Freshwater boat insurance isn’t optional if you want real protection on the water. Accidents, theft, and liability claims can drain your finances fast without proper coverage.

We at Leslie Kay’s, Inc. help boat owners understand what they actually need to stay protected. This guide walks you through the coverage types, how to pick the right policy, and what matters most for your situation.

Why Freshwater Boat Insurance Matters

Freshwater boat damage strikes faster than most owners expect. Submerged rocks, logs, and debris cause hull breaches that insurance won’t cover without physical damage protection. A collision with a dock or pier costs $5,000 to $15,000 in repairs, depending on your boat’s size and construction. Without hull coverage, you pay out of pocket. Liability claims create even bigger financial exposure-if your boat hits another vessel or injures someone on the water, medical costs and property damage can easily exceed $100,000. State requirements vary, but most lenders and marinas demand proof of coverage before you can finance or dock your boat.

Freshwater lakes present specific hazards that saltwater policies don’t address. Invasive species like zebra mussels clog engine intakes and damage propulsion systems, while seasonal storms bring lightning strikes and hail damage that standard homeowners policies explicitly exclude. Theft happens too-boat trailers and electronics disappear from lakeside parking areas more often than owners realize, and replacement costs for trolling motors and fish finders run $1,000 to $5,000 each.

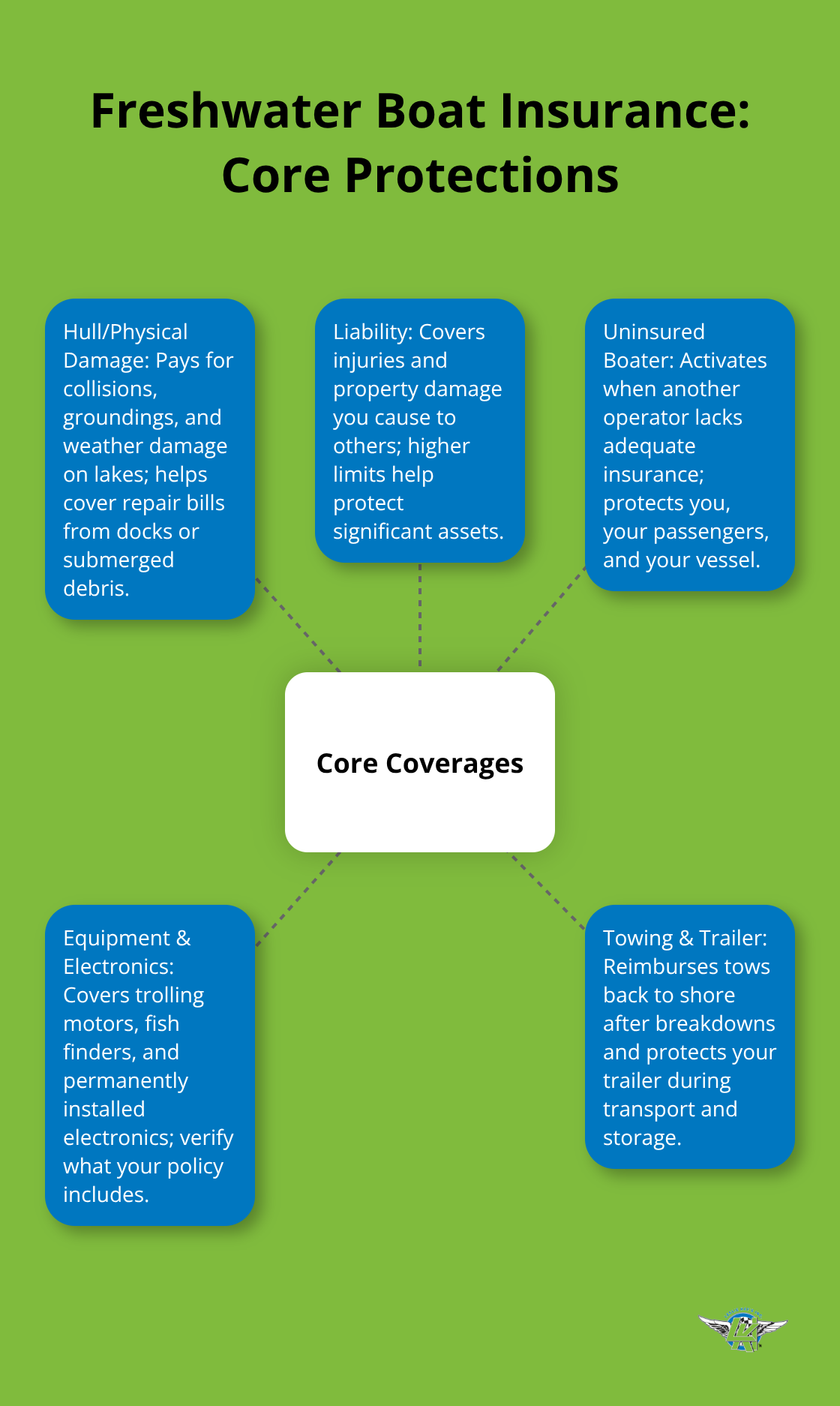

Physical Damage Coverage: What It Actually Protects

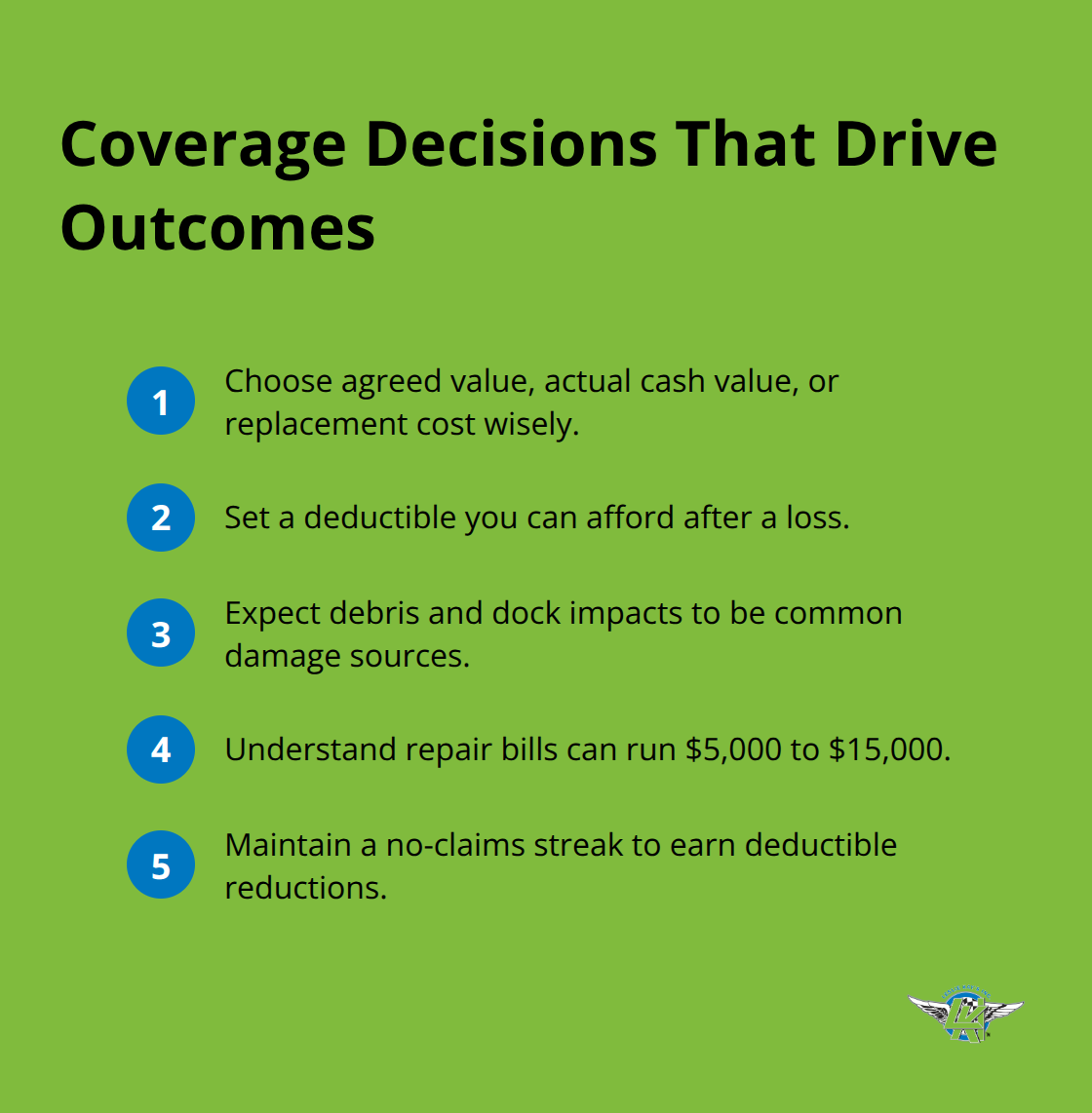

