RV owners often overpay for insurance simply because they don’t know what factors drive their premiums. At Leslie Kay’s, Inc., we’ve helped countless travelers find better recreational vehicle insurance rates by understanding exactly what insurers look for.

The difference between a quote that drains your budget and one that fits your lifestyle comes down to knowing where to look and what questions to ask. This guide walks you through the process step by step.

What Drives Your RV Insurance Costs

Vehicle Type Sets Your Premium Foundation

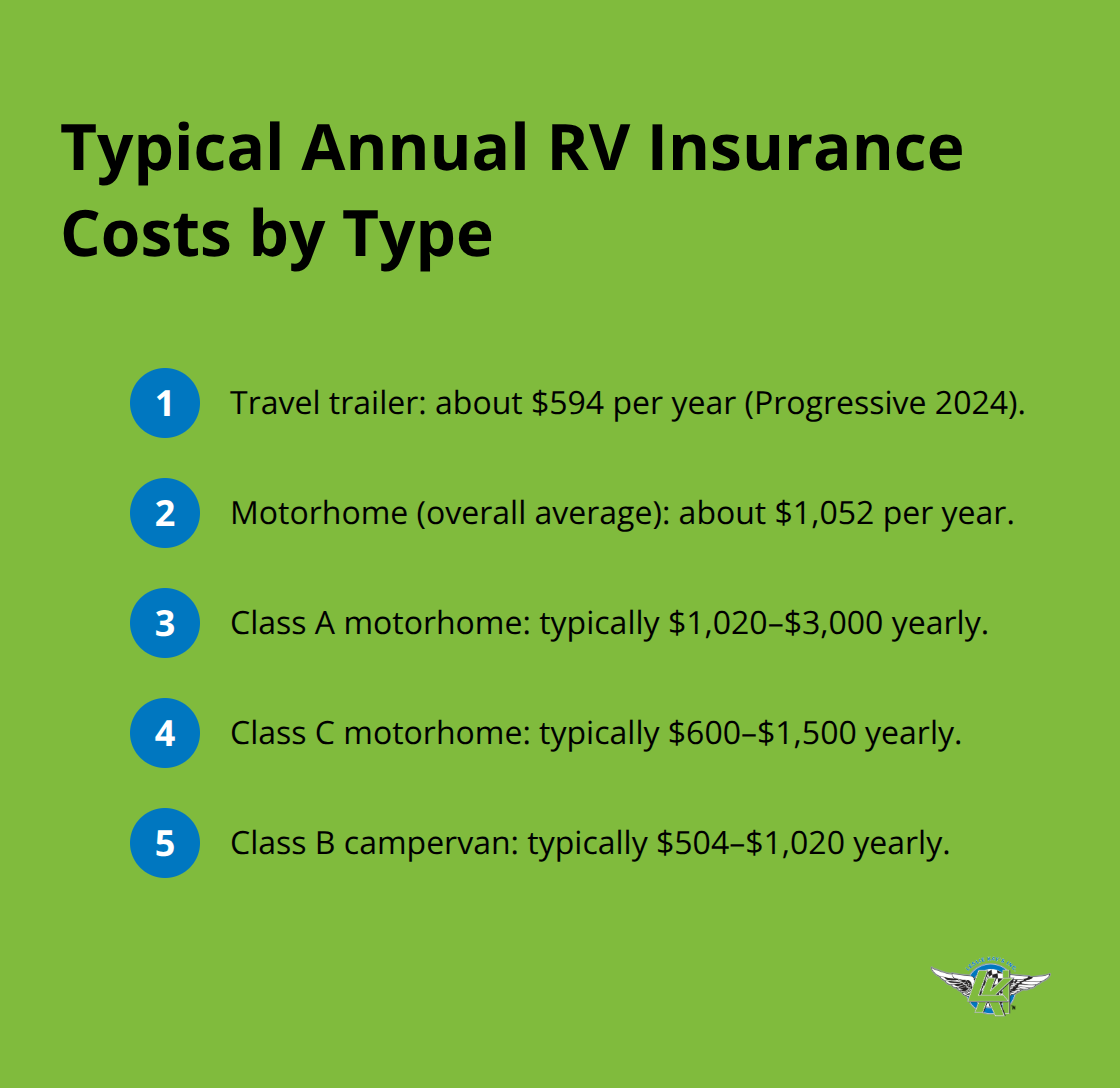

Your RV type matters more than almost any other factor in determining your premium. Travel trailers run about $594 annually according to Progressive’s 2024 data, while motorhomes jump to $1,052 per year on average. Class A motorhomes typically cost $1,020 to $3,000 yearly, Class C models range from $600 to $1,500, and Class B campervans fall between $504 and $1,020. The difference comes down to replacement value-a luxury Class A costs insurers far more to replace than a lightweight travel trailer, so they charge higher premiums to offset that risk.

New or high-value RVs amplify this effect; conversely, very old RVs can be expensive to insure because mechanical failures and scarce parts create unpredictable claims. If you shop for an RV, understand that a less expensive unit upfront often means substantially lower insurance costs over time, which compounds the savings benefit of budget-friendly models.

How You Use Your RV Shapes Your Rate

