Motorcycle insurance premiums can drain your budget fast, but finding affordable motorcycle insurance online doesn’t have to be complicated. We at Leslie Kay’s, Inc. know that riders want protection without overpaying.

This guide shows you exactly how to compare quotes, understand what drives your rates, and cut costs through smart strategies like bundling and safety courses.

How to Find Affordable Motorcycle Insurance Online

Compare Quotes from Multiple Carriers Quickly

You need multiple quotes online if you want affordable motorcycle insurance, and speed matters. Most riders can grab three to five solid quotes in under 15 minutes by having your motorcycle’s year, make, and model ready before you start. A VIN speeds things up further, though you can absolutely get an accurate quote without it. The gap between the cheapest and most expensive quote for the same bike can easily hit 40 to 60 percent, which means skipping this step costs real money.

Start with carriers that rank well for online experience-Keynova Group ranked Progressive as the top online insurer in its Q4 2025 Online Insurance Scorecard, which tells you the platform handles quotes smoothly. As you compare quotes from top providers, pay attention to what coverage each quote includes because liability, comprehensive, and collision all land differently on your final price. Coverage requirements vary by state, so selecting your state during the quote process shows you exactly what’s mandatory versus optional in your area.

Understand Liability, Collision, and Comprehensive Coverage

Liability coverage is required in nearly every state and protects others and their property if you’re at fault in an accident, which is why lenders demand it if you financed your bike. Collision coverage handles damage from accidents, while comprehensive protects against theft, vandalism, fire, and weather-and these two matter most when it comes to price swings. Online quote tools let you toggle coverage amounts and deductibles to see the immediate impact on your premium, which gives you real control over the final number. Raising your deductible from 250 to 500 dollars typically cuts your collision and comprehensive costs by 15 to 25 percent, depending on your bike and location.

Customize Coverage to Match Your Riding Profile

Many riders miss the customization options hiding in online quote flows-things like guest passenger liability, helmet and gear replacement coverage up to 3,000 dollars, and custom parts protection. You should adjust coverage levels to match your actual risk and riding habits, then watch how your premium shifts. These choices directly affect what you pay each month, so take time to explore what each option costs. Your deductible, coverage limits, and add-ons work together to shape your final price, and online platforms make it easy to test different combinations before you commit.

