Boat owners often face a tough choice: pay for insurance year-round or risk coverage gaps when their boat sits idle. At Leslie Kay’s, Inc., we’ve seen firsthand how the right seasonal boat insurance coverage strategy saves money while keeping your vessel protected.

The key is matching your policy to your actual boating schedule, not a one-size-fits-all approach. This guide walks you through the options that work.

Why Seasonal Coverage Protects Your Wallet

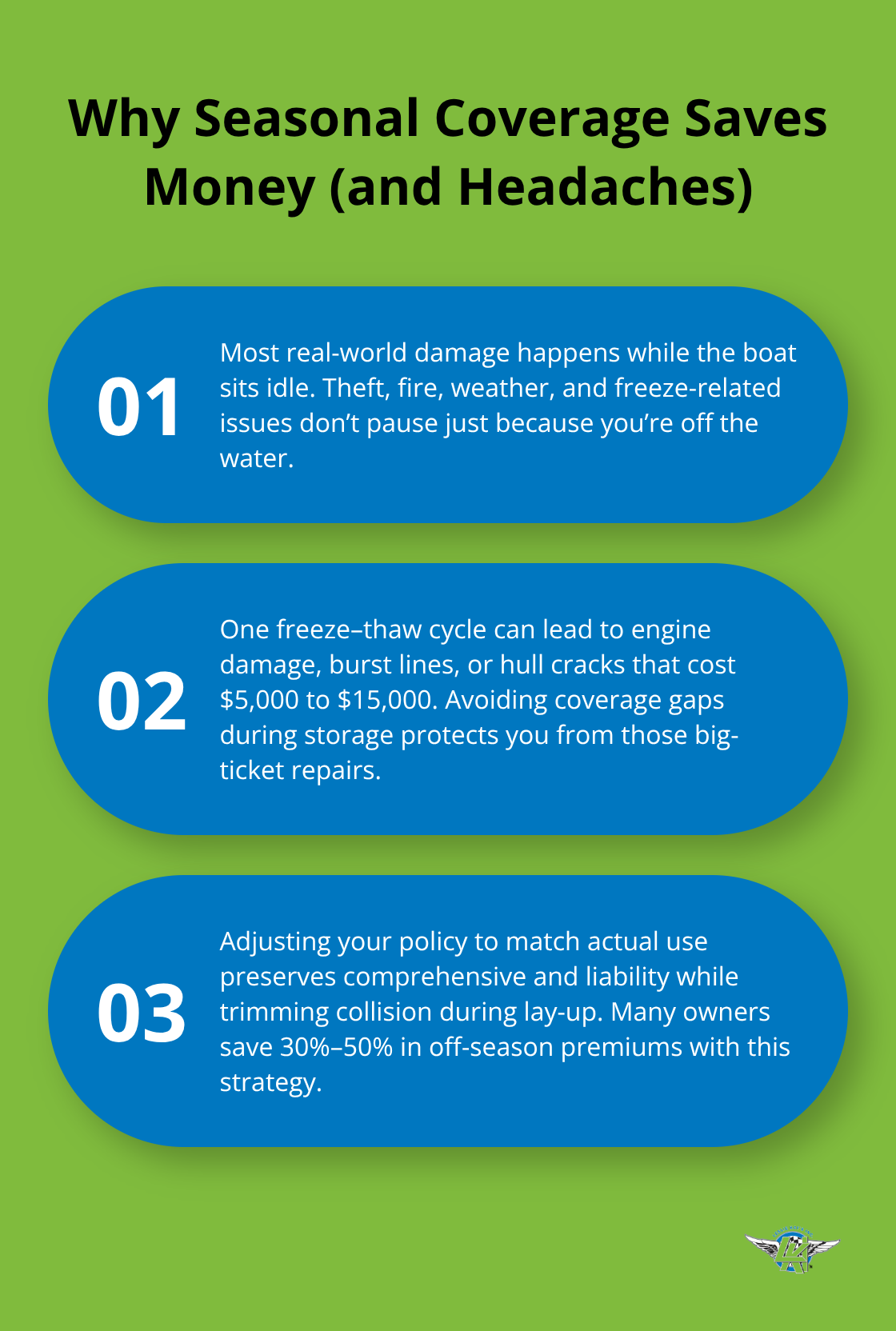

Most boat owners think year-round insurance is mandatory, but that’s not the full picture. The real issue is that your boat faces genuine risks even when you’re not using it-theft, fire, weather damage, and freeze-related destruction happen during storage, not just on the water. According to U.S. Coast Guard 2024 data, boating incidents resulted in over 550 deaths, about 2,200 injuries, and $88 million in property damage, but that’s only part of the risk equation. The other part involves what happens in your marina slip or storage facility when you’re not aboard. Without proper coverage during the off-season, a single freeze-thaw cycle can destroy your engine, burst water lines, or crack the hull-repairs that easily exceed $5,000 to $15,000. This is where strategic seasonal coverage becomes essential. Instead of canceling your policy when you store the boat, you adjust it to match your actual usage pattern.

This approach keeps you protected while reducing premiums by suspending collision coverage and lowering limits on active-use components, typically saving 30 to 50 percent during lay-up periods depending on your storage location and boat type.

