Motorcycle riders face unique insurance challenges that standard auto policies simply don’t address. At Leslie Kay’s, Inc., we know that comprehensive motorcycle insurance coverage protects you against the unexpected-from theft and weather damage to collisions with animals.

This guide walks you through what comprehensive coverage actually includes, which risks matter most to riders, and how to pick the right limits for your situation.

What Comprehensive Coverage Actually Protects

Comprehensive motorcycle insurance is a coverage option you add to your policy that pays for damage to your bike from non-collision events. Riders often confuse what comprehensive covers with what it doesn’t, and that confusion leads to expensive mistakes. Comprehensive handles theft, vandalism, fire, weather damage (including hail and flooding), and collisions with animals. It does not cover accidents where you hit another vehicle or object, normal wear and tear, or damage from negligence. The payout is based on your motorcycle’s actual cash value at the time of the loss, minus your chosen deductible. If your bike is worth $5,000 and you have a $500 deductible, comprehensive pays up to $4,500 for a covered loss.

How Deductibles Affect Your Premium and Out-of-Pocket Costs

Deductibles typically range from $250 to $2,000, and your choice directly lowers your annual premium. Raising your deductible from $250 to $1,000 can save you $100 to $300 per year, depending on your bike and location. This trade-off matters because understanding your actual risk tolerance matters more than picking the lowest price. You pay the deductible out of pocket when you file a claim, so a higher deductible means lower premiums but higher costs if damage occurs. The math works differently for every rider-someone who parks their bike in a secure garage faces different risks than someone who leaves it on the street.

When Your Lender Makes Comprehensive Mandatory

If you financed or leased your motorcycle, your lender requires comprehensive coverage to protect their investment in the bike. You don’t have a choice here. But if you own the bike outright, comprehensive is optional by law in every state. The real question is whether you could afford to replace or repair your motorcycle without financial hardship if theft or weather damage occurred. Newer bikes and higher-value motorcycles benefit most from comprehensive because the potential loss is larger. A $15,000 adventure bike stolen from your driveway hits differently than a $3,000 used cruiser.

Weather Damage and Regional Risk Factors

Weather damage is increasingly relevant for riders in areas prone to hail, heavy rain, or flooding. Georgia’s peak severe thunderstorm season is March, April and May, with a secondary peak that may occur during September and October. Your location determines how much weather risk you actually face, and that should influence your coverage decision.