Your driving history and how you use the RV shape your quote just as much as the vehicle itself. A clean record without accidents or claims typically qualifies you for lower rates, while at-fault accidents and insurance claims push premiums up noticeably. How many days per year you plan to use the RV matters too-recreational users who take occasional trips pay far less than full-time RVers who live in the vehicle 150 or more nights annually.

Full-time residents need hybrid coverage blending auto and homeowners protections, costing $1,500 to $4,000 yearly, whereas recreational users typically pay $300 to $800. Location matters significantly-densely populated areas, regions with harsh winters like New York, and theft hotspots all see higher premiums than rural or low-crime zones.

Deductibles and Coverage Limits Control Your Cost

Liability coverage limits and deductible amounts directly affect your premium; you can raise your deductible from $500 to $1,000 to lower your annual cost, but you’ll pay more out-of-pocket if you file a claim. Financed RVs require comprehensive and collision coverage by lender mandate, which increases your premium compared to liability-only policies that start around $125 annually.

These variables interact in complex ways. A financed Class A motorhome in a high-risk urban area with a young driver and a $500 deductible will cost substantially more than a paid-off travel trailer in a rural zone with an experienced driver and a $1,500 deductible. Understanding how each lever affects your rate prepares you to make informed decisions when you compare quotes from multiple carriers.

