Motorcycle riders face insurance challenges that car owners never encounter. At Leslie Kay’s, Inc., we know that finding the right biker motorcycle insurance quotes requires understanding coverage options built specifically for your riding needs.

This guide walks you through comparing policies side-by-side, evaluating what coverage actually protects you, and identifying discounts that reward safe riding habits.

Why Motorcycle Insurance Costs More Than Car Coverage

Motorcycle insurance runs significantly higher than auto insurance for concrete reasons rooted in risk assessment and specialized protection needs. Insurers classify motorcycles as higher-risk vehicles because accident statistics show motorcycle riders face substantially greater injury and fatality rates than car occupants. Motorcyclists are approximately 28 times more likely to die in a crash than passenger vehicle occupants, and five times more likely to suffer injury. This elevated risk directly translates into higher premiums regardless of your driving record. Additionally, motorcycles lack the protective shell and safety systems that cars provide, meaning even lower-speed impacts can cause severe injuries. Insurers factor in these realities when calculating your quote, which explains why a motorcycle policy costs roughly double what you’d pay for basic auto coverage on a comparable value vehicle.

How Bike Type Reshapes Your Premium

The motorcycle you ride determines a substantial portion of your insurance cost. Sport bikes and high-performance models command the highest premiums because insurers associate them with faster speeds, greater accident risk, and higher theft rates. A sport bike can cost 40 to 60 percent more to insure than a standard cruiser or commuter bike with the same rider. Touring bikes, cruisers, and standard motorcycles fall into lower-risk categories and attract more affordable rates. Engine size matters equally, with larger displacement bikes costing more than smaller ones due to increased power and accident severity. If you shop for a new motorcycle and cost concerns you, select a standard or cruiser model under 500cc to substantially lower your insurance expenses compared to a 1000cc sport bike. The specific make and model also influence pricing because insurers track theft rates and repair costs for each model, rewarding you for choosing bikes with lower theft exposure and reasonable parts availability.