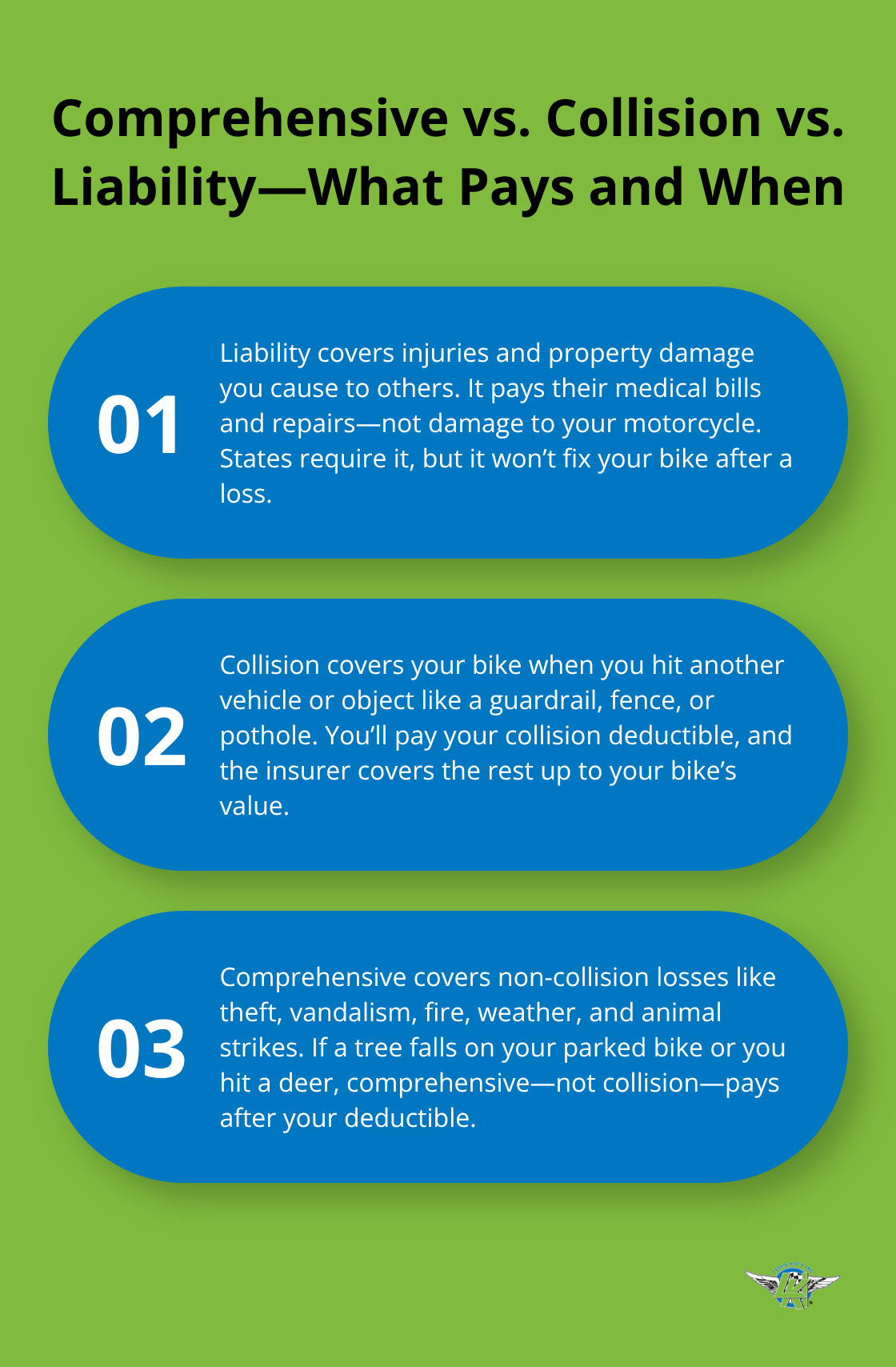

How Comprehensive Stacks Against Other Coverage Types

Liability coverage, which every state requires, pays for injuries and property damage you cause to others. It protects their medical bills and vehicle repairs, not yours. Collision coverage handles damage when your bike hits another vehicle or object like a fence or pothole. Comprehensive handles everything else that isn’t a collision. They work together in what’s called full coverage. If a tree falls on your parked bike during a storm, comprehensive pays. If you swerve to avoid that tree and crash into a guardrail, collision pays. If you hit a deer on the highway, comprehensive covers it because it’s an animal collision, not a regular collision.

Understanding this distinction prevents claim denials and ensures you have the right protection for the risks you actually face as a rider. Now that you know what comprehensive covers, the next step is assessing whether your specific situation calls for this protection.

