Coverage to Your Specific Riding Situation

State laws vary on which coverages are mandatory and which are optional, so your agent should review your specific state’s requirements. The right combination depends on your ATV’s value, your riding frequency, terrain type, and whether you ride alone or with passengers. A $3,000 ATV needs different coverage than a $15,000 machine with custom equipment. Riders who frequently tackle rough terrain should prioritize collision and comprehensive at higher limits, while trail explorers might adjust coverage downward. Your policy should reflect actual use-whether you ride weekends only or use your ATV for farm work, land maintenance, or regular trail adventures (your coverage needs shift as your riding habits change).

The next step is identifying which carriers actually specialize in off-road protection and how to compare their quotes against your specific riding profile.

Finding the Right ATV Carrier for How You Actually Ride

Assess Your Riding Frequency and Terrain

Honestly evaluate how often you ride and what terrain you tackle. Weekend trail explorers have entirely different coverage needs than someone using an ATV for farm work or land maintenance five days a week. Riders who stick to groomed trails in moderate conditions can operate with lower collision limits, while those tackling steep hills, dense woods, and rocky terrain need robust protection because impact risk climbs significantly. Track your typical riding pattern over the next month-note whether you ride once monthly or four times weekly, identify the terrain type, and determine whether you ride solo or frequently carry passengers. This data becomes your foundation for accurate quotes. If your riding changes seasonally (summer trail riding plus winter storage, for example), mention that to your agent because some carriers offer seasonal adjustments that lower premiums during off-season months.

Evaluate Custom Equipment and Modifications

Custom equipment and modifications dramatically affect your coverage requirements, yet most riders underestimate their total ATV investment. Calculate the actual cost of your machine plus any upgrades: winches, suspension systems, custom seats, protective gear, and accessories add up fast. If you own a $8,000 ATV plus $3,000 in modifications, your collision limit should reflect that $11,000 total value. Comprehensive coverage with an OEM endorsement protects those custom parts specifically-repairs use original manufacturer components when available rather than aftermarket substitutes, which matters when your bike has custom modifications that need exact replacements.

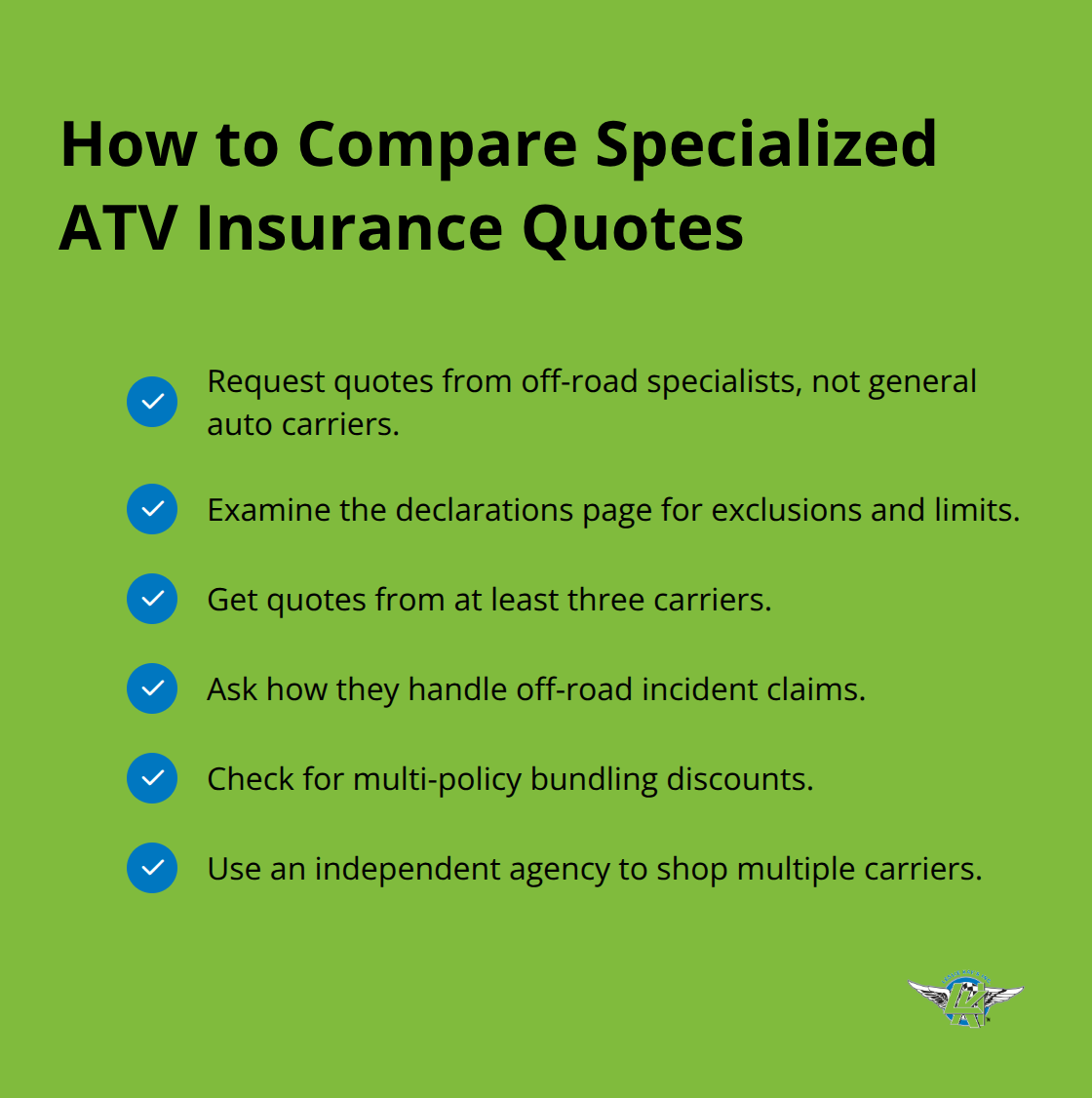

Compare Quotes from Specialized Off-Road Carriers

Request quotes from carriers that specialize in off-road vehicles rather than general auto insurers, because specialists understand ATV-specific risks and offer coverage options designed for terrain-based riding rather than cookie-cutter policies. When comparing quotes, examine the declarations page closely to understand exclusions, policy limits, and state-specific variations because coverage terms differ significantly by location.

Request quotes from at least three carriers, and specifically ask each one how they handle off-road incident claims, and whether they offer bundling discounts if you carry other policies with them. An independent agency shops multiple carriers to compare rates, coverage options, and benefits tailored to your specific riding profile-acting as your advocate rather than pushing you toward one carrier’s standard package.

Final Thoughts

Standard auto insurance leaves ATV riders completely exposed. Your homeowner’s policy won’t cover off-road riding, liability gaps can cost you tens of thousands, and custom equipment sits unprotected without specialized coverage. A custom ATV insurance policy designed specifically for your riding style eliminates these dangerous gaps and gives you actual protection when you need it most.

Specialized carriers understand off-road risks in ways general auto insurers simply don’t. They offer terrain-based coverage options, handle claims faster, and provide guidance on exclusions and limits specific to your state. An independent agency shops multiple carriers to find competitive rates and benefits tailored to your profile, acting as your advocate rather than pushing a one-size-fits-all package.

Contact Leslie Kay’s, Inc. today to get quotes from carriers that actually specialize in off-road vehicles and secure the coverage your ATV deserves. We shop multiple carriers to deliver customized policies with hands-on claims support. We understand your riding lifestyle and build protection that matches it.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.