Your boat deserves protection that matches its unique value and how you actually use it. A generic insurance policy won’t cut it-most boaters end up with gaps in coverage or paying for protections they don’t need.

At Leslie Kay’s, Inc., we build custom boat insurance policies that fit your specific boat and budget. We’ll walk you through exactly what coverage matters for your situation.

Why One-Size-Fits-All Boat Insurance Fails

Different Boats Face Different Risks

A pontoon boat used for weekend family outings faces completely different risks than a fishing vessel that runs offshore three days a week. Yet many standard policies treat them as interchangeable. Homeowners insurance, for instance, typically won’t cover your boat at all-and if it does, the limits are so low they’re nearly worthless. Most homeowners policies cap boat coverage at 10 to 15 horsepower, which means anyone with a real boat needs dedicated watercraft coverage.

Coverage Gaps That Cost You Money

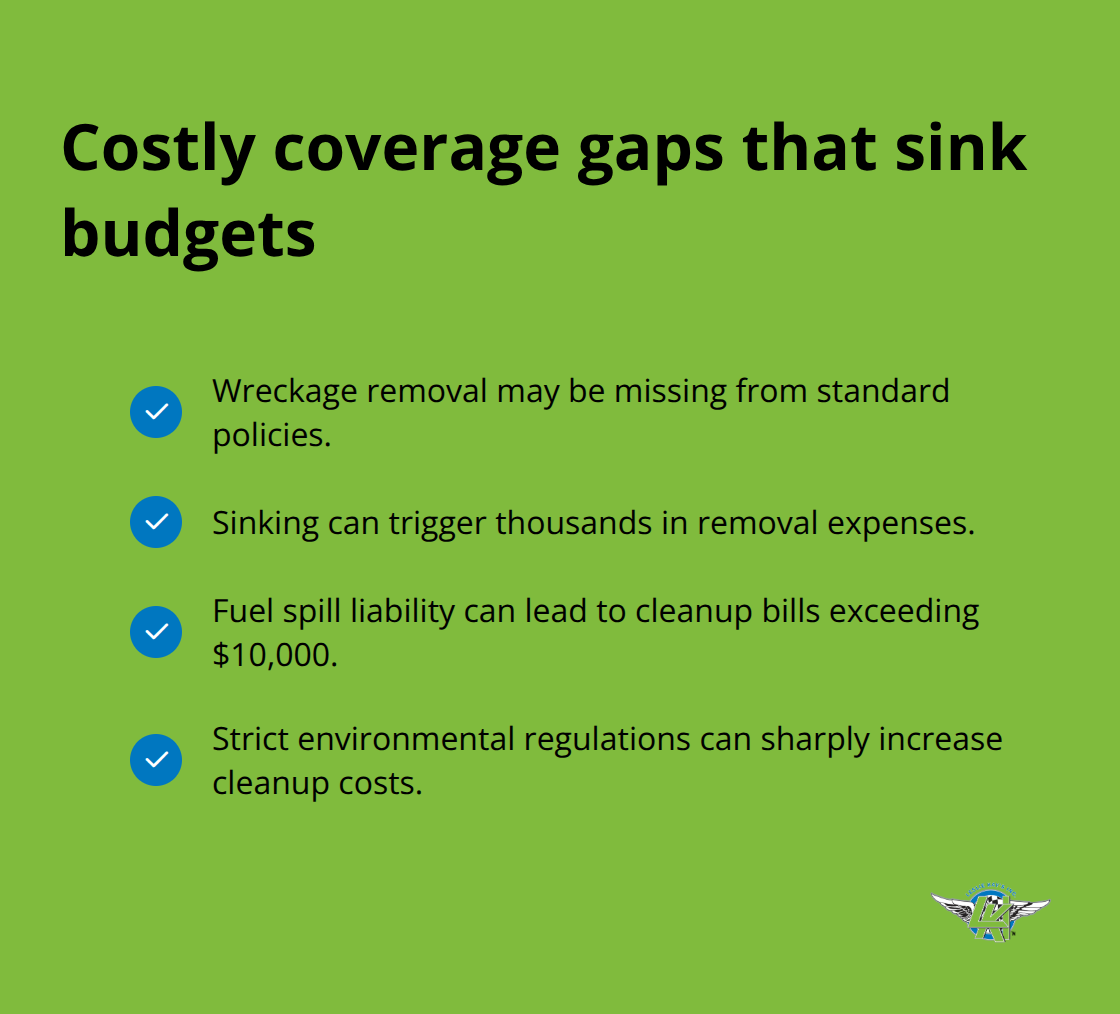

The problem worsens when you examine what standard boat policies actually protect. Many boaters discover after an incident that their policy didn’t include wreckage removal, which can cost thousands of dollars when your boat sinks. Fuel spill liability coverage represents another gap that catches people off guard, especially in states with strict environmental regulations where cleanup costs can exceed $10,000. These aren’t minor details-they’re the difference between a manageable loss and financial disaster.

Location and Experience Shape Your Real Risk

Your boating location matters enormously. Coastal navigation in Florida or Southern California exposes you to hurricane risk, theft, and saltwater corrosion-risks that inland boaters on lakes don’t face. A policy built for Midwest lake boating leaves you dangerously underprotected if you launch in Miami. Your experience level and how often you boat directly influence your premium and what coverage makes sense. Someone who boats 50 days a year with a spotless record deserves different pricing than a new boater with their first vessel. Standard policies don’t account for these distinctions effectively.