Hull coverage under a comprehensive or all-risk policy pays for collisions, groundings, and weather damage. The difference between agreed value and actual cash value matters significantly. Agreed value coverage pays what you and your insurer decided the boat was worth when you bought the policy, while actual cash value only covers depreciated value at claim time. For boats under three years old, replacement cost coverage reimburses you for a new boat of the same make, class, size, and type-eliminating depreciation losses entirely.

Your deductible choice directly impacts your premium. Selecting a $1,000 deductible instead of $500 typically lowers your annual cost by 15 to 25 percent. Many policies also reduce deductibles by about 25 percent for every consecutive year you file no claims, rewarding safe boating habits with real savings.

Liability and Medical Coverage: Your Financial Safeguard

Liability coverage protects you when your boat causes injury or property damage to others. Standard freshwater policies include liability, but limits vary-most carriers offer $100,000 to $300,000 in coverage. Carrying higher limits makes sense if you have significant assets to protect.

Medical payments coverage, often included or available as an add-on, covers medical expenses for injured passengers without requiring fault determinations. Uninsured boater coverage protects you when another operator lacks adequate insurance, a critical safeguard on popular lakes where enforcement is inconsistent. This coverage activates if an uninsured or underinsured boater causes damage to your vessel or injures you and your passengers.

Equipment and Specialized Coverage Options

Equipment coverage protects onboard electronics, trolling motors, fishing gear, and safety items. Verify coverage for permanently installed electronics when you quote, since some policies limit what they cover. Towing coverage reimburses reasonable costs to recover and return your boat to shore after a breakdown on the water.

