RV insurance quotes vary wildly between carriers, and most riders don’t realize how much money they’re leaving on the table by settling for the first option. The difference between a bare-bones policy and comprehensive coverage can mean thousands of dollars in unexpected costs when something goes wrong.

At Leslie Kay’s, Inc., we’ve helped countless RV owners cut through the confusion and find policies that actually match their lifestyle. This guide walks you through what matters when comparing quotes and how to protect your investment.

Why Price Varies So Much Between Carriers

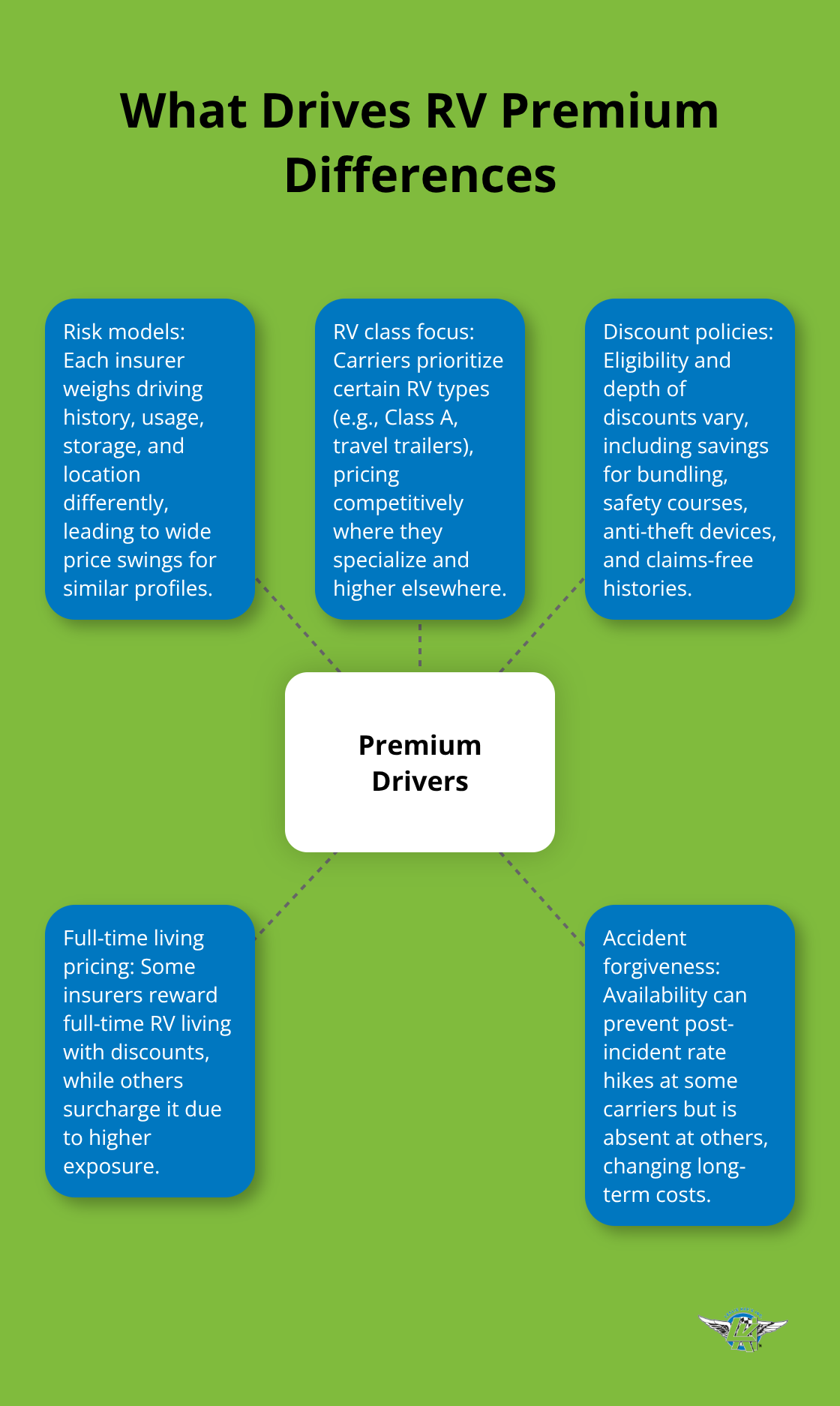

How Insurers Calculate Your RV Premium

RV insurance premiums swing dramatically depending on which carrier you choose. A Good Sam Insurance Agency survey of policies underwritten by National General Group from January through June 2025 found that average monthly premiums for new travel trailer and motorhome policies varied substantially across carriers, with some riders paying 40 percent more than others for nearly identical coverage. The difference stems from how each insurer calculates risk, which RV classes they prioritize, and what discounts they offer. Some carriers heavily discount full-time RV living while others charge premiums for it. Some offer accident forgiveness that prevents rate increases after an at-fault incident, while others don’t.