Choosing the Right Hull Value Coverage

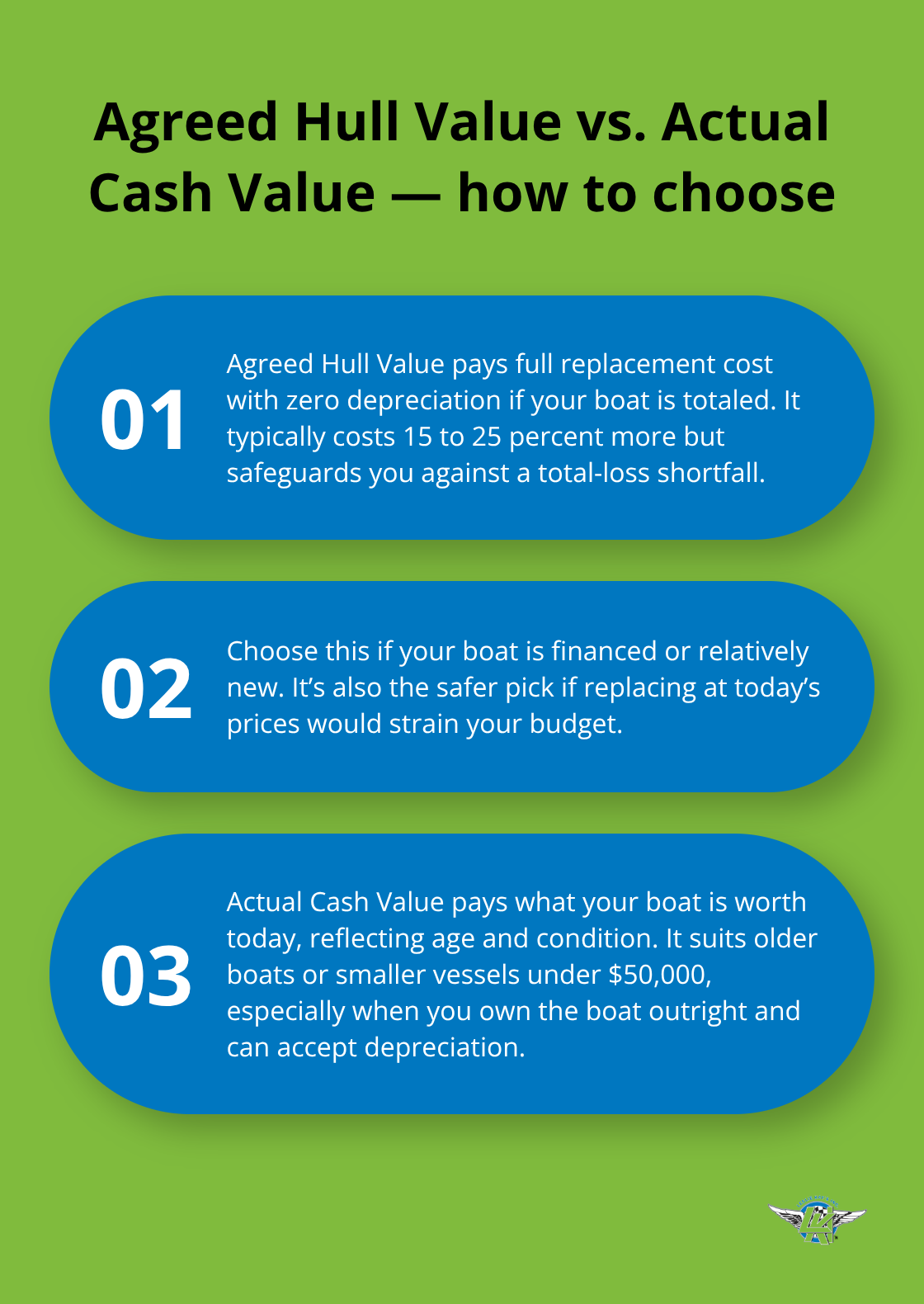

The solution starts with matching your coverage to your actual boat type, usage patterns, and location. If you finance your boat, your lender requires comprehensive and collision coverage plus liability-but lenders don’t care if you’re underinsured beyond those minimums. You need to decide whether Agreed Hull Value or Actual Cash Value makes sense for your situation. Agreed Hull Value pays full replacement cost for a total loss with no depreciation, which costs more but protects you if your boat is totaled. Actual Cash Value reduces your premium by paying current market value, which works better for older boats or smaller vessels.

Optional Coverages That Match Your Boating Style

Optional coverages like on-water towing, medical payments, and fishing equipment protection aren’t luxuries-they’re tactical choices based on where and how you boat. TowBoatUS towing coverage costs as little as $3 per month but becomes essential if you boat in remote areas far from shore. Medical payments coverage protects your passengers if someone gets injured on board, which matters if you frequently have family or friends aboard. Fishing equipment coverage reimburses you for rods, reels, and tackle if they’re damaged or lost, which adds up quickly for serious anglers. These options let you build a policy that reflects your actual boating life, not some theoretical average boater. The next step involves understanding exactly which factors drive your premium up or down-and how to control the ones you can.

Build Your Policy Around Real Boat Numbers

Gather Your Boat’s Exact Specifications

Start with the exact specifications of your boat, not generalizations. Write down your boat’s hull identification number, length, horsepower, engine type, and age. These details directly determine your premium and available coverages. A 25-foot pontoon with twin 150-horsepower outboards costs vastly different to insure than a 25-foot center console with a single 300-horsepower outboard. Insurance companies use these specifications to assess risk accurately, so vague descriptions lead to inaccurate quotes and potential coverage mismatches.