Coverage Specifics Unique to Riders

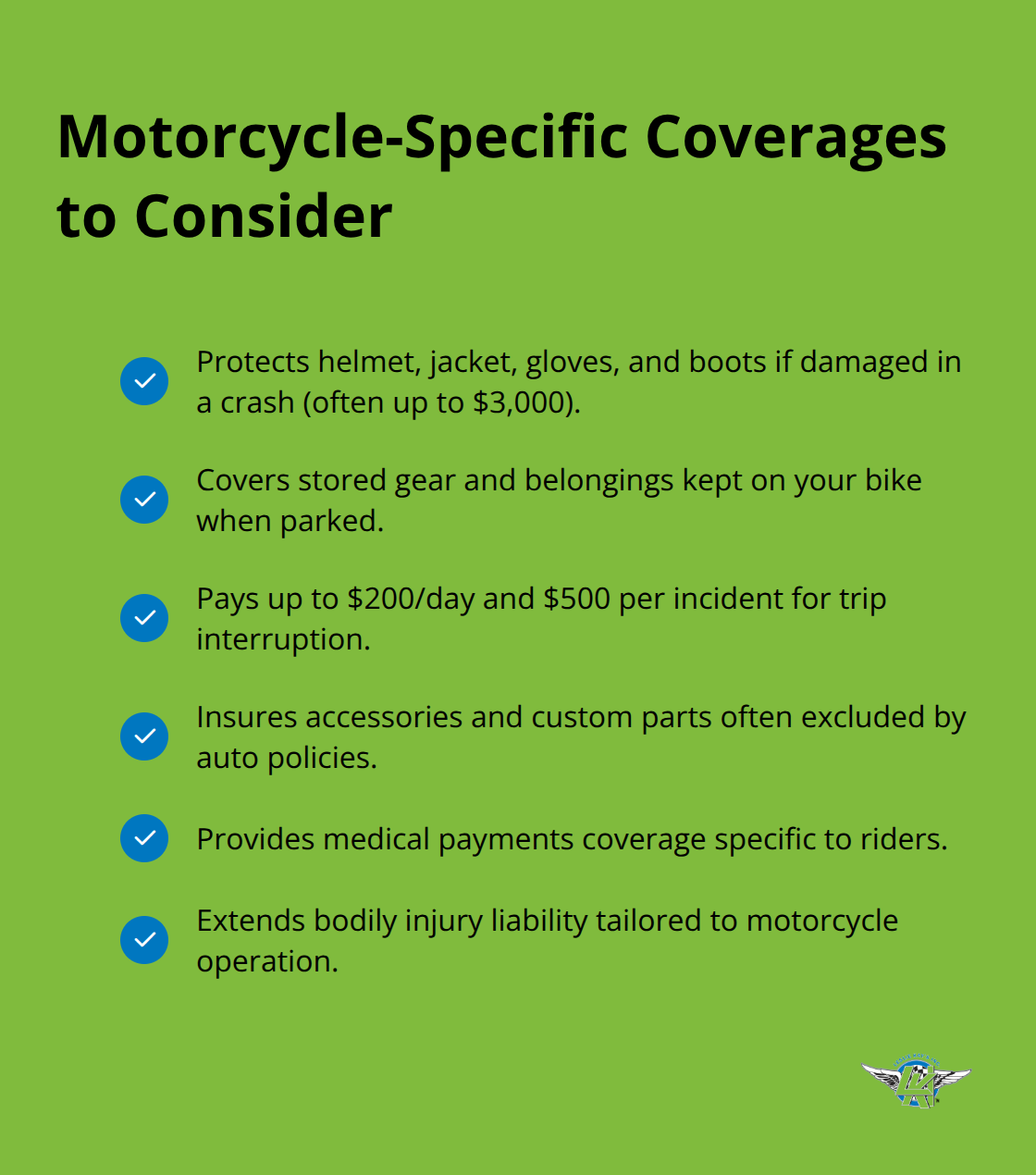

Motorcycle policies include coverage options that auto insurance never touches. Safety riding apparel coverage protects your helmet, jacket, gloves, and boots if a crash damages them, with some carriers covering up to $3,000 in gear. Stored gear coverage reimburses you for equipment kept on your bike when it sits parked, addressing the reality that riders carry belongings other vehicle operators don’t. Trip interruption coverage provides up to $200 daily and $500 per incident when a breakdown strands you away from home, recognizing that motorcyclists often take longer rides requiring specialized road service. Accessory and custom parts coverage protects aftermarket modifications, which riders frequently install but standard auto policies completely ignore.

Medical payments coverage and bodily injury liability both apply to you as the rider, whereas auto policies treat the driver differently from passengers. These specialized options exist because motorcycle riding creates exposures that four-wheel vehicles simply don’t have, and carriers have developed coverages that address the actual needs of the riding community rather than forcing riders into generic auto insurance templates.

What Separates Motorcycle Riders from Other Vehicle Owners

The differences between motorcycle and auto insurance extend beyond premiums and coverage types. Riders operate vehicles that demand active physical engagement and balance, exposing them to weather, road hazards, and visibility challenges that enclosed vehicles eliminate. Insurance companies recognize that a motorcycle accident often results in direct physical trauma to the operator, whereas car accidents distribute impact forces across a protective structure. This fundamental distinction shapes how insurers price policies and what coverages they offer. Understanding these differences helps you evaluate quotes more effectively and select policies that actually match your riding reality rather than settling for inadequate protection. As you compare quotes from different carriers, these risk factors and specialized coverages will appear consistently across policies, though each insurer weights them differently based on their claims data and underwriting philosophy.

Comparing Quotes Side-by-Side Without Missing Critical Details

Why Multiple Quotes Matter More Than You Think

Pulling quotes from multiple carriers reveals why shopping around matters so much. The US average for full-coverage motorcycle insurance sits around $364 annually, but individual quotes swing wildly based on how each insurer weights your specific risk factors. A 2018 Honda Rebel 500 ABS might cost $89 monthly with one carrier and $156 monthly with another, according to MoneyGeek’s pricing analysis. This 75-dollar monthly gap represents nearly $900 yearly on identical coverage, which explains why you should obtain at least three quotes from different insurers as your baseline standard. When you request quotes, compare the exact same coverage limits, deductibles, and add-ons across all carriers. Many riders make the mistake of comparing minimum liability policies against full-coverage quotes, which makes prices appear more different than they actually are.

Major Carriers and Their Coverage Strengths

State Farm covers all 50 states and offers motorcycle coverage for factory-built bikes, cruisers, touring models, and more with roadside assistance included when you purchase full coverage. Progressive operates nationwide except Massachusetts and provides optional accessory protection up to $3,000, expandable to $30,000 for customized builds. GEICO serves all 50 states with a 10 percent senior rider discount for those 50 and older, plus safety-course and bundling discounts that can substantially reduce your total premium.