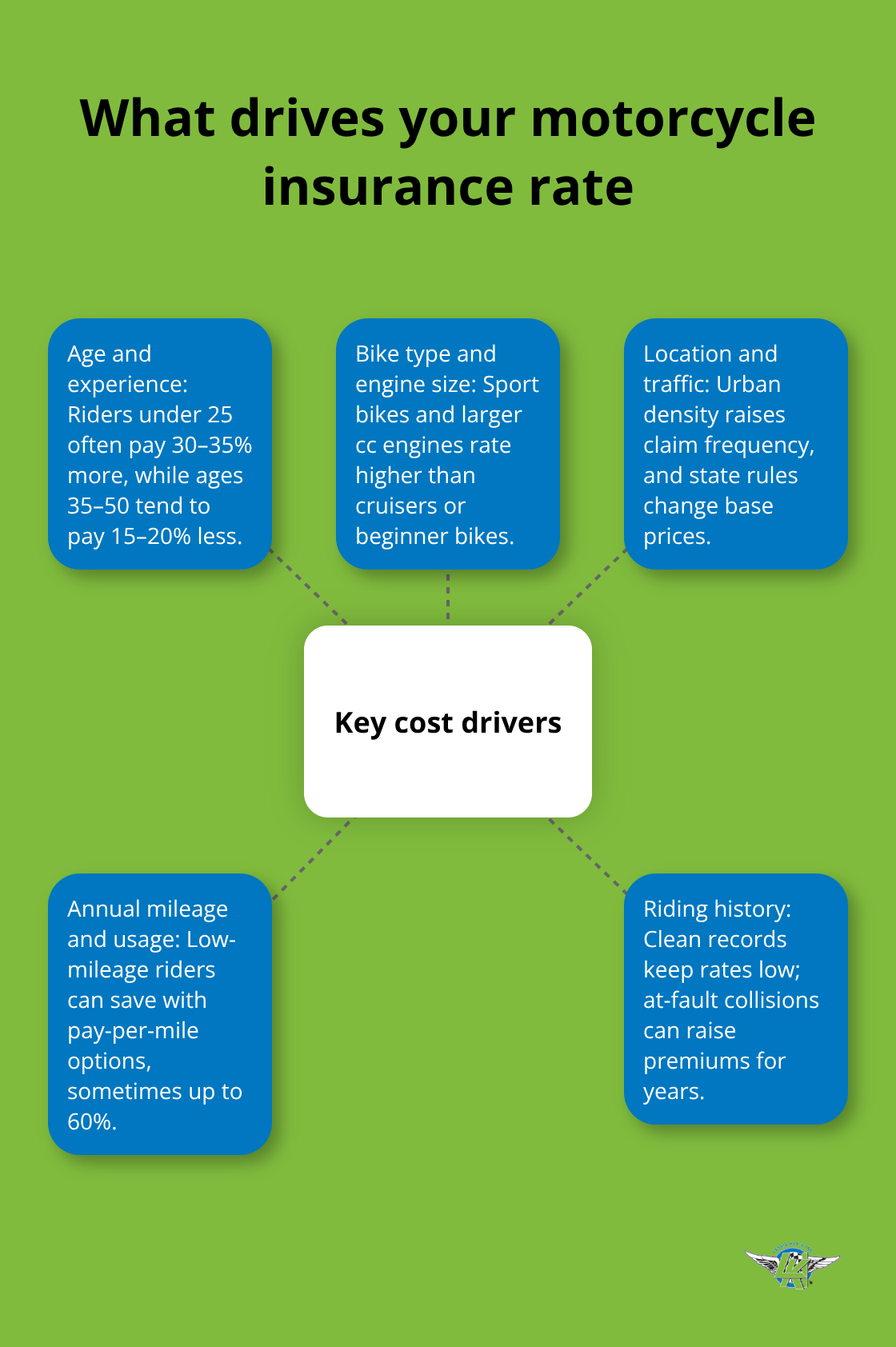

What Really Drives Your Motorcycle Insurance Costs

Age and Riding Experience Shape Your Premium

Your age and riding experience matter far more than most riders realize when it comes to what you’ll pay each month. Riders under 25 face 30 to 35 percent higher premiums than older riders, because younger riders file claims more frequently and with greater severity. The flip side works in your favor-riders aged 35 to 50 pay 15 to 20 percent less than those under 25, which reflects a lower risk profile that insurers reward with better rates. A clean riding history without accidents or violations is one of the fastest ways to lock in affordable rates, while even a single at-fault collision can push your premium up significantly for three to five years.

Motorcycle Type and Engine Size

Your motorcycle choice directly impacts your quote, and sport bikes consistently cost more to insure than cruisers or touring bikes because they attract higher claim rates. Engine size plays into this too-a 600cc sport bike will cost considerably more than a 250cc beginner bike, even from the same manufacturer. The bike you ride signals risk level to insurers, so your selection at purchase time affects what you’ll pay for years to come.

Location and Traffic Exposure

Your location determines a huge chunk of your final premium because urban riders in dense traffic face collision claims roughly 42 percent more frequently than rural riders, according to Statista data on motorcycle insurance claims. State regulations vary significantly, which is why two identical riders in different states can see premium differences of 40 percent or more. Weather exposure in your area also matters; riders in regions with heavy snow, hail, or frequent storms pay more for comprehensive coverage since weather claims are common.

Annual Mileage and Usage Patterns

Annual mileage affects your rate as well, and riders who log fewer than 2,500 miles per year can qualify for low-mileage discounts that save real money. If you ride seasonally or keep your bike in the garage most months, you should explore usage-based insurance options like pay-per-mile policies, which can save low-mileage riders up to 60 percent compared to standard annual premiums-some riders pay as little as $50 per year with this approach. Low-mileage riders who understand their actual usage patterns unlock substantial savings that standard policies simply cannot match.