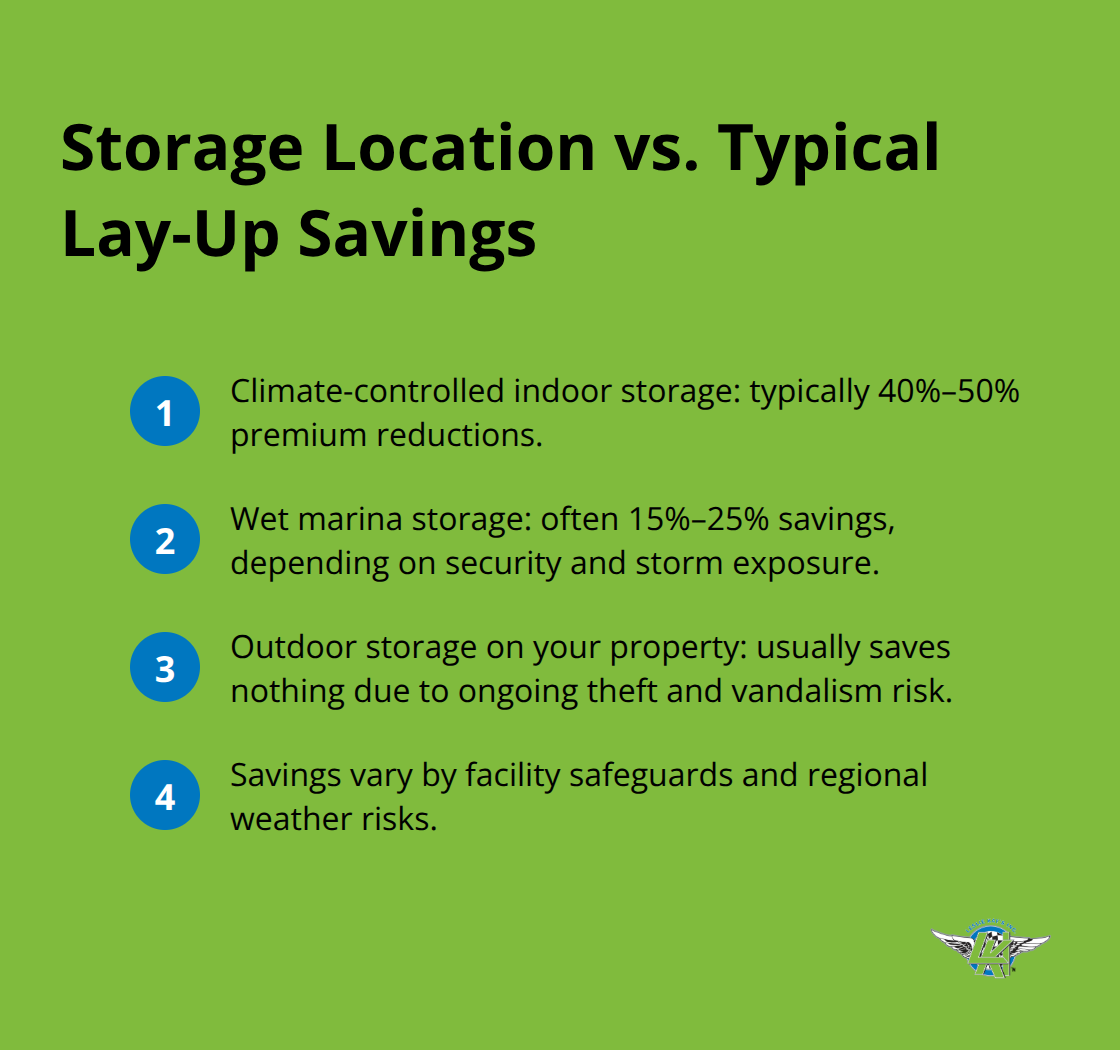

Storage location determines your savings potential

Where you store your boat directly impacts what discount you receive. Climate-controlled indoor storage offers the biggest premium reductions because it eliminates freeze damage, theft exposure, and weather risks. Covered outdoor storage provides moderate savings, while wet storage at a marina depends entirely on facility security and storm exposure in your region. If you store your boat on your property outdoors, expect minimal discounts because theft and vandalism remain real threats. A marine specialist who understands your specific storage setup can tailor your lay-up period and coverage adjustments to your exact situation rather than applying a generic formula. Many boat owners make the mistake of keeping collision coverage active during storage when they should focus on maintaining comprehensive coverage, theft protection, and liability instead.

Winterization requirements affect your claims

Improper winterization is a leading cause of costly spring repairs, and most insurers require proof of winterization before they’ll pay freeze-damage claims. This means you need documentation showing that you changed the oil, fogged the cylinders, stabilized the fuel, drained fresh water systems, and circulated non-toxic antifreeze through all relevant components. Take photos of the entire winterization process-this documentation speeds up claims processing and validates that you took reasonable steps to prevent damage. Without this proof, you’re fighting with your insurer when something goes wrong, and you might lose.

The next step involves understanding which coverage types actually work for your boat and your boating habits.

Which Coverage Types Actually Work During Storage and Active Boating

