Motorcycle insurance isn’t one-size-fits-all, and your rates shouldn’t be either. At Leslie Kay’s, Inc., we know that every rider has different needs based on their experience, bike, and riding habits.

Custom motorcycle insurance rates reflect what actually matters for your specific situation. This guide walks you through what impacts your premiums and how to get coverage that fits your ride.

What Shapes Your Insurance Premiums

Your insurance cost depends on three major factors that insurers assess differently, and understanding each one helps you anticipate what you’ll pay. Your riding experience matters significantly-riders under 25 typically pay substantially more than experienced riders, and a single speeding ticket or at-fault accident can push premiums higher for years. The type and value of your motorcycle directly influences your rate because sport bikes and high-performance models cost more to insure than cruisers or touring bikes, while custom motorcycles with higher values require more expensive coverage. Where you ride and store your bike affects theft risk and accident exposure; urban riders face higher theft rates and dense traffic conditions, while rural riders encounter higher speeds and different hazards. State location matters too, since minimum coverage requirements and theft statistics vary widely-some states require higher bodily injury and property damage limits, which increases your baseline premium.

Your Experience and Riding Habits

Insurers examine your driving history across both cars and motorcycles because they reveal your risk profile. A clean record without tickets or claims signals responsibility and typically qualifies you for lower rates, while multiple incidents suggest higher risk and result in premium increases. Riders who complete an approved motorcycle safety course often qualify for discounts because formal training demonstrates commitment to safe riding. How frequently you ride affects your accident exposure-daily commuters who spend more time in traffic face higher accident risk than weekend recreational riders, which can push premiums higher. Harley-Davidson Insurance Services recognizes experienced riders with discounts that reward longer tenure on motorcycles, acknowledging that seasoned riders statistically cause fewer claims.