Why Theft and Weather Matter Most to Motorcycle Owners

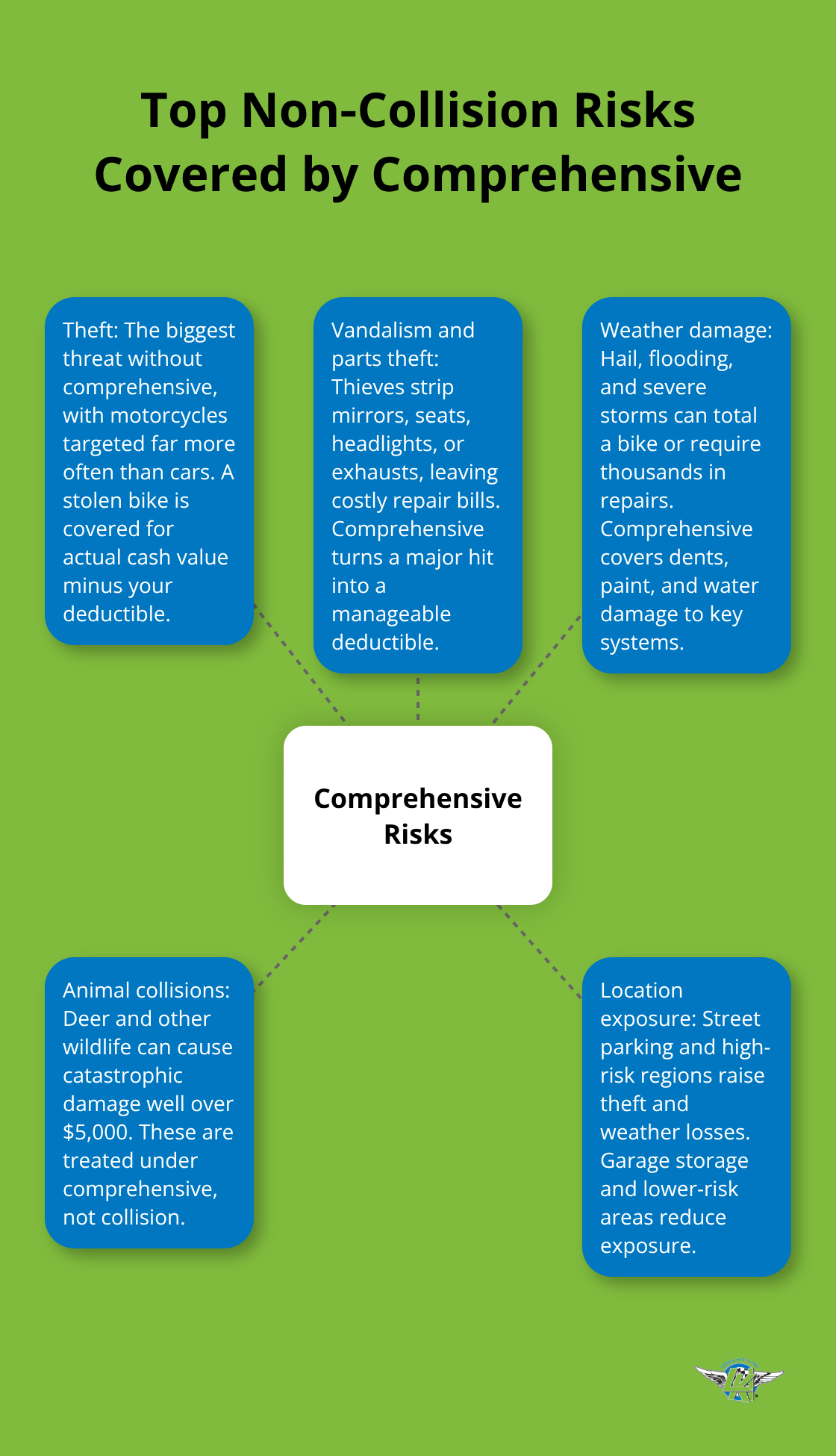

Theft ranks as the single biggest threat to motorcycle owners who lack comprehensive coverage. The National Insurance Crime Bureau reported that motorcycles face theft rates five times higher than cars. A bike parked in your driveway, even in a residential neighborhood, faces real risk. Comprehensive coverage pays the actual cash value of your motorcycle minus your deductible if a thief steals it and never recovers it, which means an $8,000 bike with a $500 deductible nets you $7,500 to replace it. Without comprehensive, you absorb the full loss yourself.

Vandalism and Parts Theft Cost Riders Thousands

Vandalism follows theft as the second reason riders file comprehensive claims. Thieves don’t always steal entire motorcycles; they strip parts like mirrors, seats, headlights, and exhaust systems instead. A single night of vandalism can cost $1,500 to $3,000 in parts and labor, and comprehensive covers those repairs.

This risk intensifies for riders who park on streets or in unsecured lots where thieves operate with minimal interference. Comprehensive protection transforms a catastrophic financial hit into a manageable deductible payment.

Weather Damage Hits Harder Than Most Riders Expect

Weather damage ranks equally serious but often gets overlooked by riders who assume their bikes face minimal exposure. Hail storms cause severe denting and paint damage that repair shops charge $2,000 to $5,000 to fix on a motorcycle, since custom bodywork demands specialized labor. If you live in regions that experience frequent hail, flooding, or severe storms, comprehensive protection becomes essential rather than optional. Riders in Texas, Oklahoma, and Kansas face significantly higher hail risk than those in coastal regions. Flooding presents another serious concern; comprehensive covers water damage to engines, electrical systems, and frames when your bike sits in heavy rain or flash floods. Without comprehensive, a flooded motorcycle becomes a total loss you pay for yourself. A motorcycle stored outside or parked on a street during monsoon season in Arizona or intense hurricane seasons in Florida faces damage that costs thousands to repair.