Storm coverage provides compensation for repairs or replacement due to hurricanes, lightning, and hail-protection that standard homeowners policies won’t provide. Trailer coverage is commonly included or available as an add-on, essential when you transport your boat on inland lakes. These add-ons fill gaps that basic policies leave open, and the right combination depends entirely on how you use your boat and what equipment you carry.

Types of Coverage That Actually Matter for Freshwater Boats

Hull coverage and comprehensive protection form the foundation of any freshwater boat policy, but the specific type you choose determines what happens when damage occurs. Agreed value coverage pays the amount you and your insurer agreed upon when the policy started, while actual cash value only reimburses depreciated value at claim time-a significant difference on older boats. For boats under three years old, replacement cost coverage eliminates depreciation entirely by paying for a new boat of the same make, class, size, and type. This matters because boat depreciation rates for freshwater boats typically show 8-10% depreciation in the first year; actual cash value on a total loss could leave you significantly short of what you need to replace it.

Your deductible choice directly affects your premium and out-of-pocket costs when claims happen. Jumping from a $500 deductible to $1,000 typically reduces annual premiums by 15 to 25 percent, and many policies reduce deductibles by roughly 25 percent for each consecutive year without claims. Submerged rocks, logs, and debris cause the majority of freshwater hull damage, along with collisions at docks and piers that cost $5,000 to $15,000 in repairs depending on boat size and construction. Without physical damage coverage, you absorb these costs entirely.

