RV owners face unique insurance challenges that standard auto policies simply don’t address. Your motorhome or travel trailer requires specialized protection that goes beyond what a typical car owner needs.

At Leslie Kay’s, Inc., we’ve helped countless RV enthusiasts understand why full coverage RV insurance matters. This guide walks you through what’s included, how it differs from regular auto insurance, and how to pick the right policy for your adventures.

What Your Full Coverage RV Policy Actually Protects

Collision and Comprehensive Coverage: Your Foundation

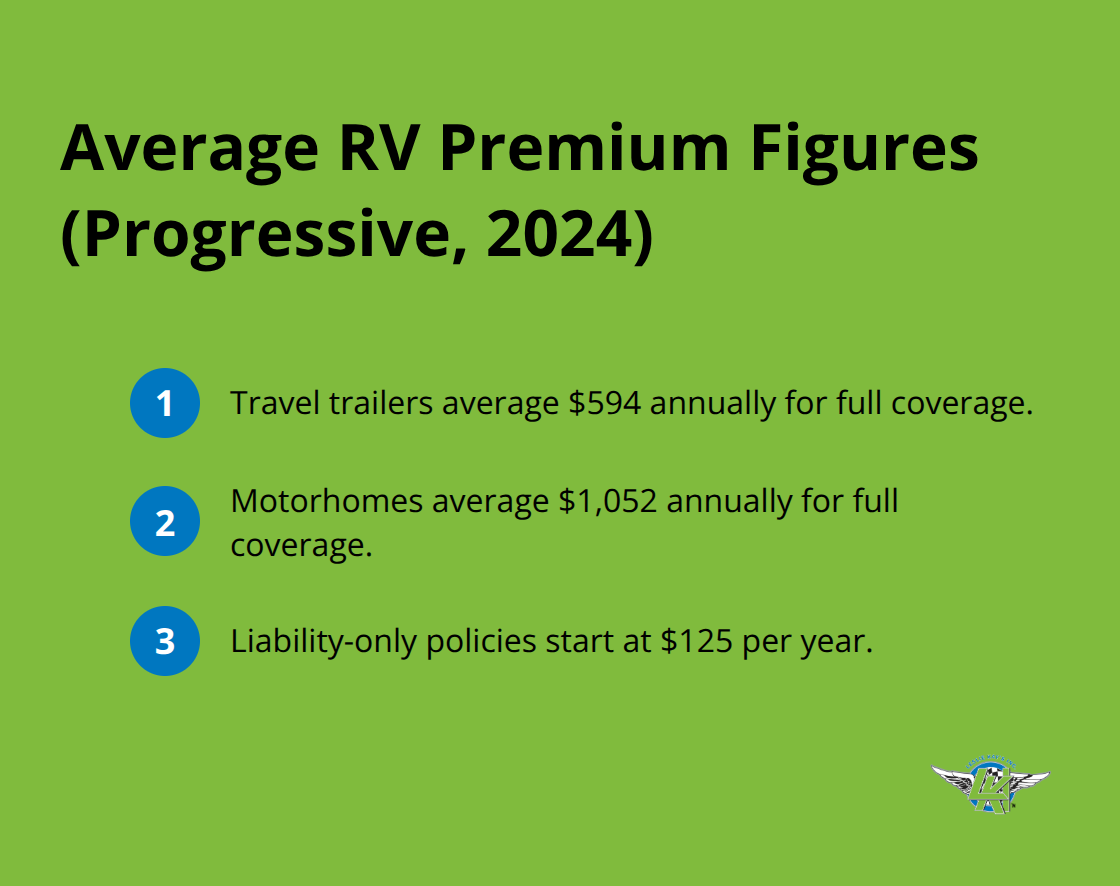

Collision coverage pays to repair or replace your RV after it hits another vehicle, a fence, a tree, or a guardrail-including hit-and-run incidents. Comprehensive coverage handles events outside your control: theft, vandalism, fire, hail, high winds, lightning, and weather damage. Glass breakage that doesn’t involve a collision also falls under comprehensive. Both require you to select a deductible, typically ranging from $500 to $1,000, and selecting a higher deductible lowers your premium. Progressive’s 2024 data show that average RV premiums run $594 per year for travel trailers and $1,052 per year for motorhomes when you include liability-only coverage starting at $125 per year.