Animal Collisions Demand Separate Coverage Consideration

Animal collisions happen more frequently than most riders realize, especially on rural roads and highways. Hitting a deer, elk, or moose at highway speeds causes catastrophic damage-broken frames, destroyed fairings, and engine damage that easily exceeds $5,000 in repairs. Comprehensive classifies animal collisions separately from regular collisions, meaning your comprehensive deductible applies instead of your collision deductible. This distinction matters because you might choose a $1,000 comprehensive deductible and a $250 collision deductible, saving money on the more common animal strike scenario. Riders who regularly travel rural routes, commute through areas with wildlife crossings, or live near forests should absolutely carry comprehensive coverage for this reason alone.

Your Location Determines Your Real Risk Profile

Your location determines whether weather damage and animal strikes represent genuine threats or theoretical concerns. Regional patterns shape which risks demand immediate attention and which ones remain unlikely in your specific area. Understanding your actual exposure-not just national statistics-helps you make coverage decisions that protect your bike and your wallet. The next step involves assessing your motorcycle’s value and determining which deductible levels align with your financial situation and risk tolerance.

Matching Coverage to Your Bike’s Real Value

The biggest mistake riders make is choosing comprehensive coverage based on what they paid for their motorcycle rather than what it’s actually worth today. If you bought your bike three years ago for $8,000, it’s not worth $8,000 anymore-it’s worth whatever someone would pay for it right now in its current condition. Comprehensive pays your motorcycle’s actual cash value at the time of loss, minus your deductible, which means overestimating your bike’s value wastes money on premiums you don’t need. Check current market listings for your exact model, year, and mileage on sites like CycleTrader or local classified ads to establish a realistic baseline. A 2021 Harley-Davidson Street 750 in good condition might be worth $6,500 today, not the $7,500 you paid in 2021. Setting your coverage limit to match that $6,500 value prevents you from paying premiums to protect money you won’t actually receive.

How Deductibles Control Your Actual Costs

Your deductible choice becomes the real lever for controlling costs. If your bike is worth $6,500 and you choose a $500 deductible, the maximum comprehensive will ever pay you is $6,000. Jumping to a $1,000 deductible typically saves $80 to $150 annually on comprehensive premiums alone, which adds up to $400 to $750 over five years. That savings makes sense if you could comfortably pay $1,000 out of pocket after theft or weather damage; it makes no sense if a $1,000 unexpected expense would strain your finances. Financed bikes require lenders’ minimum deductible requirements, often $500 or $1,000, so check your loan documents before shopping.

Getting Real Quotes From Multiple Carriers

Once you know your bike’s value and your deductible comfort zone, comparing actual quotes from multiple carriers reveals which insurers price your specific risk profile most competitively. Progressive, Allstate, and other carriers price identical coverage differently based on their underwriting models. A $6,500 cruiser with a $500 deductible might cost $180 annually with one carrier and $240 with another-that $60 difference matters across multiple years. Requesting quotes from at least three insurers takes 15 minutes online and shows you the real price range for your situation rather than relying on averages you find in articles. Compare the declarations page line-by-line to confirm deductibles, coverage limits, and any exclusions match across quotes. Some carriers exclude flood coverage in certain states, while others cover it automatically, so verification prevents claim surprises later.