Document Your Actual Usage Patterns

Next, document how you actually use your boat. Do you launch it 12 times a year for family weekends, or 100 times a year for fishing tournaments? Does your boat stay in a marina slip, or do you trailer it to different launch sites? Does it stay in the water year-round, or do you winterize it? Insurance companies track these details because usage patterns directly correlate with claims frequency. A boat that sits in a heated marina slip in Minnesota faces different theft and weather risks than an identical boat stored outside in Florida. Your navigation area matters equally. If you fish coastal waters in Louisiana, your policy needs different protection than someone who stays within 10 miles of shore on a Great Lakes lake. Some carriers restrict coverage based on navigation limits, and hurricane-prone states like Florida often impose lower hull value limits-for example, 35 feet in length and $175,000 in value maximum in certain high-risk zones.

Choose Between Agreed Hull Value and Actual Cash Value

Agreed Hull Value coverage pays full replacement cost for a total loss with zero depreciation, which protects you if your boat is totaled but costs 15 to 25 percent more in premiums. This approach makes sense if your boat is financed, relatively new, or if you’d struggle to afford replacement at current market prices. Actual Cash Value reduces your premium by paying what your boat is worth today, accounting for age and condition.

This option works better for older boats, smaller vessels under $50,000, or situations where you own the boat outright and could accept depreciation on a total loss. The real decision hinges on one question: could you absorb the depreciation hit and still replace your boat? If the answer is no, Agreed Hull Value is mandatory.