Bundle Discounts Create Major Price Gaps

Some insurers apply substantial discounts for bundling your RV policy with home, auto, motorcycle, and many other types of insurance, while competitors limit bundle eligibility to specific combinations. This fragmentation means you must obtain quotes from multiple carriers if you want fair pricing. Shopping across carriers reveals what you should actually pay rather than accepting the first option presented to you. The real cost of settling for the first quote you receive could easily exceed hundreds of dollars annually.

Why Multiple Quotes Matter More Than You Think

Getting quotes from multiple carriers isn’t optional-it’s the only way to know what you should actually pay. Each insurer weights risk factors differently, applies discounts inconsistently, and structures deductibles in ways that dramatically affect your final premium. One carrier might offer superior rates on Class A motorhomes while another specializes in travel trailers. Another might reward riders who complete safety courses or own anti-theft devices. Without comparison shopping, you never discover which carrier aligns best with your specific RV type and riding habits.

Coverage Gaps Create Serious Financial Exposure

Coverage gaps create far more serious consequences than overpaying premiums. Many RV owners discover too late that their policy doesn’t cover personal belongings stored inside the RV, emergency expenses after a breakdown, or damage to permanently attached equipment like awnings and satellite dishes. Full-time RV living requires specific protections that standard policies don’t include, and rental RVs need entirely different coverage than owned units. Deductibles matter more than most riders realize-choosing a higher deductible saves money on premiums but leaves you responsible for more out-of-pocket costs when something happens.

Liability Limits and Real-World Protection Needs

Liability limits vary by state minimum requirements, but those minimums often fall short of actual protection you need. One accident involving another vehicle or property damage can expose you to tens of thousands in personal liability. Shopping multiple quotes forces you to examine what’s actually covered versus what you assumed was included, which is how coverage gaps get identified and fixed before disaster strikes. This comparison process reveals whether your current or prospective policy protects your belongings, covers emergency lodging after a breakdown, and includes adequate liability protection for the risks you actually face on the road.