Comparing RV Insurance Quotes Without Wasting Your Time

Request Quotes from Multiple Carriers at Once

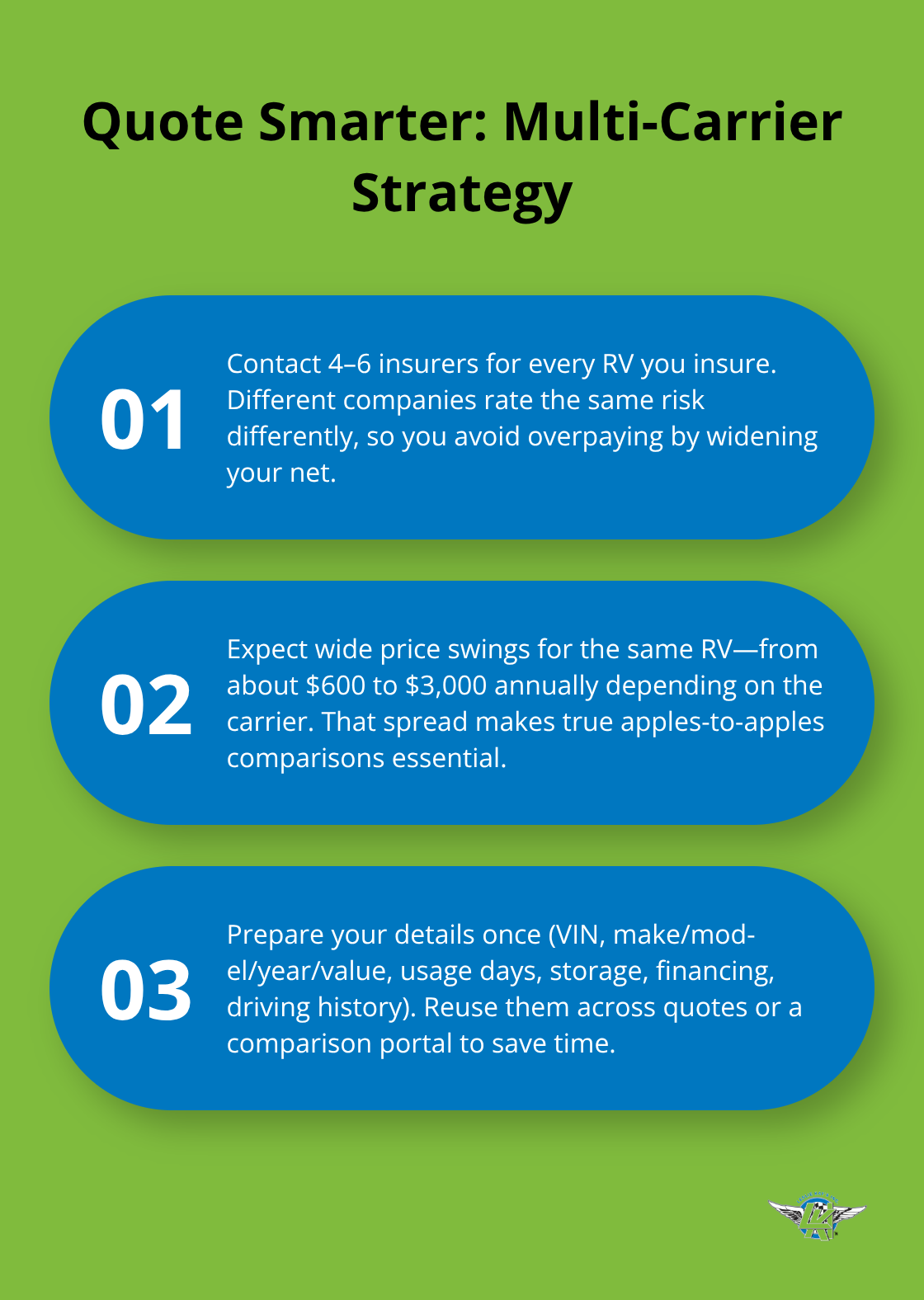

You must contact at least four to six insurers if you want to avoid overpaying for RV coverage. Progressive, Auto-Owners, Nationwide, National General, Good Sam, and Roamly each price risk differently, and the same RV can carry premiums ranging from $600 to $3,000 annually depending on which company quotes you. Most RV owners stop after contacting two or three carriers and settle for whatever sounds reasonable-that approach costs you money.

The real strategy involves preparing your information upfront so you don’t waste time repeating details across multiple calls. Collect your RV’s VIN, make, model, year, and current value; your driving history; how many days annually you’ll use the RV; your storage location; and whether the RV is financed. When you contact insurers or use comparison platforms like Good Sam Insurance Agency (which partners with Progressive, Foremost, Safeco, and National General in a single portal), you can input this information once and receive multiple quotes without calling each company separately. This single step cuts your research time dramatically while ensuring apples-to-apples comparison across carriers.

Understand What Each Policy Actually Covers

Reading beyond the premium number separates smart shoppers from those who leave money on the table. Nationwide offers over ten discounts including RV safety course completion and paid-in-full incentives, potentially saving you up to 20 percent when you bundle with homeowner coverage, yet some discounts don’t appear online until you request a formal quote. National General stands out for specialized options like suspending collision and liability coverage during storage periods, which reduces your winter premium substantially, and offering full replacement cost coverage that pays the purchase price for the first nine years regardless of depreciation.