If you finance your RV, lenders almost always require both collision and comprehensive. If you own your RV outright, the decision depends on your finances and risk tolerance. An older RV worth only a few thousand dollars may not justify physical-damage coverage with a $1,000 deductible, but high-value motorhomes or RVs you live in full-time need this protection against major loss.

Liability Coverage Protects Your Assets

Liability coverage is legally required in most states and covers damage or injuries you cause to other people or their property. For motorhomes, this is mandatory; for towable RVs, your tow vehicle’s liability typically covers you while on the road, but your trailer itself needs its own comprehensive and collision coverage. A single serious accident can easily exceed $100,000 in damages, especially if multiple vehicles or injuries are involved. Many RV owners set liability limits too low for their actual exposure.

You should review your liability limits before each trip, particularly if you’re towing or traveling with passengers. This simple step prevents underinsurance when it matters most.

Optional Protections That Fill Critical Gaps

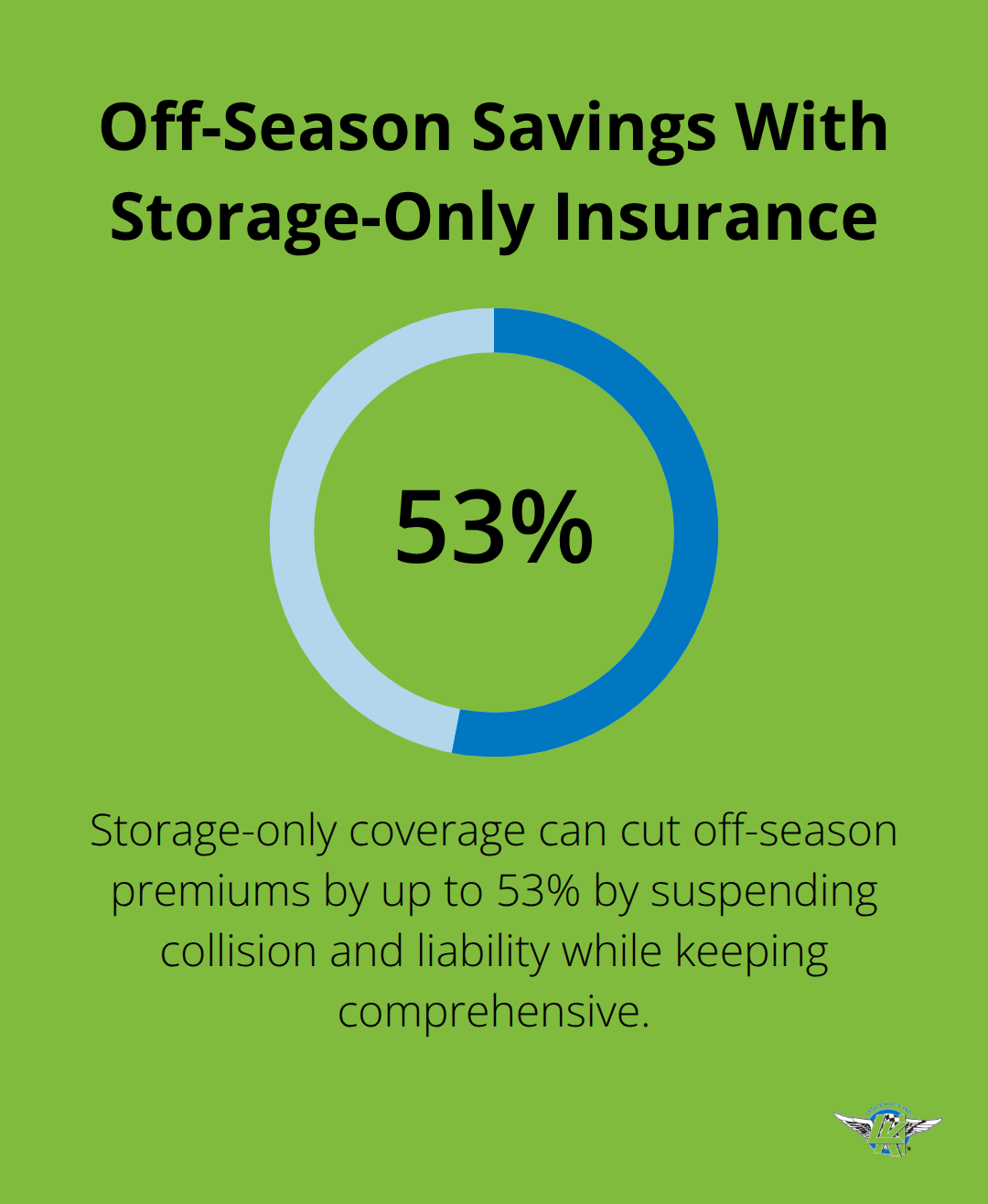

Additional protections worth considering include roadside assistance for breakdowns or lockouts, emergency expense coverage for hotel stays if your RV becomes uninhabitable, personal effects replacement for electronics and belongings inside your RV, and vacation liability for accidents that happen at your campsite. Storage-only insurance suspends collision and liability during off-season months while keeping comprehensive protection, potentially cutting premiums by up to 53% when your RV sits unused.

The key is matching your coverage to your actual usage patterns and asset value, not purchasing blanket protection you don’t need. Your coverage choices directly affect both your financial security and your monthly costs-which brings us to how RV insurance differs fundamentally from the standard auto policy most drivers carry.