Your Bike’s Type and Custom Modifications

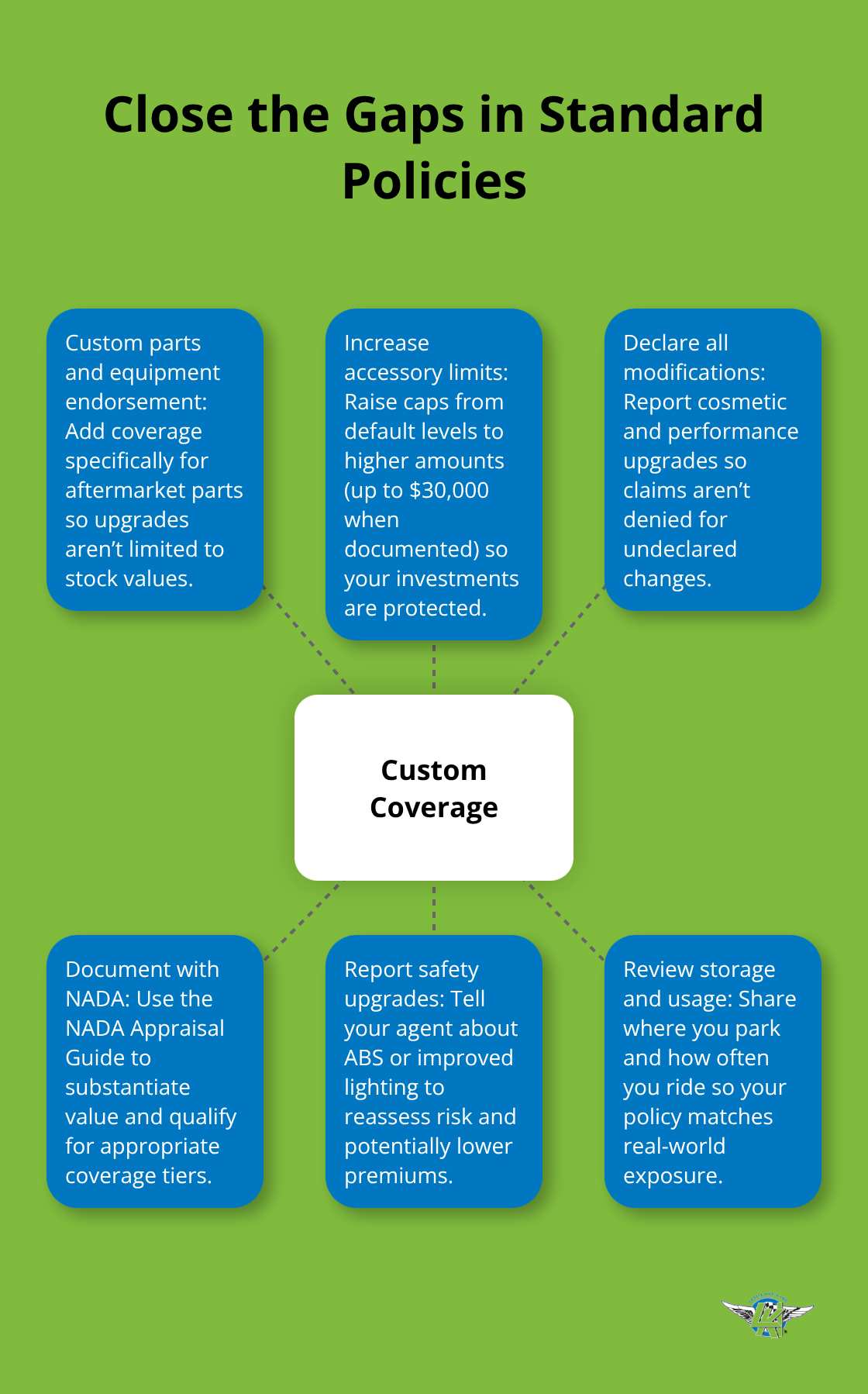

The motorcycle itself represents a major cost factor because insurers calculate replacement and repair expenses based on the bike’s market value and repair costs. Custom bikes require special attention because modifications change the replacement value and may not be covered under standard policies. If your custom motorcycle appears in the NADA Appraisal Guide, you can access comprehensive coverage including accessory and custom parts protection up to $3,000 for bikes under 25 years old, with optional increases to $30,000. Undeclared modifications create serious problems-insurers may deny claims if they discover upgrades you didn’t report, leaving you to pay out-of-pocket after an incident. Safety upgrades like anti-lock brakes or improved lighting can actually lower your premiums because they reduce accident risk, while performance enhancements that boost horsepower typically raise costs due to increased crash potential.

Storage Location and Riding Environment

Where you park your motorcycle significantly impacts your premium because secure storage dramatically reduces theft and weather damage risk. A locked garage provides substantially better protection than street parking or open storage, and insurers recognize this difference in their pricing. Urban environments carry higher theft rates and denser traffic, while rural areas present different risks like higher speeds and less police presence. Seasonal riding patterns also matter-limiting seasonal riding and discussing storage-based coverage adjustments with your agent helps manage costs because you reduce actual exposure time. Progressive and other insurers consider state-specific factors including local theft statistics, accident rates, and weather patterns when calculating your individual rate, which is why identical riders in different states pay different premiums for the same coverage.

Moving Beyond Standard Coverage

Standard motorcycle policies often fail to protect custom parts, aftermarket accessories, and performance upgrades that represent significant investments in your ride. Your bike deserves coverage built for its specific needs, not a generic policy that treats all motorcycles the same way. When you work with agents who understand your riding style and bike modifications, you gain access to tailored endorsements and riders that actually protect what matters to you. The next section explores how to lower your costs while maintaining the protection your custom motorcycle requires.

