Most riders think they’re already getting the best deal on their motorcycle insurance. The truth is, the average motorcyclist leaves hundreds of dollars on the table every year by missing simple discounts and making preventable coverage mistakes.

At Leslie Kay’s, Inc., we’ve helped countless riders find rider motorcycle insurance discounts they didn’t know existed. This guide shows you exactly where those savings hide and how to restructure your policy to pay less without sacrificing protection.

Real Discounts That Actually Lower Your Rate

Safety Course Discounts Pay for Themselves

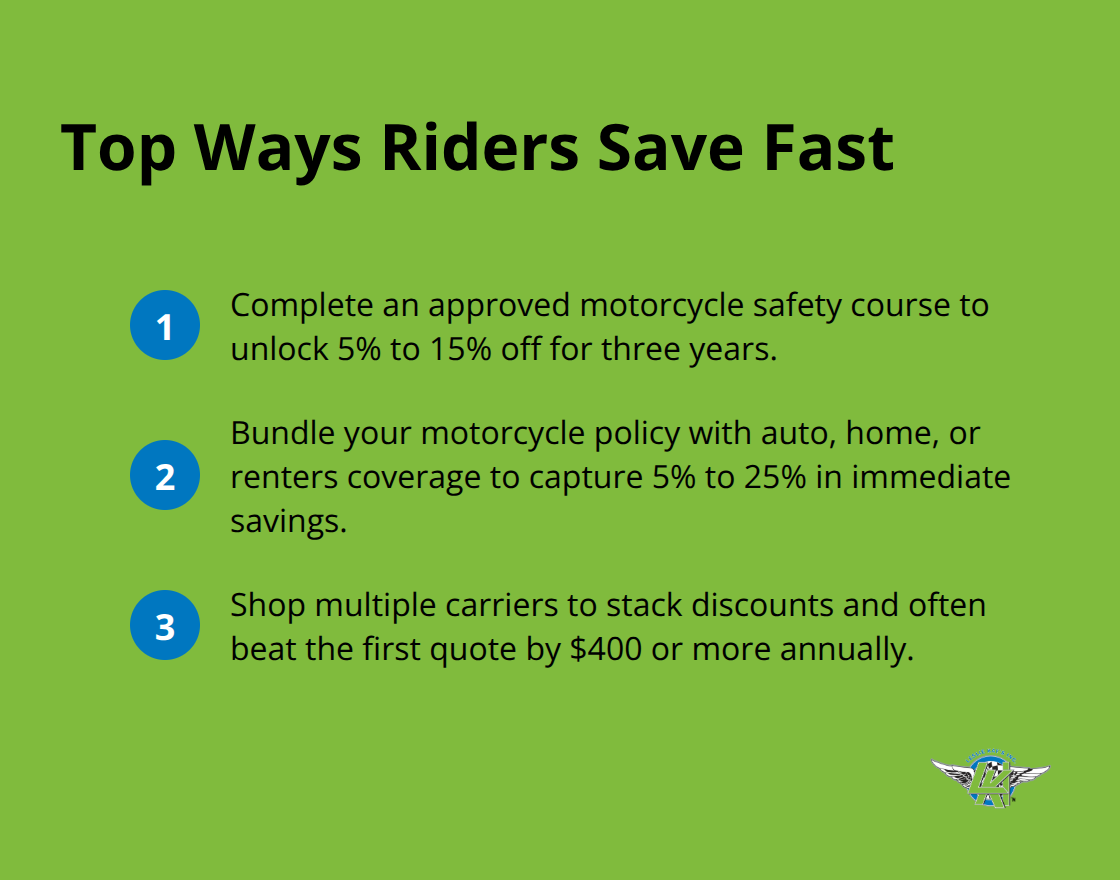

An approved motorcycle safety course cuts your premium far more than most riders realize. The Motorcycle Safety Foundation course qualifies you for discounts at nearly every major carrier, and the savings typically range from 5% to 15% off your policy. The discount lasts for three years after you finish the course, so one weekend of training pays dividends for years. If you’re a safety instructor, some carriers offer even steeper discounts for your credentials. Most riders see $200 to $400 knocked off their annual premium after submitting their course completion certificate (which costs roughly $200 to $300 to obtain). That’s a return on investment that happens in a single policy year.