Liability Coverage Protects Your Assets

Liability coverage protects you when your boat injures someone or damages another vessel, with standard limits ranging from $100,000 to $300,000. Higher limits make sense if you own significant assets-a serious injury claim can easily exceed $100,000 in medical costs and lost wages. Medical payments coverage, often included or available as an add-on for $500 to $2,000 annually, covers injured passengers without requiring fault determinations and streamlines claims handling.

Uninsured Boater Coverage Fills a Critical Gap

Uninsured boater coverage activates when another operator lacks adequate insurance, a critical protection on popular lakes where enforcement remains inconsistent. This coverage protects both your vessel and your passengers when an uninsured or underinsured boater causes damage or injury. Many boat owners overlook this protection, yet it addresses a real risk that standard liability policies cannot cover.

Equipment and Specialized Add-Ons

Equipment coverage protects trolling motors, fish finders, and permanently installed electronics-items that cost $1,000 to $5,000 each to replace. Verify exactly what qualifies as covered equipment when you quote, since policies vary on whether they cover portable versus permanently installed gear. Towing coverage reimburses reasonable recovery costs after a breakdown on the water, typically ranging from $250 to $500 per incident. Storm coverage compensates for damage from lightning, hail, and seasonal weather-protection your homeowners policy explicitly excludes. Trailer coverage, commonly included or available as an add-on, protects your boat trailer during transport and storage.

Freshwater-Specific Hazards Require Attention

Invasive species like zebra mussels clog engine intakes and damage propulsion systems, yet standard policies often overlook these inland hazards. Discuss freshwater-specific risks with your agent to close coverage gaps before they become expensive problems. The right combination of add-ons depends entirely on how you use your boat and what equipment you carry-which means your next step involves assessing your actual boat value and usage patterns to determine which coverages truly matter for your situation.

How to Choose the Right Freshwater Boat Insurance Policy

Start with an Accurate Boat Valuation

Your boat’s current value drives everything else-hull coverage limits, replacement cost decisions, and ultimately your premium. Most owners underestimate what their boat is actually worth, which creates serious problems when claims happen. Collect your purchase documents, recent maintenance records, and any upgrades you’ve made, then check current market prices on platforms like NADA Guides or Boat Value to see what similar boats sell for in your region. Understating your boat’s value creates a coverage gap that insurance won’t fill during a claim, while overstating it inflates your premium unnecessarily.

Document Your Actual Usage Patterns

How you use your boat determines your insurance costs more than almost anything else. Tournament fishing and high-horsepower bass boats typically cost 20 to 30 percent more to insure than recreational cruising because they carry greater risk and more expensive electronics. Storage location affects rates significantly-boats stored at a marina dock slip cost more than those kept in a garage or off-site storage because dock theft happens regularly. Once you know your boat’s value and usage pattern, you have the information needed to request quotes that actually reflect your situation.

Compare Quotes from Multiple Carriers

Comparing quotes from multiple carriers reveals how dramatically prices vary for identical coverage. Contact at least three insurers that advertise marine policies-Progressive, BoatUS Insurance, and regional carriers often quote differently based on their underwriting criteria and available discounts. When you call, provide the exact same boat details (year, make, model, length, hull identification number, engine horsepower, current value) and coverage preferences to each insurer so the quotes are genuinely comparable.