Select Optional Coverages That Fit Your Boating Life

Add optional coverages strategically based on your actual boating life. Towing coverage runs as little as $3 per month for boats under 20 feet, or about $50 annually for larger vessels in most states, but costs $30 yearly in Florida due to higher risk. This becomes essential if you fish remote areas, boat far from shore, or frequently trailer to unfamiliar launch sites. Medical payments coverage typically costs $10 to $25 annually and covers emergency medical bills for you and your passengers regardless of fault. If you regularly have family or friends aboard, this protects against unexpected medical expenses from watersports injuries. Fishing equipment coverage reimburses tackle, rods, reels, and related gear up to policy limits, which adds genuine value if you carry $3,000 or more in equipment. Skip it if you trailer your expensive gear to and from your boat rather than leaving it aboard.

Know What Drives Your Premium Up or Down

Once you’ve locked in your boat’s specifications, usage patterns, and coverage choices, the next step involves understanding exactly which factors push your premium higher or lower-and how to control the ones within your reach.

What Really Drives Your Boat Insurance Premium

Boat Specifications Set Your Premium Foundation

Your boat’s specifications form the foundation of your premium, but they’re only the starting point. A 25-foot center console with a single 300-horsepower outboard costs significantly more to insure than a 25-foot pontoon with twin 150-horsepower motors, even though both are 25 feet long. Insurance carriers weight horsepower heavily because higher-powered boats correlate with faster speeds, greater accident severity, and higher liability exposure. Older boats typically cost less to insure than newer ones when you choose Actual Cash Value coverage, since depreciation lowers replacement costs. However, age works the opposite direction with Agreed Hull Value because the gap between what you owe and what it’s worth shrinks. Boat type matters equally-fishing boats with offshore capability face higher premiums than recreational runabouts because offshore navigation exposes you to worse weather, equipment failure at distance from help, and saltwater corrosion.

Storage Location and Navigation Area Reshape Your Costs

Where you store and launch your boat dramatically reshapes your premium. Coastal Florida marinas charge roughly 40 to 60 percent more than inland Minnesota storage because hurricane risk, theft, and saltwater damage drive claims frequency higher in coastal zones. A boat that lives in a heated, enclosed slip inside a secure marina costs less than an identical boat sitting outside on a trailer in a parking lot. Navigation area restrictions vary by carrier-some limit coastal boats to 25 miles offshore, others to 50 miles, and some exclude offshore navigation entirely unless you pay extra. Hurricane-prone states like Florida often impose lower hull value limits (for example, 35 feet in length and $175,000 in value maximum in certain high-risk zones).