Active-season policies cover your boat only during the months you actually use it, typically May through September depending on your region. These policies maintain full collision and comprehensive coverage while your boat is on the water, protecting against accidents, weather damage, and theft during peak-use periods. The advantage is straightforward: you pay only for the protection you need when you need it. However, many boat owners make a critical mistake here. They assume active-season coverage includes storage protection, but most carriers suspend or severely limit collision coverage the moment your boat leaves the water. This creates a dangerous gap. If a spring storm damages your boat in April while it’s still in storage, collision won’t cover it because the policy technically ended in fall. You need comprehensive coverage active year-round to handle these risks, even if collision coverage is suspended during lay-up.

How lay-up coverage adjusts your protection

Storage and lay-up coverage operates differently than active-season policies. Instead of canceling your policy entirely, you adjust it to reflect that your boat isn’t being used for active recreation. Comprehensive coverage remains active to protect against theft, fire, and weather damage while your boat sits in storage. Liability coverage also stays in place because someone could still be injured near your stored vessel. What you suspend or reduce is collision coverage, since collisions cannot happen when the boat isn’t moving. This adjustment typically saves 30 to 50 percent on premiums during your off-season months.

Flexible lay-up periods match your schedule

The lay-up period itself is negotiable with your insurer. Most carriers offer flexible start and end dates rather than locking you into November-to-March coverage. If your boating season runs March through October, you can set your lay-up period for November through February. This flexibility matters because it aligns your coverage costs with your actual usage patterns. Contact your marine specialist before your storage season begins, not after. Setting up the lay-up adjustment in advance prevents accidental lapses in coverage and ensures your comprehensive protection activates on schedule.