Why Standard Auto Insurance Won’t Cover Your RV

The Coverage Gap Between Auto and RV Policies

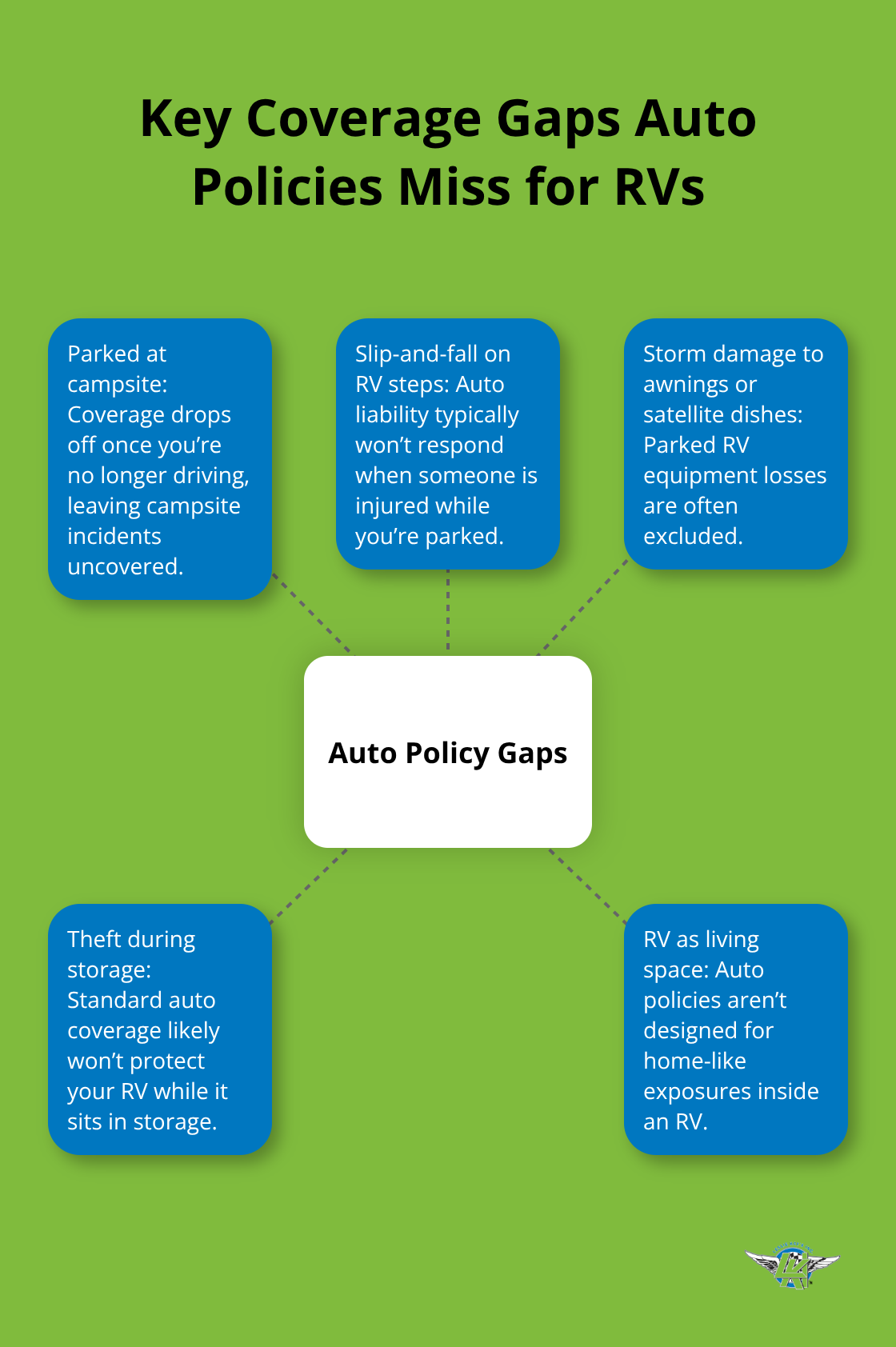

Standard auto insurance treats your vehicle as a car that sits in a garage most of the time. Your RV, by contrast, functions as a mobile home, business, and recreational vehicle simultaneously. An auto policy covers liability and collision while you’re driving, but it leaves massive gaps the moment you park at a campsite. If someone slips on your RV’s steps, your auto policy won’t respond. If a storm damages your awning or satellite dish while you’re parked for two weeks, you remain uninsured.

If thieves target your RV while it sits in storage, standard auto coverage likely won’t protect you. The National Highway Traffic Safety Administration reports RV accident trends over the past decade, yet most RV owners discover their auto insurer won’t acknowledge an RV claim until it’s too late.

Why RV Value Demands Specialized Protection

The value difference alone makes RV-specific policies non-negotiable. A typical motorhome costs $75,000 to $150,000 or more, and Class A models frequently exceed $200,000. Travel trailers range from $14,000 to $50,000 depending on size and features. Your auto policy caps coverage far below these values and completely ignores permanent attachments like awnings, antennas, and satellite dishes (which can cost $3,000 to $8,000 to replace). Storage location matters significantly too. If your RV sits in a high-theft region or an unprotected lot during winter, comprehensive coverage becomes essential because your auto policy won’t cover theft or vandalism at all.

Full-Time Living Requires Home-Style Protection

Full-time RVers who live in their vehicles need homeowners-style liability protection and personal property coverage for belongings inside-protection that no auto policy provides. Seasonal travelers benefit from storage-only insurance that suspends collision and liability during off-season months while keeping comprehensive protection, potentially cutting premiums by up to 53% when your RV sits unused. These specialized needs exist because RVs operate across multiple states with varying legal requirements, and they function as living spaces rather than transportation-only vehicles.

How RV Insurance Addresses What Auto Policies Miss

RV insurance addresses these gaps by blending auto, home, and travel coverage into a single policy designed for vehicles that double as living spaces. This hybrid approach protects you at campsites, during storage, and across state lines in ways that standard auto or home policies simply cannot match. The moment you understand what your RV actually needs-and what your current auto policy fails to provide-the case for specialized RV coverage becomes clear. Selecting the right RV insurance policy requires you to assess your specific situation, compare what different carriers offer, and match your coverage to your actual usage patterns.

