Your boat represents a significant financial investment that deserves real protection. Marine insurance for boats isn’t optional-it’s the difference between a manageable claim and financial disaster.

At Leslie Kay’s, Inc., we’ve helped countless boat owners navigate coverage options that actually match their needs. This guide walks you through the types of coverage available, what affects your rates, and the mistakes that cost boat owners thousands in inadequate protection.

What Coverage Types Actually Protect Your Boat

Hull coverage and physical damage protection form the backbone of any marine insurance policy, and this is where most boat owners get it wrong. Hull coverage pays for repairs or replacement of your boat after collisions, theft, vandalism, fire, or weather damage like hurricanes and lightning strikes. You’ll choose between two approaches: Agreed Value, which means you and the insurance company decide upfront what your boat is worth, or Actual Cash Value, which pays current market value minus depreciation. Agreed Value almost always makes more sense because it eliminates arguments about what your boat is worth when you need the money. The coverage extends beyond just the hull itself-it includes engines, fuel tanks, batteries, safety equipment, and onboard furnishings damaged in a covered incident. Physical damage deductibles typically start around 1% of your boat’s insured value and can go up to 5%, so a $50,000 boat might have a $500 to $2,500 deductible. Higher deductibles lower your premiums, but they increase what you pay out of pocket after a claim, so choose based on what you can actually afford to cover yourself.

Why Liability Coverage Isn’t Optional

Liability coverage protects you from financial catastrophe if you injure someone or damage another person’s property while boating. This coverage pays for medical bills, lost wages, and legal costs up to your policy limits, and it covers passengers in watersports as well. Most policies include wreckage removal and disposal as part of liability, which matters because removing a sunken boat costs thousands. Many boat owners dramatically underestimate their liability exposure-if you hit another boat worth $200,000 or injure someone seriously, your personal assets become vulnerable without adequate coverage. Liability limits should reflect the value of boats you might hit and the potential medical costs of injuries, not just the minimum your state requires.

Uninsured and Underinsured Coverage Fills a Critical Gap

Uninsured and underinsured boater coverage protects you when another boater lacks sufficient liability insurance or has no insurance at all. This coverage pays your medical costs and, in some cases, property damage to your boat when you’re hit by an uninsured or underinsured boater. In Florida, where boating is extremely popular with an extensive coastline and numerous waterways, this protection matters more than in landlocked states because you encounter more boats and more operators with varying insurance levels. The coverage applies regardless of who caused the accident, so you’re protected even if the other boater was at fault but couldn’t pay. Many policies set per-person medical limits and annual caps for this coverage, so verify these limits match your needs-if you boat with family or friends regularly, higher limits make sense.

What Happens Next With Your Rates

Your coverage choices matter, but they’re only half the equation. The next section examines what actually drives your boat insurance rates and why two boat owners with similar vessels can pay dramatically different premiums.