What to Compare in Your RV Insurance Quotes

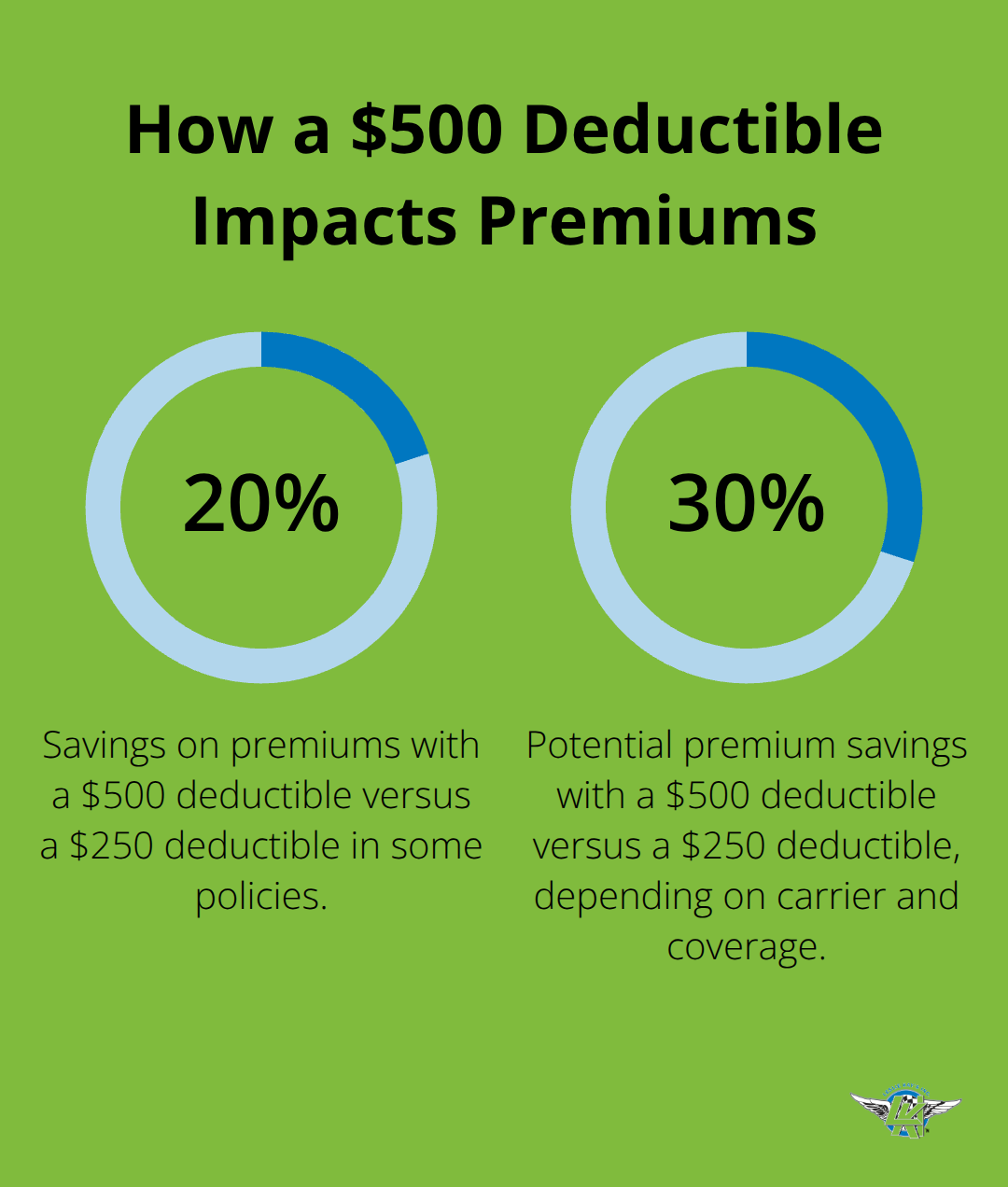

Liability coverage protects you when your RV causes injury or property damage to someone else, and state liability coverage minimums are dangerously low. Most states require only $30,000 for injury or death to one person, $60,000 for injury or death to more than one person, and $15,000 for property damage, which barely covers a single serious accident. A collision involving another vehicle or property can easily exceed 100,000 dollars in damages, leaving you personally responsible for the gap. Physical damage coverage-collision, comprehensive, and specialized protections-determines what happens when your RV is damaged, stolen, or destroyed. Collision covers accidents you cause or are involved in, while comprehensive handles theft, fire, water damage, and falling objects. The real question isn’t whether these coverages exist; it’s whether your deductible is set at a level you can actually afford when a claim happens. A 500-dollar deductible saves you 20 to 30 percent on premiums compared to a 250-dollar deductible, but that math only works if you have 500 dollars available when disaster strikes.

Permanent Attachments and Personal Belongings Need Specific Coverage

Most RV owners don’t realize their base policy excludes damage to awnings, satellite dishes, antennas, and other permanently attached equipment. Custom equipment coverage must be added separately, and many riders skip it to save money-then regret it when an awning tears during a storm or a satellite dish breaks. Personal effects coverage protects electronics, appliances, clothing, and gear stored inside your RV, which standard policies often limit or exclude entirely.

Full-Time Living Demands Additional Protections

Full-time RV living requires additional protection that part-time owners don’t need, including emergency expense coverage for lodging and meals if your RV becomes uninhabitable after an accident. This coverage typically pays 100 to 300 dollars daily and covers costs while your RV is being repaired, which matters far more when your RV is your actual home. Travel trailers and fifth wheels may not require separate motorized RV policies depending on your state, but rental RVs demand entirely different coverage structures than owned units.

Deductible Structures Vary Across Policies

When you compare quotes, demand clarity on what your deductible applies to-some policies use one deductible for collision, another for comprehensive, and separate limits for personal property and emergency expenses. The cheapest quote often excludes protections you didn’t know you needed until you needed them. Understanding these distinctions before you purchase a policy prevents costly surprises when you file a claim, which is why comparing multiple quotes across different carriers reveals what protection actually costs versus what you assumed was included.