Bundle Multiple Policies for Immediate Savings

Bundling your motorcycle policy with auto, home, or renters coverage is where real money disappears if you’re not paying attention. Most riders carry their motorcycle insurance separately from their car insurance, which means they miss out on bundle discounts that typically range from 5% to 25% depending on the carrier and what you bundle together. When you consolidate multiple policies under one insurer, the math works in your favor immediately. A rider with an auto policy and motorcycle policy bundled together can save $300 or more annually on the combined premium.

Leverage Your Riding Experience

Your riding experience matters to insurers because the data shows experienced riders file fewer claims. Carriers reward riders with three or more years of on-road experience with lower rates. Some insurers specifically target riders over 45 with a clean record and more than three years of riding history, offering additional discounts on top of your base rate. The key is telling your agent exactly how long you’ve been riding and confirming they’ve applied every experience-based discount your carrier offers.

Shop Multiple Carriers to Stack Discounts

Most riders accept the first quote they receive, which means they leave discounts on the table. When you shop multiple carriers, you uncover which insurer offers the best combination of discounts for your specific situation. One carrier might excel at bundling discounts while another rewards safety course completion more generously. The difference between carriers can easily exceed $400 annually on the same coverage. Your agent should compare quotes across multiple insurers to stack every available discount together, not just one or two that leave money on the table.