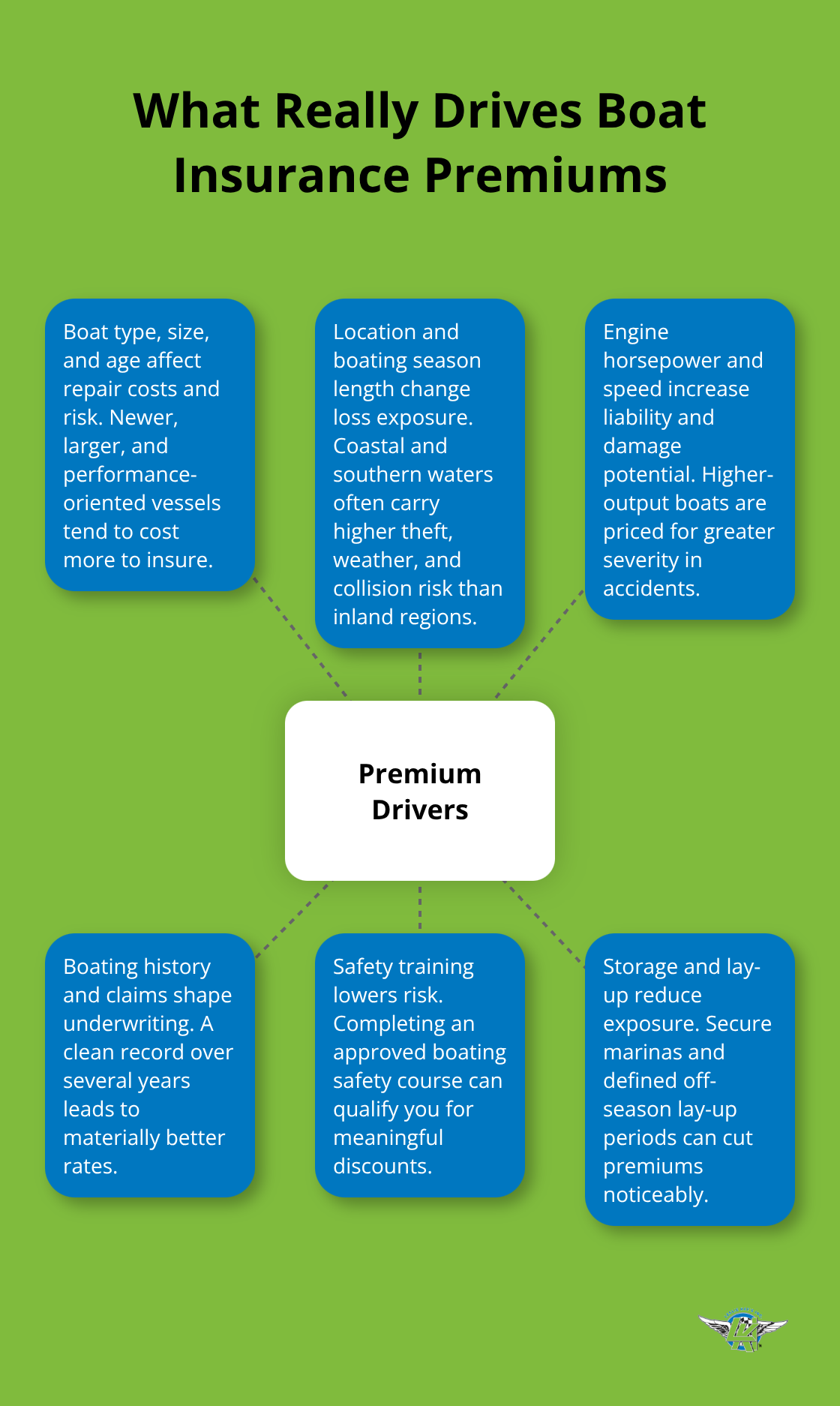

What Really Drives Your Boat Insurance Costs

Boat Type, Age, and Value Shape Your Premium

Your boat’s age, size, and type directly determine how much you’ll pay for insurance, and the numbers vary dramatically across the country. A 25-foot fishing boat in Minnesota costs around $267 annually on average, while the same boat in Florida runs $839 per year-that’s a 214% difference driven entirely by location and boating season length. Coastal southern states with longer boating seasons and bigger ocean-going vessels consistently pay more than northern inland and Great Lakes states where boats tend to be smaller and used seasonally.

Boat type matters significantly too: pontoon boats, fishing vessels, and powerboats all carry different risk profiles and repair costs that insurers price accordingly.

A boat valued at $50,000 will cost less to insure than a $150,000 vessel simply because the potential repair and replacement costs are lower. Engine horsepower affects your premium as well-more powerful boats represent higher liability exposure and faster accident speeds, so a 300-horsepower fishing boat costs more to insure than a 150-horsepower recreational cruiser. Your boat’s age plays a substantial role in underwriting decisions too. Older boats may require a recent marine survey before an insurer will even quote your policy, and that survey directly influences the terms you receive.