Experience and Claims History Function as Hidden Multipliers

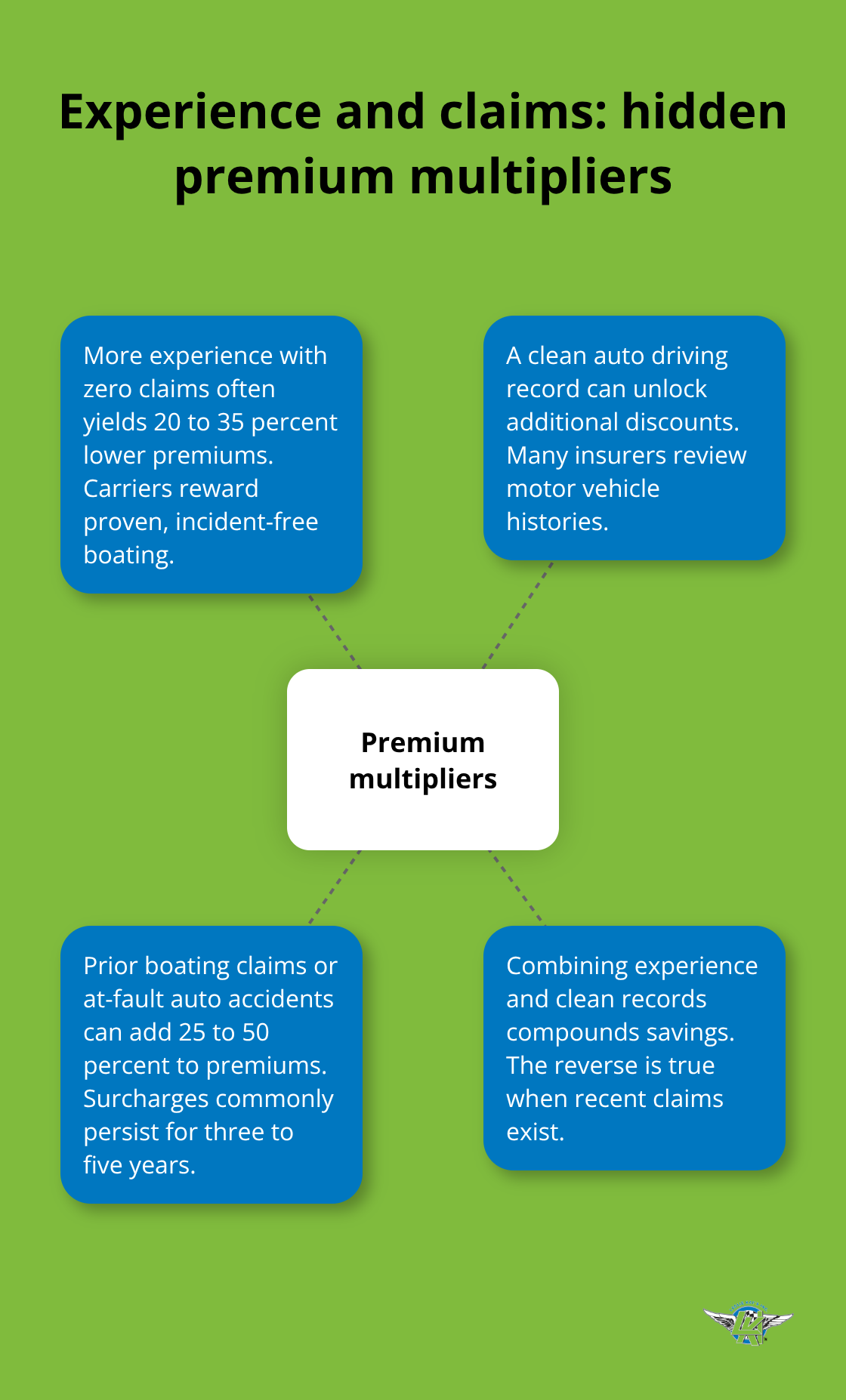

Your boating experience and claims history function as hidden multipliers on your entire premium. Someone with 15 years of boating experience and zero claims pays substantially less than a first-time boat owner with the same vessel, often 20 to 35 percent lower depending on the carrier. A clean auto driving record helps too-some insurers check your motor vehicle record and apply discounts for drivers with no tickets or accidents. Conversely, a prior boating claim or at-fault auto accident can increase your premium by 25 to 50 percent for three to five years.

Factors You Cannot Control

New boat discounts reward recent purchases because newer vessels have better safety systems, modern engines with fewer failures, and lower total loss costs. Marital status influences rates with some carriers, as married applicants occasionally qualify for lower premiums than single boaters. Homeownership also factors in-carriers sometimes view homeowners as lower risk and apply small discounts. These factors sit outside your control, but understanding them helps you anticipate what your premium might look like.

Factors You Can Control to Lower Your Premium

The real control you have centers on factors you can change. Maintain a clean driving record to qualify for better rates with most carriers. Complete a boating safety course through the U.S. Coast Guard Auxiliary or U.S. Power Squadrons to earn a 5 to 10 percent discount on your annual premium. Install onboard safety equipment like GPS or depth finders to qualify for additional discounts. Try a higher deductible to lower your annual premium, though this increases your out-of-pocket costs if you file a claim.

Final Thoughts

Building a custom boat insurance policy that protects your boat and fits your budget requires more than reading generic coverage descriptions online. You need someone who understands watercraft insurance, knows which carriers offer the best rates for your specific situation, and can explain why one policy structure makes sense for your boat while another doesn’t. We at Leslie Kay’s, Inc. specialize in watercraft insurance built for boaters like you, and as an independent agency, we shop multiple carriers to compare rates and benefits rather than pushing you toward one company’s standard offerings.

Our team works seven days a week answering questions and handling claims, which matters when you need help fast. Whether you’re comparing Agreed Hull Value versus Actual Cash Value coverage, deciding whether towing or medical payments make sense for your boating style, or filing a claim after an incident, you reach real people who understand boats and insurance. We handle motorcycle, RV, auto, and watercraft coverage across multiple states, which means we’ve worked with dozens of carriers and understand how different companies price and structure policies.

That experience translates directly into finding you the right custom boat insurance policy at the right price. Visit Leslie Kay’s, Inc. to discuss your boat and get a quote. Tell us your boat’s specifications, how you actually use it, and what coverage matters most to you.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.