Deductible Strategy and Pay-Per-Mile Options

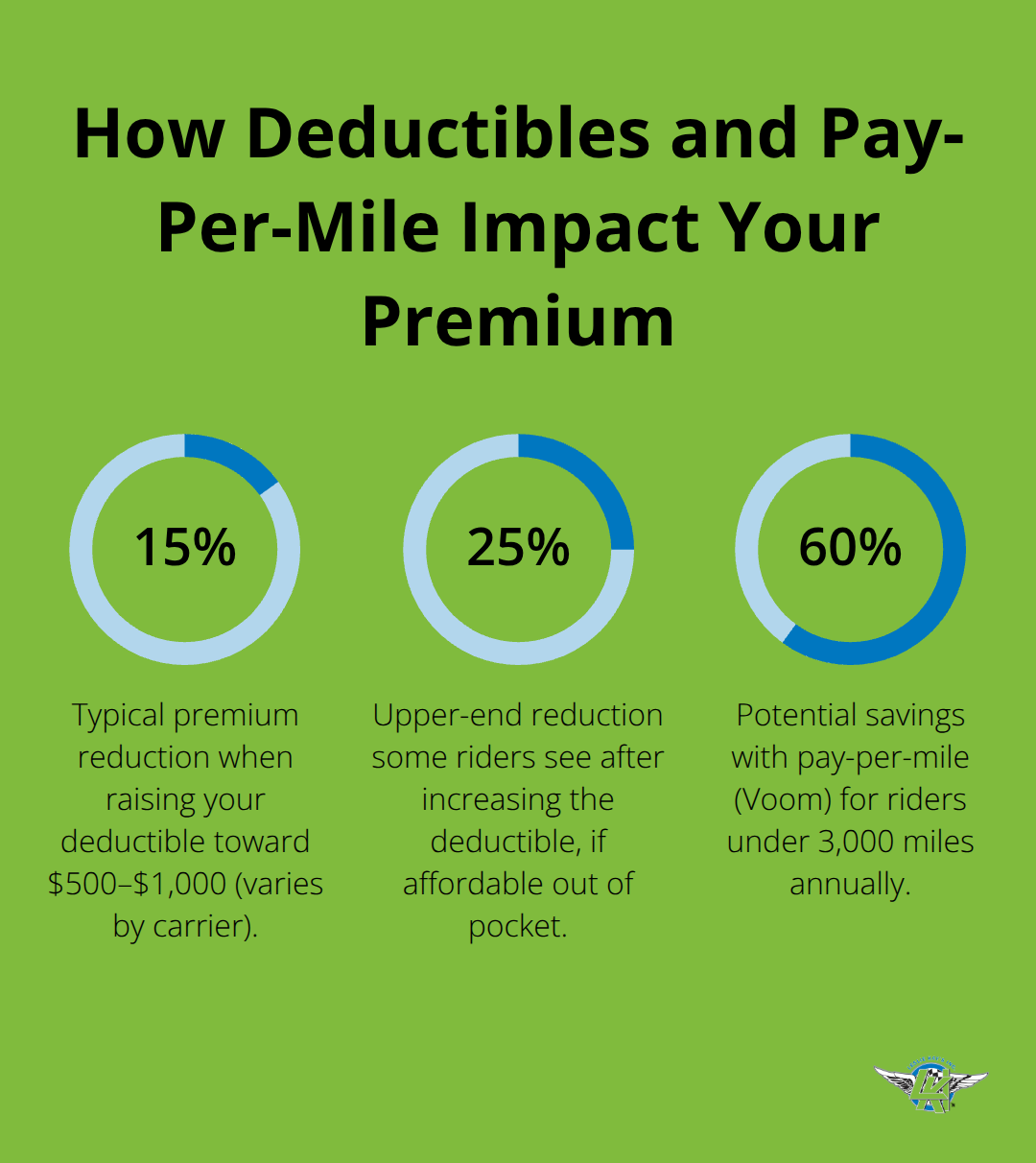

Your deductible choice creates the most immediate impact on monthly cost. Raising your deductible from $250 to $500 or $1,000 typically lowers premiums by 15 to 25 percent, but this strategy only works if you can actually afford that out-of-pocket amount if you file a claim. A sport bike rider paying $200 monthly might drop to $150 by increasing the deductible, yet a single accident could cost $1,000 out of pocket. Riders with low annual mileage should seriously consider pay-per-mile insurance through carriers like Voom, which starts around $50 yearly. Voom tracks mileage via monthly odometer photos with no hardware or app required, potentially cutting costs by up to 60 percent for riders covering under 3,000 miles annually.