How to Cut Motorcycle Insurance Costs Without Sacrificing Coverage

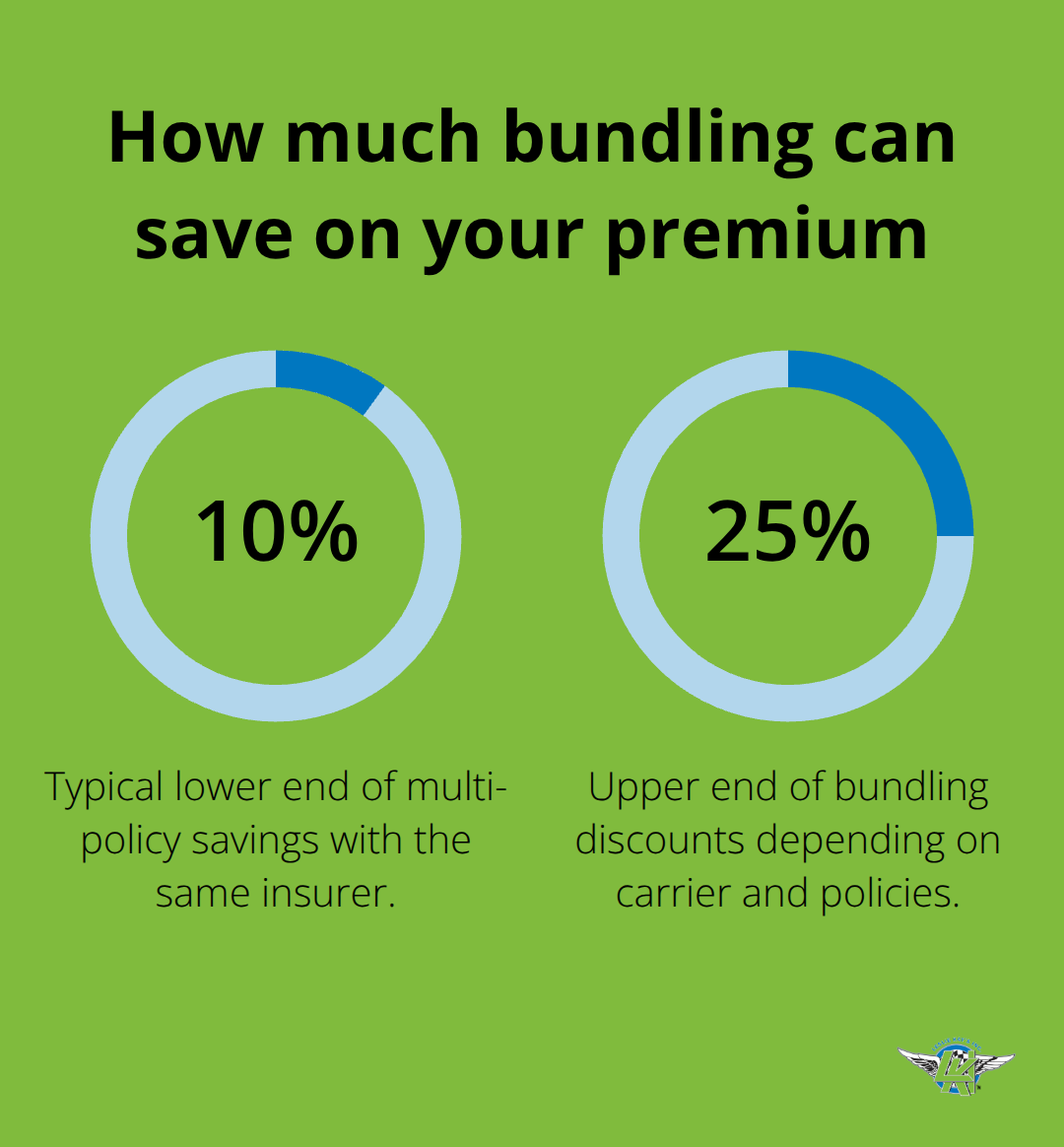

Stack Discounts Through Policy Bundling

Bundling your motorcycle policy with auto, home, or renters insurance delivers real savings that most riders overlook. Multi-policy discounts typically range from 10 to 25 percent depending on the carrier and what you combine together, which means a rider paying $80 monthly for motorcycle-only coverage could drop to $60 or $65 when adding a car policy to the same insurer. The math works because insurers reward loyalty and reduce their acquisition costs when you consolidate accounts. Start with each carrier during your quote process and ask what bundling discounts apply in your state, since availability varies-some states offer more aggressive multi-policy savings than others. If you currently carry auto insurance with one company and motorcycle coverage elsewhere, a single phone call to your auto insurer often reveals bundling options you never knew existed.

This single move frequently saves more than taking a safety course or raising your deductible, making it the first lever you should pull when shopping for affordable coverage.

Complete a Motorcycle Safety Course for Premium Reductions

Motorcycle safety courses cut premiums in concrete ways that insurers value because trained riders file fewer claims. Most courses last four to eight hours, cost between $150 and $300, and unlock discounts of 5 to 15 percent on your liability and collision coverage for three years. The Motorcycle Safety Foundation and state-approved programs qualify for discounts at nearly every major carrier, and some insurers waive the course cost entirely if you complete one before purchasing a policy. One rider taking the MSF Basic RiderCourse might spend $200 on training but recover that investment within four months through premium reductions on a standard annual policy.

Raise Your Deductible to Lower Annual Premiums

Raising your deductible attacks costs from the opposite angle-jumping from $250 to $500 typically reduces your collision and comprehensive premiums by 15 to 25 percent annually, while moving to $1,000 can save another 10 to 15 percent. The catch is real: you pay more out of pocket if you file a claim, so this strategy only works if you ride carefully and have emergency funds available. Low-mileage riders and those with clean riding histories benefit most from higher deductibles because their claim probability stays low, making the risk manageable.

Final Thoughts

Affordable motorcycle insurance online rewards riders who invest 15 minutes in comparing quotes across multiple carriers, since the gap between the cheapest and most expensive option typically hits 40 to 60 percent for identical coverage. Online platforms let you toggle liability, collision, and comprehensive amounts in real time, then watch your premium shift before you commit to anything. This transparency beats phone calls and in-person meetings because you control the process and make decisions based on actual numbers, not sales pressure.

Bundling your motorcycle policy with auto or home insurance often delivers bigger savings than any single discount, while a safety course pays for itself within months through premium reductions. If you ride fewer than 2,500 miles annually, pay-per-mile options can slash your costs dramatically compared to standard annual policies. Your motorcycle type, age, location, and riding history all shape what you’ll pay, but smart choices around deductibles and coverage customization put control back in your hands.

Visit Leslie Kay’s, Inc. to explore your options with an agency built by riders, for riders, and let our team handle the comparison work so you can focus on the road ahead.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.