Mistakes That Drain Your Motorcycle Insurance Budget

Underestimating Your Coverage Limits

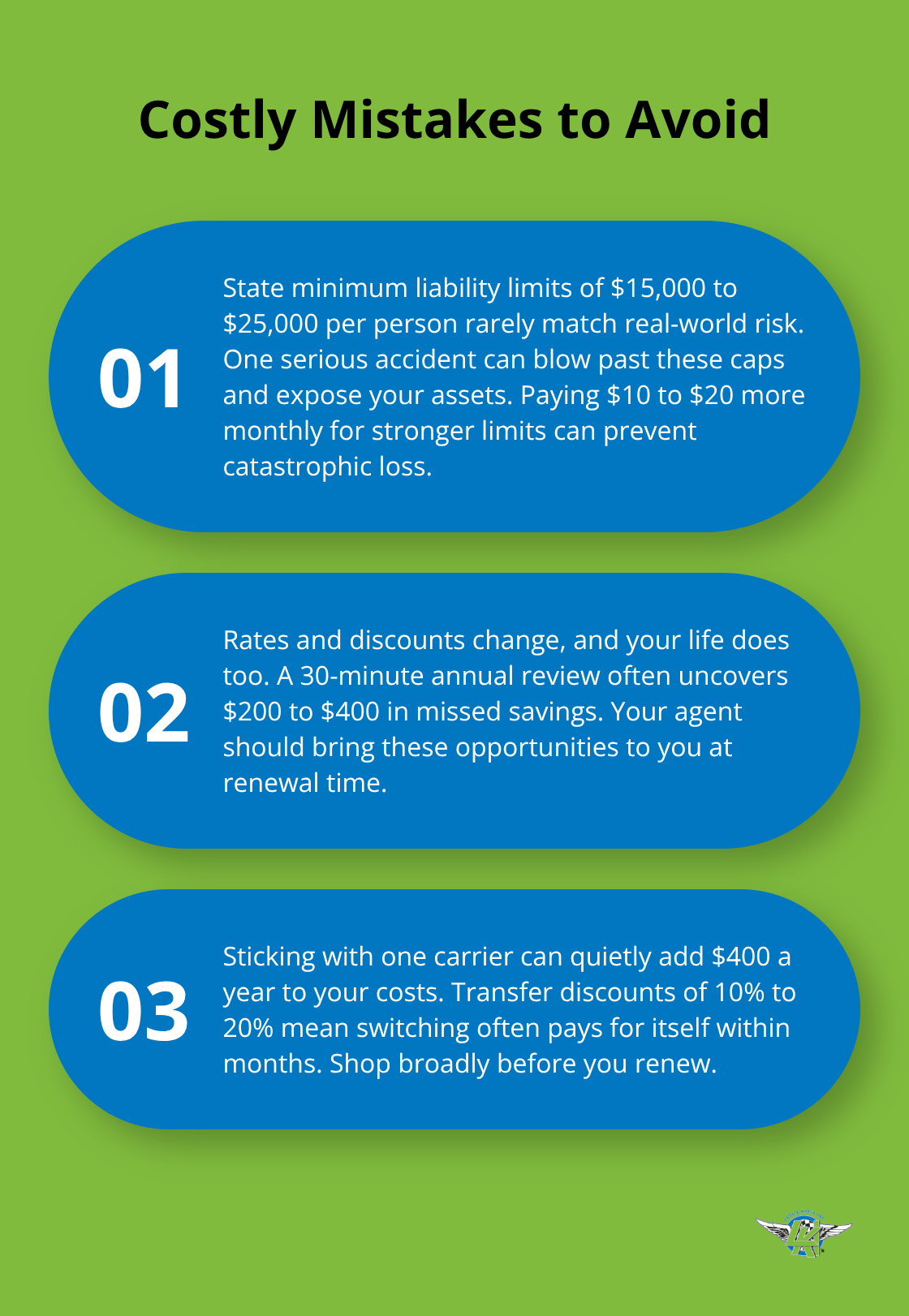

Most riders set their coverage limits based on state minimums instead of actual risk. State minimum liability coverage typically sits between $15,000 and $25,000 per person, which sounds reasonable until you cause an accident that injures multiple riders or damages a vehicle worth $50,000. A single lawsuit can exceed your coverage limits by hundreds of thousands of dollars, leaving your personal assets vulnerable. The cost difference between state minimum liability and proper coverage is often just $10 to $20 monthly, yet it protects you from catastrophic financial exposure.

Your comprehensive and collision coverage matters equally. Riders who skimp on these limits to save a few dollars discover too late that their $12,000 bike won’t be fully replaced with a $500 deductible and minimal coverage. Adequate limits cost far less than the financial devastation an underinsured claim creates.

Ignoring Your Annual Policy Review

You never review your policy after the first year-and that costs you real money. Rates change, new discounts appear, and your circumstances shift, yet most riders pay renewal premiums without question. Insurance carriers count on this inertia to keep you overpaying.

A rider who completed a safety course last year might not have applied that discount to their renewal. Someone who bundled policies three years ago might have missed an additional discount that appeared at their carrier last year. Annual policy reviews take 30 minutes and frequently reveal $200 to $400 in untapped savings. Your agent should initiate this conversation at renewal time, not wait for you to ask.

Missing Discounts You Actually Qualify For

Many riders qualify for discounts they’ve never claimed because they don’t match the carrier’s specific criteria or because their agent never asked the right questions. A rider with 15 years of experience might qualify for a preferred operator discount that requires proof of riding history. A homeowner might miss a homeowner discount simply because the agent didn’t ask. An active military member or affinity group participant leaves money on the table without mentioning their status.

Your agent needs to ask detailed questions about your riding history, home ownership, military service, group memberships, and safety training to uncover every available discount. Most carriers won’t volunteer these savings-you have to claim them.

Staying With Your Current Carrier Too Long

Shopping multiple carriers every few years reveals a hard truth: your current insurer might no longer offer the best rates for your situation. A rider who got a great quote five years ago could be overpaying by $400 annually today while a competitor offers better rates for the same coverage. Transfer discounts from switching carriers typically range from 10% to 20%, which means moving to a cheaper option often pays for itself within months.