Your Boating History and Safety Training Cut Costs

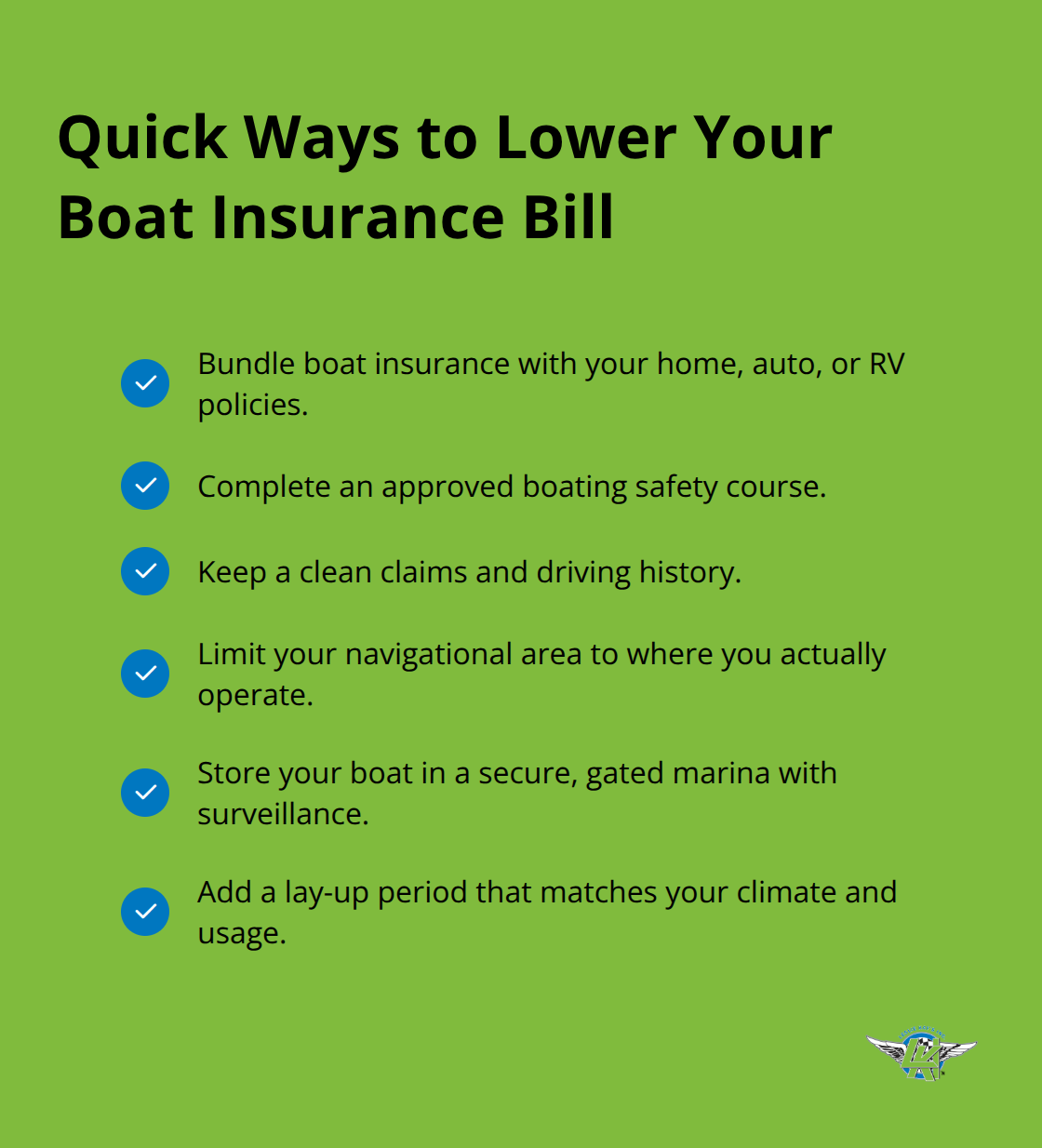

Your personal boating history and where you operate your boat matter more than most owners realize. Completing an approved boating safety course qualifies you for meaningful premium discounts because these courses reduce accident risk statistically. If you’ve filed claims in the past, insurers will charge higher premiums-a clean claims history over three to five years substantially improves your rates. Your driving record factors into boat insurance quotes too, since insurers view auto claims as indicators of overall risk management habits.