Roamly focuses specifically on full-time RVers with emergency expense allowances and loss assessment coverage, while Progressive includes accident forgiveness for comprehensive and collision claims on vehicles valued at $25,000 or more at purchase. This means your first at-fault accident won’t automatically spike your rate. The discount landscape matters equally: a clean three-year driving record, original ownership status, and paying your premium in full each unlock savings across most carriers, but RV-specific discounts for safety courses or RV club membership vary by insurer.

Ask Representatives About Hidden Discounts

Don’t assume a lower initial quote includes the discounts you qualify for. Call back and explicitly ask what savings apply to your situation, as representatives sometimes reveal additional programs during conversation that don’t appear on written quotes. This direct approach often uncovers savings that online quote tools miss, turning a mediocre offer into a competitive one.

The next step involves identifying which coverage options match your actual RV usage and lifestyle, since optional add-ons can significantly impact both your premium and your protection level.

Real Ways to Cut Your RV Insurance Costs

Bundle Policies to Unlock Immediate Savings

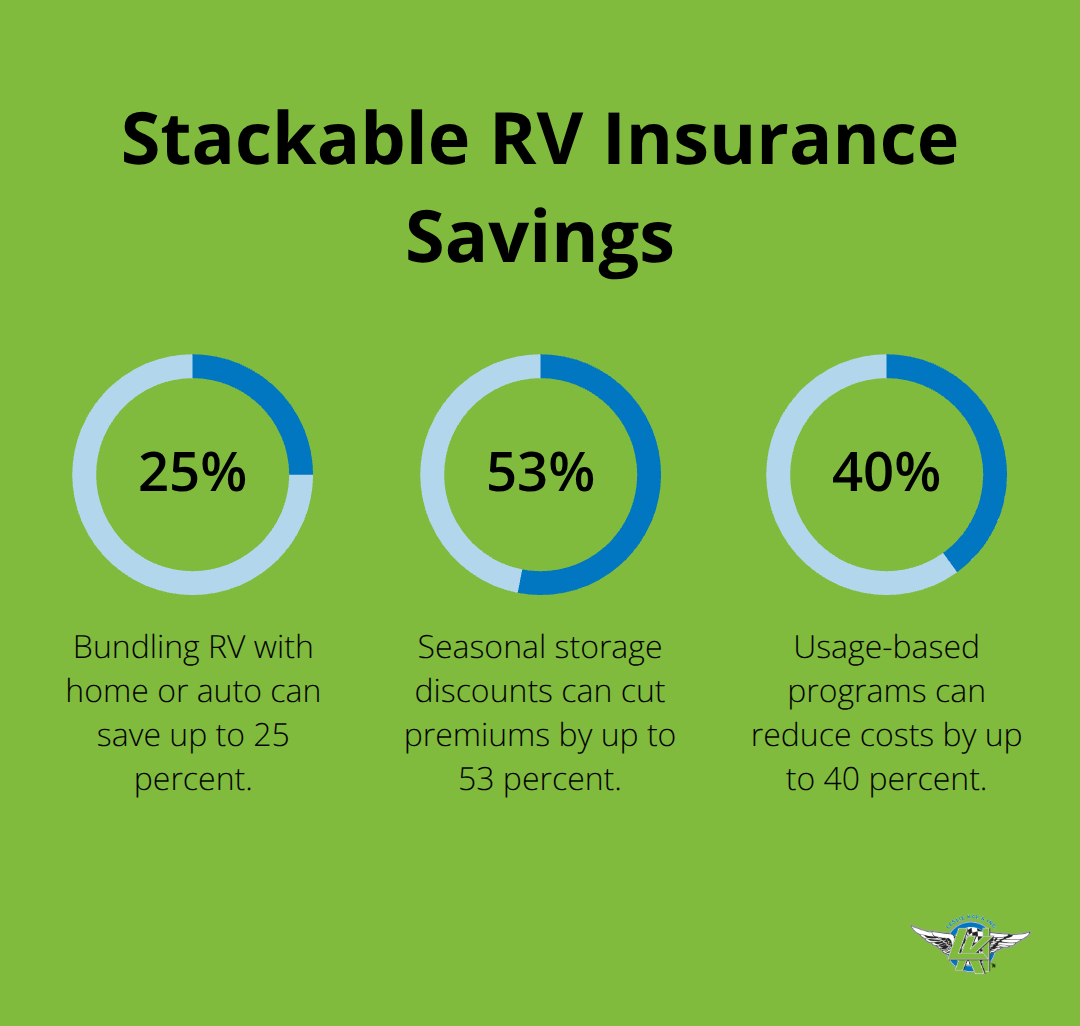

Combining your RV policy with homeowner or auto coverage delivers measurable savings that most RV owners overlook. Bundling RV insurance with home and auto coverage can save you up to 25% on your annual premiums, and this discount applies whether you own one vehicle or five. Insurers reward customer loyalty and reduce administrative costs when they handle multiple policies, passing those savings directly to you. Contact your current homeowner or auto insurer first to see what bundling options exist, then compare that bundled rate against standalone RV quotes from carriers like Progressive or National General. You might find that staying with your existing insurer beats switching to a specialist, or you might discover that a fresh start with a new carrier saves you hundreds annually. The only way to know is requesting bundled quotes alongside standalone options.

Reduce Premiums During Storage Months

Storage discounts amplify savings further-Good Sam reports reductions up to 53 percent when you store your RV during winter months, since parked vehicles generate fewer claims. This matters enormously in states like New York where seasonal storage is standard practice. If you don’t use your RV from November through March, suspend or reduce your liability and collision coverage during those months rather than paying full premiums for a stationary asset.

Leverage Your Clean Driving Record