How to Actually Lower Your Motorcycle Insurance Costs

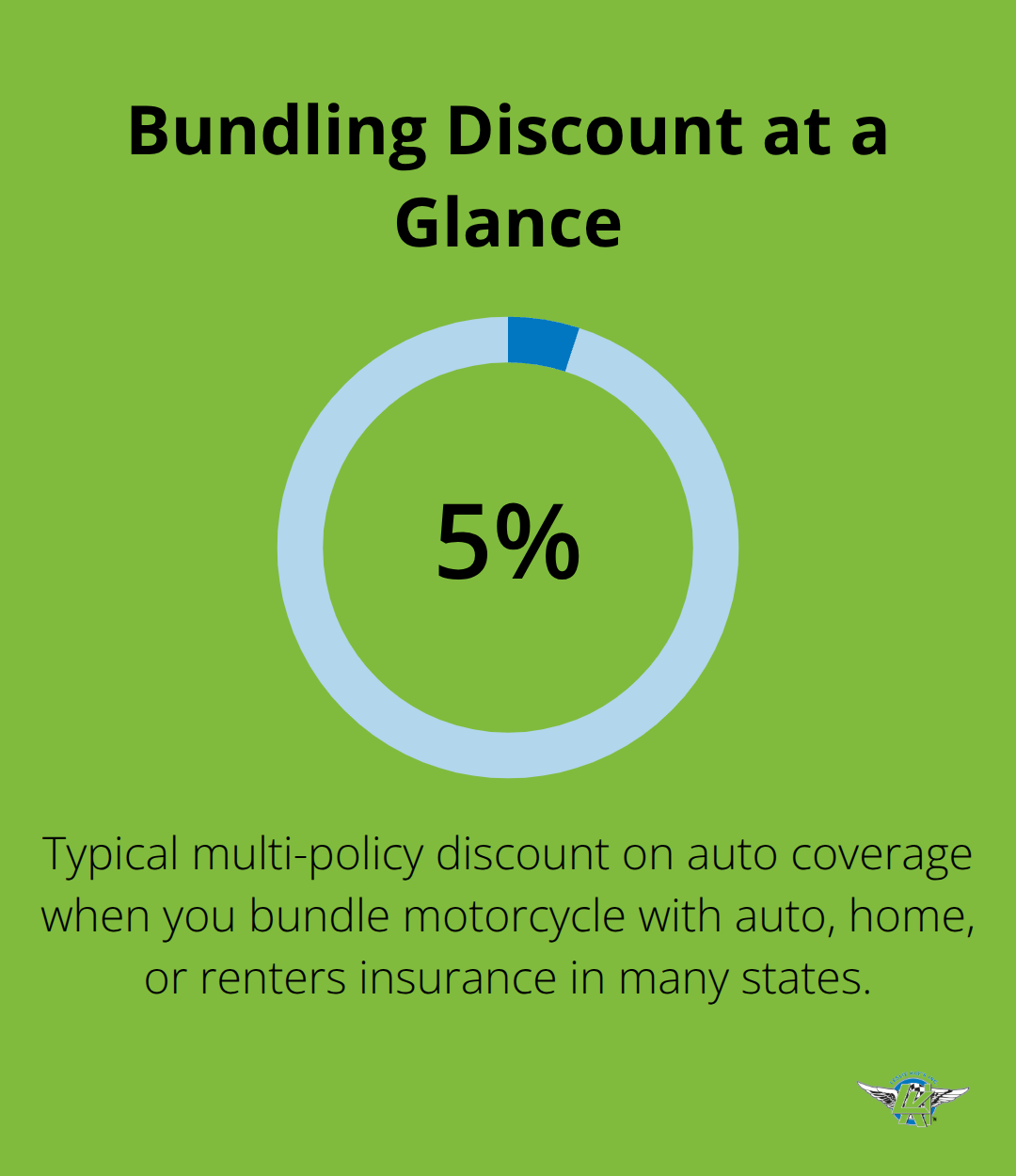

Lowering your motorcycle insurance premium requires action, not just wishful thinking. The most effective strategy combines multiple discount opportunities that stack together-bundling your motorcycle policy with auto, home, or renters insurance typically yields a multi-policy discount around 5% on your auto coverage in many states.

If you insure more than one motorcycle, you qualify for a multi-cycle discount that reduces per-bike costs, making it worth insuring both your primary ride and that vintage restoration project. Harley-Davidson Insurance Services lists 16 distinct discounts, and strategic stacking of three or four of them can meaningfully reduce your annual premium. The paid-in-full discount rewards annual or automatic payment methods, lowering your average monthly cost compared to monthly billing. A claim-free renewal discount applies when you avoid at-fault incidents and don’t file comprehensive claims over $500 in your prior policy period, which directly incentivizes safe riding habits that protect both your wallet and your bike.

Safety Courses Reduce Your Rates

A motorcycle safety course isn’t just about learning technique-it’s about getting insurance companies to lower your rates because formal training demonstrates you take riding seriously. The Motorcycle Safety Foundation and H-D Riding Academy courses qualify for discounts with many carriers. Honda offers a $75 reimbursement for MSF training when you purchase a new motorcycle or scooter. Your agent can confirm which courses your specific insurer recognizes and how much you’ll save by completing one.

Your Driving History Determines Your Premium

Your driving history across both cars and motorcycles matters more than most riders realize because insurers examine the entire picture. A single speeding ticket can increase your premium for years, while a clean record with zero incidents qualifies you for claim-free and clean driving record discounts. Military and law enforcement personnel receive dedicated discounts recognizing their discipline and training. Membership in motorcycle clubs or associations like H.O.G. unlocks rider group discounts that reduce your quote cost simply for joining an organized community.