The carriers that offer the best rates shift constantly based on their claims experience and market strategy. Loyalty doesn’t reward you-it rewards them. An independent agency that shops multiple carriers (rather than pushing you toward one insurer) reveals which option actually fits your needs and budget today, not yesterday.

How to Maximize Your Savings With the Right Coverage Strategy

Choose Your Deductible Based on Your Financial Reality

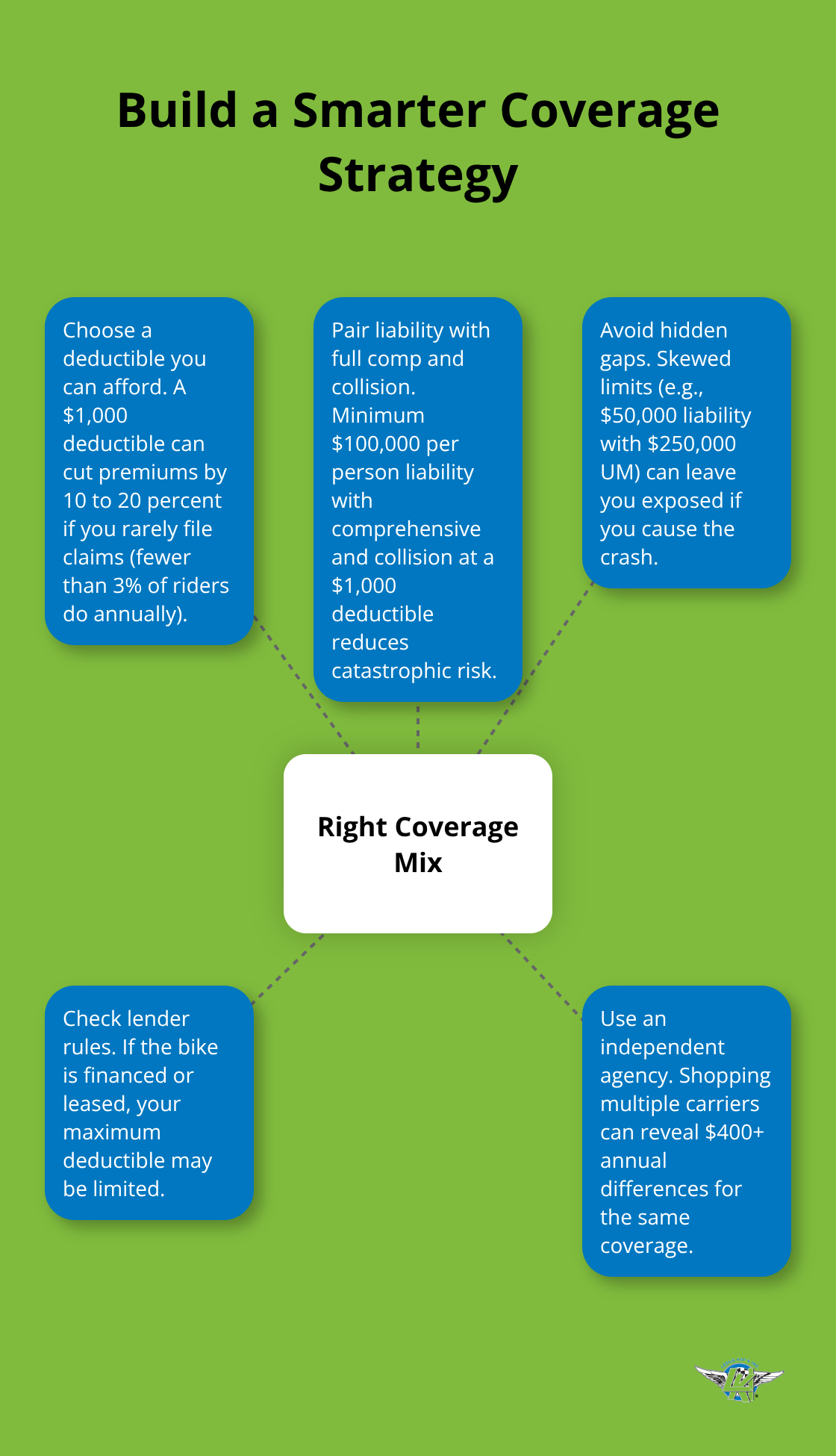

Deductible selection separates riders who understand their finances from those who guess. Most riders pick a $500 deductible because it sounds middle-ground, but that choice often costs more annually than it saves. If you carry comprehensive and collision coverage on a bike worth $15,000 or more, a $1,000 deductible can reduce premiums by 10 to 20 percent compared to a $500 deductible. The math only fails if you file claims frequently, which statistically happens to fewer than 3% of riders annually. A rider filing one claim every ten years pays far less overall with the higher deductible and lower premiums. However, if your bike is financed or leased, your lender dictates the maximum deductible allowed, so this choice disappears.

The real decision comes down to emergency cash reserves. If you can absorb a $1,000 loss without financial stress, the higher deductible wins. If a $1,000 unexpected expense creates hardship, stick with $500 and accept the higher premium as insurance against your own cash flow problems.

Pair Liability With Comprehensive and Collision Coverage

Liability coverage and physical damage coverage work together, and treating them as separate decisions costs you money. Many riders max out liability limits at $100,000 or $250,000 per person, then cut comprehensive and collision to bare minimums to offset the cost. That strategy backfires because it protects everyone except yourself.

A $50,000 liability limit with $250,000 in uninsured motorist coverage creates a dangerous gap: if an uninsured driver hits you, you’re covered, but if you hit them, your liability exposure is limited. Worse, comprehensive and collision cover your bike’s actual replacement value, not what you owe on it. A $12,000 motorcycle with a $2,500 deductible and minimal coverage leaves you with roughly $9,500 maximum payout after a total loss, which rarely covers a replacement bike.