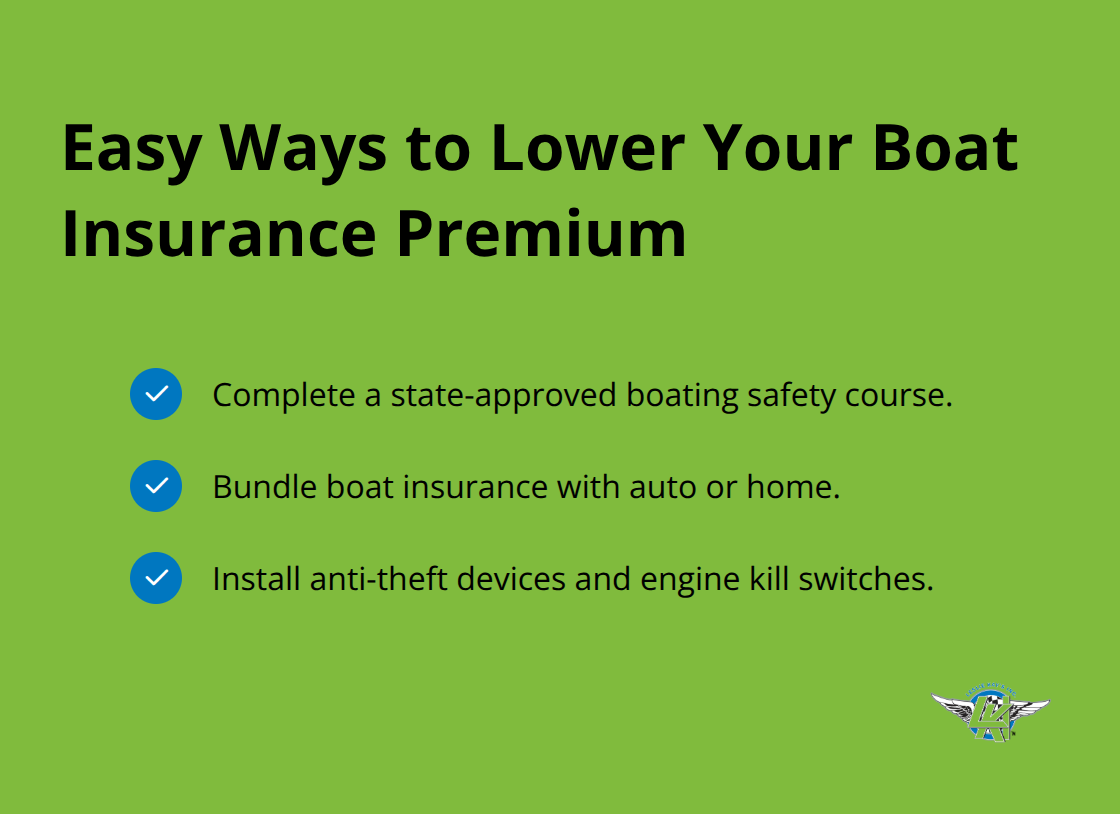

Most carriers offer 15 to 25 percent discounts for completing a boating safety course, bundling boat insurance with auto or home policies, and installing anti-theft devices like engine kill switches. A boating safety course costs $30 to $100 online and pays for itself through premium savings within a year, plus it strengthens your navigation skills on the water.

Select Your Deductible Strategically

Deductible selection directly impacts your final premium. Jumping from $500 to $1,000 typically cuts your annual cost by 15 to 25 percent, while $2,500 deductibles lower premiums even further if your emergency fund can absorb that out-of-pocket expense. Choose a deductible that aligns with what you can actually afford to pay after a loss, not the lowest number available.

Verify Coverage Details Before You Commit

Once you have three quotes with identical coverage options, compare the liability limits each carrier offers and verify that freshwater-specific coverage like uninsured boater protection is included. Confirm that add-ons like equipment coverage and towing align with your boat’s electronics and how often you venture far from shore. At Leslie Kay’s, Inc., we shop multiple carriers to help you find the right protection at competitive rates, with hands-on support when you need it most.

Final Thoughts

Freshwater boat insurance protects your investment and your finances when accidents, theft, or liability claims happen on the water. Hull protection, liability coverage, uninsured boater protection, and equipment add-ons work together to address the specific risks you face on lakes and inland waterways. Your boat’s value, how you use it, and where you store it determine which combination of coverages actually matters for your situation.

Choosing the right policy requires honest assessment of your boat’s current value, accurate documentation of your usage patterns, and comparison shopping across multiple carriers. A $1,000 deductible instead of $500 cuts your premium by 15 to 25 percent, while completing a boating safety course saves another 15 to 25 percent through available discounts. These decisions compound quickly, turning a thorough quoting process into real savings without sacrificing the protection you need.

Start with your boat’s details-year, make, model, length, hull identification number, engine horsepower, and current value-along with information about how you use it and where you store it. Visit Leslie Kay’s, Inc. to get a freshwater boat insurance quote tailored to your lakeside boating lifestyle, or call to speak with an agent who understands what protection actually matters for your adventures on the water.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.