Freeze-damage coverage requires winterization proof

Freeze-damage coverage deserves special attention here. Standard comprehensive policies typically exclude damage from freezing water expansion unless you add a specific freeze-damage rider. This rider requires proof of proper winterization, which ties directly back to the steps you took before storage. The cost of adding freeze-damage coverage is minimal compared to the risk of engine block cracks or burst water lines. Insurers require this documentation because improper winterization is a leading cause of costly spring repairs, and they want assurance that you took reasonable steps to prevent damage.

Understanding your coverage options is only half the battle. The next step involves assessing your specific boating habits and comparing what different carriers actually offer for your boat and storage situation.

Matching Your Boat to the Right Coverage Plan

Choosing seasonal coverage requires honest answers about how you actually use your boat, not how you wish you used it. Most boat owners either over-insure during storage months or under-insure during peak season, both mistakes that cost money. Track your boating activity for the past two years. Count the actual days you spent on the water, the months when your boat sat idle, and the storage conditions during those idle periods. If you launch in May and haul out in October, that’s five months of active use and seven months of storage. Your coverage should reflect this reality, not some idealized version of year-round boating.

Storage location determines your savings potential

Once you know your actual schedule, contact marine specialists who understand your region’s seasonal patterns. They can calculate whether a lay-up adjustment saves more money than a straight annual policy, and they’ll know if your storage location qualifies for climate-controlled discounts. Climate-controlled indoor storage typically generates 40 to 50 percent premium reductions during lay-up, while wet marina storage might only save 15 to 25 percent depending on facility security and local storm exposure. Outdoor storage on your property usually saves nothing because theft and vandalism remain constant threats. This is where most boat owners waste money-they assume all storage is equal, but it isn’t.

What carriers actually cover during lay-up

Comparing carriers requires looking at what they actually cover during lay-up, not just the quoted price. Some insurers maintain full comprehensive and liability coverage during storage while suspending only collision, while others reduce comprehensive limits or exclude freeze damage entirely unless you pay extra. Request detailed quotes from at least three carriers that specialize in marine coverage, because standard auto insurers often handle boat policies poorly. Ask each carrier specifically what happens to your coverage on November 1st when you activate lay-up, and get their answer in writing. Ask whether freeze-damage coverage is included or an add-on, and what winterization documentation they require. Ask if they offer discounts for safety courses, security systems like GPS trackers, or bundling with auto or home policies.

Deductible decisions and financial tolerance

When comparing deductibles, don’t automatically choose the lowest option. A $500 deductible costs more in premium than a $1,000 deductible, but if your boat is worth $35,000 and sits in outdoor storage where theft is a real risk, that extra premium might be worth it. During lay-up when collision is suspended, your deductible only applies to comprehensive claims like theft or weather damage, so the cost difference shrinks. The real decision point is your financial tolerance: can you absorb a $1,000 loss if your boat is damaged in storage, or does that create hardship? If hardship results, pay for the lower deductible. If you can handle it, take the higher deductible and redirect those premium savings toward freeze-damage coverage or indoor storage instead.

Final Thoughts

Seasonal boat insurance coverage works because it matches your protection to your actual boating reality, not an imaginary year-round schedule. Your boat faces genuine risks during storage that require comprehensive and liability coverage year-round, even when collision coverage is suspended. Storage location determines your savings potential more than any other factor, so climate-controlled indoor storage delivers the biggest premium reductions during lay-up periods.

Track your actual boating activity over the past two years and count the months you spend on the water versus idle storage time. Contact a marine specialist who understands your region’s seasonal patterns and storage conditions, then request detailed quotes from at least three carriers. Compare deductibles based on your financial tolerance, set your lay-up period in advance, and take photos of your winterization process to speed claims if damage occurs.

We at Leslie Kay’s, Inc. specialize in watercraft coverage and shop multiple carriers to deliver customized policies that fit your actual boating schedule and budget. Contact us to get a quote tailored to your boat, storage location, and boating habits-year-round peace of mind starts with coverage that actually matches how you use your boat.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.