Transparency Unlocks the Right Discounts

The real power comes from transparency with your agent about your specific situation. When you disclose modifications, discuss your actual riding frequency and routes, and explain storage arrangements, agents can identify which discounts apply to your exact profile rather than guessing. This conversation also ensures your coverage actually protects your custom parts and riding habits instead of leaving gaps that could cost you thousands after an incident. Getting multiple quotes from different insurers is essential because premium variation is substantial-what costs $571 annually with one carrier might cost significantly less with another based on how they weight your individual risk factors and available discounts.

Your next step involves understanding why standard policies fail to protect what you’ve invested in your motorcycle and how custom coverage actually works for riders like you.

Why Standard Policies Leave Gaps in Your Protection

Standard motorcycle policies treat all riders the same way, and that’s exactly the problem. Most generic policies cover basic liability and maybe collision, but they completely miss the reality of custom bikes, performance upgrades, and the specific way you actually ride. When you have $5,000 in aftermarket parts, a turbo kit, or custom paint work, a standard policy doesn’t automatically protect those investments because they fall outside the original bike’s factory specifications. Progressive and other major carriers require you to specifically request custom parts and equipment coverage as an add-on endorsement, which means if you don’t ask for it, you won’t have it. Motorcycle fatality rates and insurance claim outcomes underscore why accurate coverage matters-claims from serious incidents expose gaps in standard policies that leave riders paying thousands out of pocket.

Custom Modifications Fall Outside Standard Coverage

Custom motorcycles that don’t appear in the NADA Appraisal Guide face severe limitations because you can only access liability coverage, leaving comprehensive and collision completely unavailable no matter how much you’re willing to pay. Dairyland Insurance and other carriers structure their base policies around stock motorcycles, forcing you to hunt down the right endorsements yourself. A $1,000 custom paint job increases replacement value, but standard policies often don’t account for custom cosmetic costs in their valuation. Performance enhancements that boost horsepower change your actual crash risk profile, yet insurers typically don’t adjust coverage to match that increased exposure-you need to specifically discuss this with your agent and request appropriate coverage limits.

Accessory Coverage Limits Create Real Shortfalls

Accessory coverage caps at $3,000 for bikes under 25 years old with standard endorsements, which sounds adequate until you realize your custom exhaust system, wheels, and seat alone might cost $4,000 to replace. You can increase this to $30,000 if you request it and document everything in the NADA Guide, but most riders never know this option exists. This gap means your actual investments remain unprotected unless you take action to expand your policy limits.

Safety Upgrades Require Active Communication

Safety-oriented upgrades like anti-lock brakes or improved lighting actually reduce your risk and should lower premiums, yet you need to explicitly tell your agent about these changes so they can reassess your rate. Your agent cannot identify these risk-reducing modifications without your input, which means you miss out on potential savings that should apply to your profile. Each upgrade you add to your bike changes your coverage needs, but your policy stays static unless you actively communicate changes to your carrier.

Transparency Unlocks Proper Protection

The problem compounds when you modify your bike over time without updating your coverage. Standard policies force you into a one-size-fits-all box when your motorcycle doesn’t fit that box at all. We understand that transparency with your agent about modifications, riding frequency, storage location, and your specific riding style matters more than picking the cheapest quote. When you disclose what you’ve actually invested in your motorcycle and how you actually ride it, your agent can build coverage that protects your real situation instead of leaving gaps that could cost you thousands after an incident.

Final Thoughts

Your motorcycle deserves insurance that matches your actual investment and riding reality, not a generic policy built for someone else’s bike. Custom motorcycle insurance rates that reflect your ride start with honest conversations about what you’ve modified, how you ride, and where you store your motorcycle. When you work with agents who understand your specific situation, you gain access to coverage that protects your custom parts, performance upgrades, and riding habits instead of leaving dangerous gaps.

Standard policies fail because they ignore the reality of your custom modifications and unique riding style. Your agent needs to know about every upgrade, every safety enhancement, and every change you’ve made to your bike so they can build coverage around your actual needs. This isn’t about paying more for unnecessary protection-it’s about paying for the right protection that actually covers what matters to you (and your investment).

Start by getting a quote that accounts for your actual situation and discussing your modifications, riding frequency, storage location, and riding style with your agent. Contact Leslie Kay’s, Inc. to get a quote built around your ride, not around someone else’s assumptions about what you need.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.