The solution is pairing adequate liability limits (minimum $100,000 per person) with full comprehensive and collision coverage at a $1,000 deductible, then accepting the premium that comes with real protection. This combination typically costs $50 to $100 monthly more than underinsured policies, yet it eliminates catastrophic financial risk.

Work With an Agency That Shops Multiple Carriers

An independent agency that shops multiple carriers finds the insurer offering the best rates for your coverage combination, which often costs less than you’d expect when discounts are properly stacked. Leslie Kay’s, Inc. specializes in this approach-shopping multiple carriers to deliver customized policies at competitive prices. The difference between carriers can easily exceed $400 annually on the same coverage, so comparing options across insurers (rather than accepting the first quote) reveals which option actually fits your needs and budget today.

Final Thoughts

The path to lower motorcycle insurance premiums starts with understanding that most riders overpay because they never actively manage their policies. Safety course discounts, bundle savings, and experience-based rate reductions exist at nearly every carrier, yet they remain unclaimed by riders who fail to ask the right questions. Your annual renewal is the moment to stop accepting whatever premium arrives in the mail and start demanding better rates through strategic coverage choices and discount stacking.

The real savings come from combining three actions: completing an approved safety course to lock in a three-year discount, bundling your motorcycle policy with auto or home coverage to capture immediate savings, and shopping multiple carriers to find which insurer rewards your specific situation best. A rider who implements all three typically saves $400 to $800 annually compared to someone who accepts their current policy without review. That’s money that stays in your pocket instead of flowing to an insurer counting on your inertia.

Pull out your current policy and identify which discounts you’re actually receiving versus which ones you qualify for but haven’t claimed. Check whether your safety course completion certificate is on file, confirm your bundling status, and verify that your agent asked about riding experience, homeownership, military service, and group memberships. Contact us at https://lesliekays.com to review your current policy and see what you’re actually leaving on the table with your rider motorcycle insurance discounts.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.