Your driving record directly translates to dollar amounts on your bill, making this the one factor you control most effectively. Drivers with three or more years of clean history without accidents or claims qualify for discounts across all major carriers, while a single at-fault accident can raise your rate 15 to 25 percent. Progressive’s accident forgiveness program eliminates this penalty for comprehensive and collision claims on vehicles valued at $25,000 or more at purchase, but you only access this benefit if you choose that carrier.

Enroll in Usage-Based Monitoring Programs

Usage-based programs like Nationwide SmartRide save up to 40 percent by monitoring your actual driving patterns rather than charging a flat rate based on demographics. This approach rewards careful drivers who maintain safe speeds, avoid hard braking, and drive fewer miles annually. Install a usage-tracking app, drive conservatively during the monitoring period, and you’ll see meaningful reductions reflected in your renewal quote. These programs work best for recreational RV users who take occasional trips rather than full-time travelers, since infrequent drivers naturally demonstrate safer patterns. The combination of a clean record plus a usage-based discount can easily save $400 to $600 annually compared to standard recreational rates.

Final Thoughts

Finding affordable recreational vehicle insurance rates comes down to three concrete actions: understanding what drives your premium, comparing quotes across multiple carriers, and claiming every discount you qualify for. Vehicle type, driving history, and coverage choices determine your cost, but these factors only matter if you shop strategically. Most RV owners accept the first quote they received, leaving hundreds or thousands of dollars on the table annually.

A travel trailer might cost $594 per year with one insurer and $800 with another, while a Class A motorhome could range from $1,020 to $3,000 depending on which company you contact. That $200 to $1,000 difference per year adds up fast over a five or ten-year ownership period. Bundling your RV policy with home or auto coverage saves up to 25 percent, storage discounts cut premiums by 53 percent during winter months, and usage-based programs reward safe drivers with reductions up to 40 percent.

Start by gathering your RV’s details, driving history, and usage information, then request quotes from at least four to six carriers. Contact Leslie Kay’s, Inc. to work with an independent agent who shops multiple carriers on your behalf, saving you time while ensuring you don’t miss discounts or coverage options that match your situation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.