Discounts That Reward Safe Riders

Discounts reward safe behavior and smart choices across all major carriers. Completing an MSF approved motorcycle safety course qualifies you for discounts with virtually every insurer, and some offer substantial rewards-GEICO provides up to 20 percent off for MSF instructors specifically. Multi-policy bundling consistently delivers 10 to 20 percent savings when you combine motorcycle, auto, home, or renters coverage with the same company. Maintaining a clean driving record matters enormously because a single speeding ticket or accident claim can raise your premium 25 to 40 percent, while riders with no violations enjoy the lowest available rates. Location and storage method also drive discounts-motorcycles stored in locked garages cost less to insure than those parked on streets, and anti-theft devices or tracking systems earn additional reductions from most carriers.

Moving Forward With Your Quote Comparison

Once you’ve gathered quotes and identified the discounts you qualify for, the next step involves evaluating which coverage options actually protect your specific riding situation and bike setup.

Essential Coverage You Cannot Skip

Why Liability Coverage Forms Your Foundation

Liability coverage protects you financially when you cause an accident that injures another person or damages their property. Most states require minimum liability limits, which vary by state for bodily injury and property damage coverage. Here’s the critical reality: these minimums are dangerously low. A serious accident involving another vehicle, passengers, or property can easily exceed $100,000 in damages, leaving you personally responsible for the difference if your policy limits are too low. You should carry at least $100,000 per person and $300,000 per accident in bodily injury liability, with $100,000 property damage coverage as a practical baseline that protects your assets without excessive premium increases. The cost difference between minimum and these higher limits typically runs $10 to $20 monthly, making the upgrade financially sensible.

Collision and Comprehensive: Protecting Your Bike

Collision and comprehensive coverage protects your own motorcycle rather than covering others, which is why lenders require both if you finance your bike. Collision covers accidents and impacts-dropping your bike, hitting a pothole, or colliding with another vehicle-while comprehensive handles theft, vandalism, weather damage, and animal strikes. Your deductible choice here dramatically affects your monthly cost; a $250 deductible costs substantially more than a $1,000 deductible, yet that $750 difference means you’d pay $1,000 out of pocket if your bike gets stolen. Riders financing newer sport bikes typically select $250 or $500 deductibles to minimize personal financial risk, while those with older bikes or strong emergency savings often jump to $1,000 to cut premiums.

Uninsured Motorist Coverage: Your Safety Net

Uninsured and underinsured motorist coverage protects you when another rider causes an accident but carries insufficient or no insurance-a remarkably common scenario since many riders operate without valid coverage. This coverage pays your medical bills and repair costs up to your policy limits when an uninsured motorist hits you, functioning as your safety net in situations where the at-fault party cannot cover damages. This protection is statistically vital rather than merely theoretical.

Final Thoughts

Comparing biker motorcycle insurance quotes from at least three major carriers like State Farm, Progressive, and GEICO ensures you find the best coverage at the lowest price for your specific situation. Request identical coverage limits, deductible amounts, and add-ons across all quotes so you can accurately compare what each insurer charges. Your liability foundation should exceed state minimums substantially, collision and comprehensive coverage should match your bike’s value and financing requirements, and uninsured motorist protection should reflect the reality that many riders operate without adequate insurance.

The coverage essentials discussed throughout this guide form your actual protection against financial disaster. Liability shields your personal assets when you cause an accident, collision and comprehensive protect your motorcycle investment, uninsured motorist coverage handles situations where other riders fail to carry insurance, and safety apparel plus stored gear coverage address the unique exposures that motorcycle ownership creates. These protections aren’t optional add-ons for riders who want comprehensive coverage-they form the foundation of responsible ownership.

Insurers weight your risk factors differently based on their claims experience, which means a quote that seems expensive from one carrier might be the cheapest option from another. Discounts for safety courses, bundling, clean driving records, and secure storage compound these differences, making shopping around financially essential. Contact Leslie Kay’s, Inc. to get your biker motorcycle insurance quotes and secure the right policy for your riding style.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.