Location, Storage, and Lay-Up Periods Lower Your Rates

The waters where you operate your boat directly impact your premium because some regions have higher theft, accident, and weather damage rates than others. Operating your boat only within a limited navigational area rather than coastal coverage across multiple states lowers your premiums noticeably. If you store your boat in a secure marina with gated access and surveillance, you’ll pay less than someone who keeps their boat in an unsecured location or at home. Lay-up periods-the months when you don’t use your boat-can earn substantial discounts if you request the longest reasonable lay-up period for your climate and boating patterns.

The combination of safety training, clean history, and smart storage choices can reduce your annual premium by 20 to 30 percent compared to an owner with the same boat who ignores these factors. These adjustments aren’t minor tweaks-they represent real savings that add up year after year. Understanding what drives your rates puts you in control of your costs, but many boat owners still make preventable mistakes when selecting their coverage that undermine these savings.

Mistakes That Cost Boat Owners Thousands in Inadequate Coverage

Most boat owners make their coverage decisions in a rush, often just before launching season, and these rushed choices compound into serious financial gaps when accidents happen. The first major mistake is underestimating what your boat and liability exposure actually require. Many owners base their coverage limits on their boat’s purchase price, but that’s backwards-your liability coverage should reflect the value of vessels you might collide with and potential medical costs from serious injuries, not your own boat’s value.

Liability Coverage Gaps Leave You Exposed

If you operate a 25-foot center console in Florida waters where you encounter expensive offshore yachts and fishing charters, carrying the state minimum liability coverage is reckless. Florida boat insurance premiums averaged $839 annually in 2023-2024 for good reason-the waters are crowded and accident costs run high. A collision with a $300,000 sport yacht or a serious injury claim involving multiple passengers can easily exceed $100,000 in damages, yet many boat owners carry liability limits of just $25,000 or $50,000.

Your hull coverage faces similar underestimation. Owners often choose actual cash value instead of agreed value to save a few dollars on premiums, then discover at claim time that depreciation slashed their payout by 30 to 40 percent. That premium savings of maybe $100 annually becomes a $15,000 shortfall when your boat needs major repairs.

Seasonal Storage and Lay-Up Periods Offer Real Savings

The second costly mistake is ignoring lay-up periods and seasonal storage entirely. If you boat only from May through October but carry year-round coverage, you waste money on premiums for months when your boat sits unused. Requesting the longest reasonable lay-up period for your climate can reduce your annual premium by 10 to 15 percent-that’s $80 to $125 in savings on an $839 Florida policy.

Where you store your boat during off-season matters tremendously. Boats stored in secured marinas with gated access, surveillance, and professional management qualify for better rates than boats left in backyard storage or at unsecured docks. This single decision can shift your premium by several hundred dollars annually.

Multi-Policy Bundling Cuts Costs Significantly

The third mistake-failing to bundle your boat insurance with auto, home, or RV policies-leaves significant discounts on the table. Multi-policy bundling typically cuts 10 to 20 percent from your overall insurance costs across all your policies. If you carry homeowners, auto, and boat insurance separately, you likely pay $200 to $400 more annually than you should.

Shopping with an independent agency that works across multiple carriers helps you capture every available discount while maintaining the specific coverage your watercraft actually needs.

Final Thoughts

Your boat deserves protection that matches its real value and your actual liability exposure. The coverage decisions you make today determine whether a boating accident becomes a manageable claim or a financial catastrophe that threatens your personal assets. Marine insurance for boats protects your waterbound investment when you understand what you need, what drives your costs, and where you can cut expenses without cutting protection.

We at Leslie Kay’s, Inc. specialize in watercraft coverage across multiple carriers, which means we shop your policy to find the specific protection your boat needs at the most competitive price available. As an independent agency, we work with numerous insurers rather than pushing one company’s products, so your coverage reflects your actual boating patterns and risk profile, not a one-size-fits-all template. Our team handles claims support seven days a week, which matters when you need answers fast after an incident on the water.

Contact Leslie Kay’s, Inc. for a personalized quote that accounts for your boat type, where you operate, your boating history, and the coverage limits that protect your waterbound investment properly. We identify every discount you qualify for-bundling, safety training, storage location, lay-up periods-and build a policy that fits your budget without leaving gaps that cost you later.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.