Risk Factors That Shape Your Premium

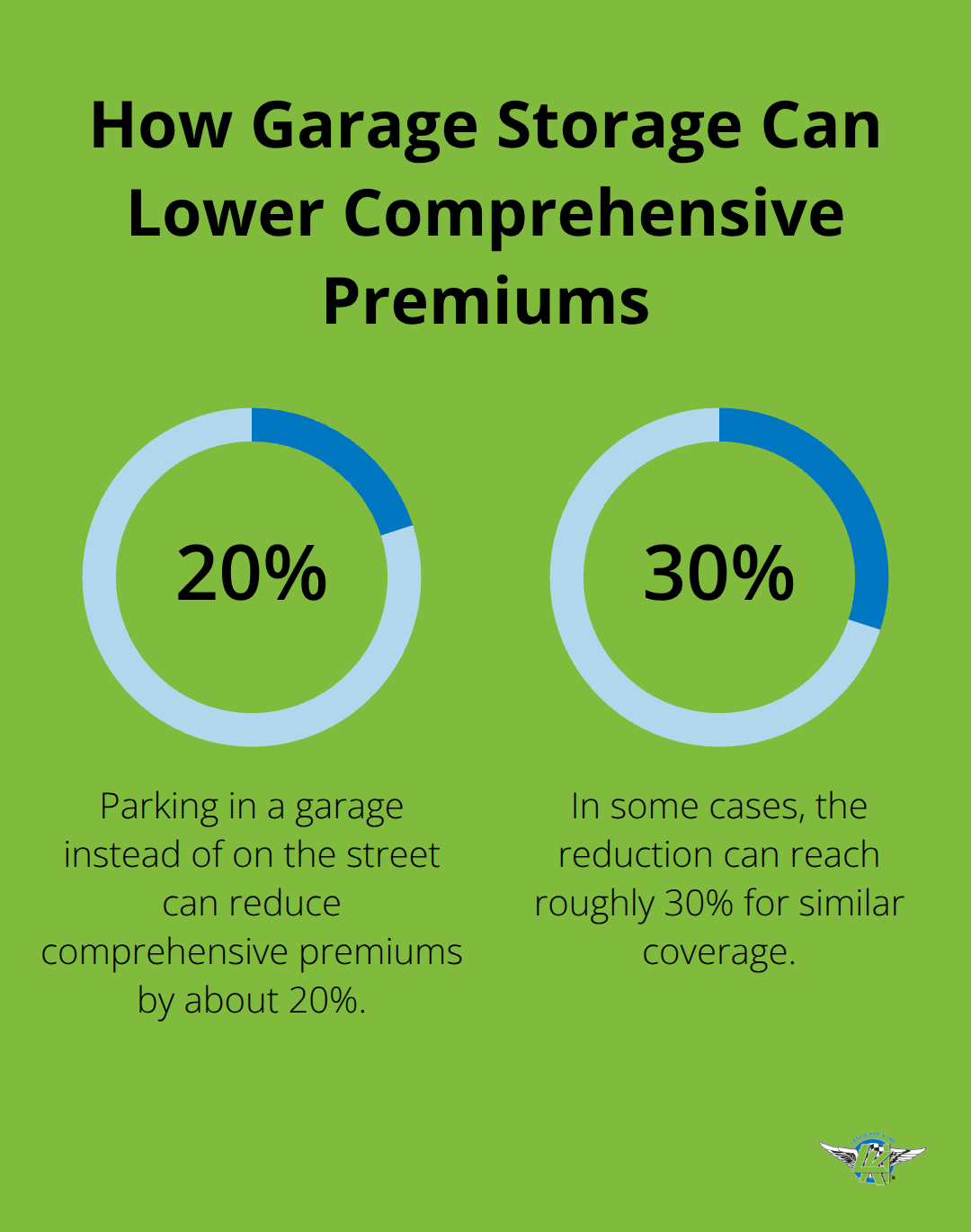

Your actual cost also depends on where you park your bike, your annual mileage, and your riding history. A bike parked in a garage overnight faces dramatically lower theft and weather risk than one left on a street, which can reduce comprehensive premiums by 20 to 30 percent. Riders who commute 500 miles monthly pay higher premiums than weekend-only riders because exposure increases risk.

A clean riding record lowers rates significantly, while accidents or violations increase them (these factors mean your neighbor’s premium for identical coverage tells you nothing about what you’ll actually pay). Getting custom motorcycle insurance rates tailored to your specific bike and riding style ensures you’re not overpaying for coverage that doesn’t match your actual risk.

Final Thoughts

Comprehensive motorcycle insurance coverage protects you against theft, weather damage, vandalism, and animal collisions that standard liability coverage ignores. Your decision hinges on three factors: your motorcycle’s actual cash value today, your ability to absorb an out-of-pocket loss, and the specific risks your location and riding habits create. A $15,000 adventure bike parked on a street in a theft-prone neighborhood demands different protection than a $4,000 used cruiser stored in a secure garage.

Getting real quotes from multiple carriers matters far more than relying on national averages or what your friend pays for identical coverage. Compare declarations pages line-by-line to confirm deductibles, limits, and exclusions match across quotes, and verify whether your lender requires specific deductible minimums if you financed your bike. Calculate whether the annual premium savings from raising your deductible outweigh the risk of paying a larger amount out of pocket after damage occurs.

Contact Leslie Kay’s, Inc. today to get a personalized quote that reflects your specific situation and protects what matters to you on the road. We shop multiple carriers to find customized policies that match your actual bike, riding style, and location rather than forcing you into generic coverage. Our hands-on support means you get real people who understand motorcycles when you need help most.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.