Selecting Your RV Insurance to Match Your Actual Situation

Know Your RV’s True Market Value

Start with your RV’s current market value, not what you paid for it. Check NADA Guides or Kelley Blue Book for your specific model and year, then compare that figure against your deductible options. If your RV is worth $15,000 and you select a $1,000 deductible, you protect a meaningful asset. If your RV is worth $8,000 and you consider a $1,500 deductible, liability-only coverage might actually serve you better financially.

Match Coverage to Your Usage Patterns

Progressive’s 2024 data shows travel trailers average $594 annually for full coverage, but liability-only policies start at $125 per year-a substantial difference when your RV depreciates faster than you pay premiums. An RV that sits in storage nine months yearly doesn’t need the same collision protection as one you live in full-time or use every weekend. Storage-only insurance cuts premiums by up to 53% during off-season by suspending collision and liability while keeping comprehensive protection for theft and weather damage.

If you travel primarily within one or two states, rates stay lower than if you cross multiple regions where theft and accident rates vary dramatically. Document your annual mileage honestly-underreporting to save premium dollars creates a claim denial trap if an accident occurs.

Obtain Quotes From Multiple Carriers

Obtain apples-to-apples quotes from at least three carriers before deciding, and provide identical RV details and coverage limits to each one. Most insurers now offer online quotes in minutes, but speaking with a licensed representative ensures you avoid missing state-specific requirements or endorsements that matter for your situation. The Good Sam Insurance Agency specializes in RV coverage and shops multiple carriers to balance protection and price rather than pushing you toward a single preferred option. Leslie Kay’s, Inc., an independent agency built for adventure enthusiasts, also shops multiple carriers to deliver customized, competitively priced policies tailored to your specific needs.

Compare What Each Policy Actually Covers

When comparing quotes, examine what each policy actually covers-one carrier might include full replacement cost for total loss while another doesn’t, and that $2,000 to $5,000 difference should factor into your decision. Higher deductibles reduce premiums significantly; jumping from $500 to $1,000 typically cuts your annual cost by 15 to 25 percent depending on your RV’s value and claims history. Bundling RV insurance with auto or home policies often yields 15 to 20 percent overall savings across all policies combined, which frequently outweighs the slight premium increase from carrying full coverage.

Leverage Discounts and Special Programs

Ask each carrier about discounts for paid-in-full policies, multi-vehicle coverage, good driving records with no accidents or violations in the past three years, safety features like GPS tracking or anti-theft devices, and affiliation memberships that might apply to you. Personal belongings coverage should match your actual inventory-measure the replacement cost of electronics, gear, and furniture inside your RV, then confirm your policy limits align with that total. These discounts stack quickly and can reduce your final premium far more than selecting a higher deductible alone.

Final Thoughts

Full coverage RV insurance protects your investment across multiple states and usage scenarios in ways that standard auto policies simply cannot match. Your RV’s value, storage location, and annual mileage directly determine which coverage options make financial sense for your situation. An RV worth $15,000 sitting in storage nine months yearly requires different protection than a $120,000 motorhome you live in full-time, and Progressive’s 2024 data show travel trailers average $594 annually for full coverage while liability-only policies start at $125 per year.

Shopping multiple carriers remains the single most effective way to secure competitive rates without sacrificing essential protection. Obtain apples-to-apples quotes from at least three insurers, provide identical RV details to each one, and examine what each policy actually covers before deciding. Higher deductibles reduce premiums significantly, but only if you can afford the out-of-pocket cost after a claim occurs, and bundling RV insurance with auto or home policies often yields 15 to 20 percent overall savings across all policies combined.

Contact Leslie Kay’s, Inc. today to compare quotes and secure the full coverage RV insurance protection your adventures deserve. We shop multiple carriers to deliver customized, competitively priced policies tailored to your specific RV needs and travel patterns. Your next road trip starts with the right coverage in place.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.