Why Shopping Multiple Carriers Matters More Than Speed

Comparing RV insurance quotes across different carriers takes time, but the financial payoff justifies every minute spent. Most riders contact one or two insurers, receive quotes, and move forward without realizing they’re potentially overpaying by hundreds of dollars annually. The problem intensifies when you own multiple vehicles-an RV plus a motorcycle, for example. Standard auto insurance carriers often exclude or severely limit motorcycle coverage, while many insurers that specialize in motorcycles don’t offer competitive RV rates. This fragmentation forces you to either accept mediocre pricing on one vehicle or juggle policies across multiple companies.

How Independent Agencies Eliminate the Legwork

Independent agencies that represent multiple carriers pull quotes from their entire network, identify which insurers offer the best rates for your specific situation, and explain why one policy costs more than another. A Good Sam Insurance Agency survey from January through June 2025 found that average monthly premiums for new travel trailer and motorhome policies varied substantially across carriers-some riders paid 40 percent more than others for nearly identical coverage. That variance doesn’t disappear when you shop alone; it only becomes visible when you actually compare quotes. This approach also reveals which carriers offer the discounts that actually apply to your circumstances-some reward safety course completion, others discount anti-theft devices, and still others offer accident forgiveness that prevents rate increases after at-fault incidents.

Customization and Support Beyond Quote Comparison

The real advantage of working with an independent agency extends beyond quote comparison into customization and ongoing support. Full-time RV living requires emergency expense coverage, personal effects protection, and sometimes total loss replacement coverage that standard policies either exclude or severely limit. Rental RVs demand entirely different structures than owned units. Travel trailers and fifth wheels may fall under auto policy coverage in some states but require separate motorized RV policies in others. A carrier that excels at Class A motorhome coverage might offer weak protection for travel trailers. Another insurer might structure deductibles in ways that create unnecessary out-of-pocket costs when you file a claim.

Claims Expertise and Round-the-Clock Support

Independent agencies know these distinctions because they work with multiple carriers daily and understand which insurers handle claims efficiently for RV owners. Seven-day-a-week support matters more than most riders realize-breakdowns and accidents don’t wait for business hours, and when your RV is your home or your adventure platform, you need answers immediately. An agency built for RV owners understands the unique risks that you face, from extended travel in unfamiliar territory to full-time living situations where your RV is your primary residence (this expertise translates into policies that actually protect your investment rather than policies that look comprehensive on paper but leave critical gaps when claims happen).

The Financial Reality of Comparison Shopping

The initial time investment in comparing multiple quotes across carriers pays dividends through lower premiums, better coverage alignment, and faster claims resolution when you need it. Without direct comparison, you never know which discounts you qualify for or which carrier prioritizes your RV class. Independent agencies eliminate the guesswork by presenting side-by-side comparisons of what each insurer charges for your exact RV type, driving record, and usage patterns.

Final Thoughts

Comparing RV insurance quotes across multiple carriers saves thousands of dollars over the life of your policy. A Good Sam Insurance Agency survey from January through June 2025 found that some riders paid 40 percent more than others for nearly identical coverage, which means the difference between a quick quote and a thorough comparison could easily exceed 500 dollars annually. That financial advantage compounds year after year, especially when you factor in the coverage gaps that emerge only when you examine policies side by side.

Biker-friendly agencies understand RV-specific risks in ways that standard insurance brokers simply don’t. They recognize that full-time RV living demands emergency expense coverage, that travel trailers need different protection than Class A motorhomes, and that riders who own both motorcycles and RVs face unique bundling challenges. These agencies work with multiple carriers daily, which means they know which insurers handle claims efficiently for RV owners, which ones offer accident forgiveness that prevents rate increases after at-fault incidents, and which carriers actually reward safety course completion with meaningful discounts.

We at Leslie Kay’s, Inc. shop multiple carriers to deliver customized policies built around your specific RV lifestyle and handle claims with hands-on support. Whether you own a travel trailer, fifth wheel, or motorhome, or you’re juggling RV and motorcycle coverage, get RV insurance quotes from Leslie Kay’s, Inc. and discover what your coverage should actually cost.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.