ATV riding comes with real risks, and the right insurance protects you from financial disaster. At Leslie Kay’s, Inc., we know that all terrain vehicle insurance isn’t one-size-fits-all-your coverage needs depend on how you ride and where you ride.

This guide breaks down the coverage types that matter, the factors that shape your rates, and how to pick a policy that actually fits your situation.

What Coverage Types Actually Protect You on the Trail

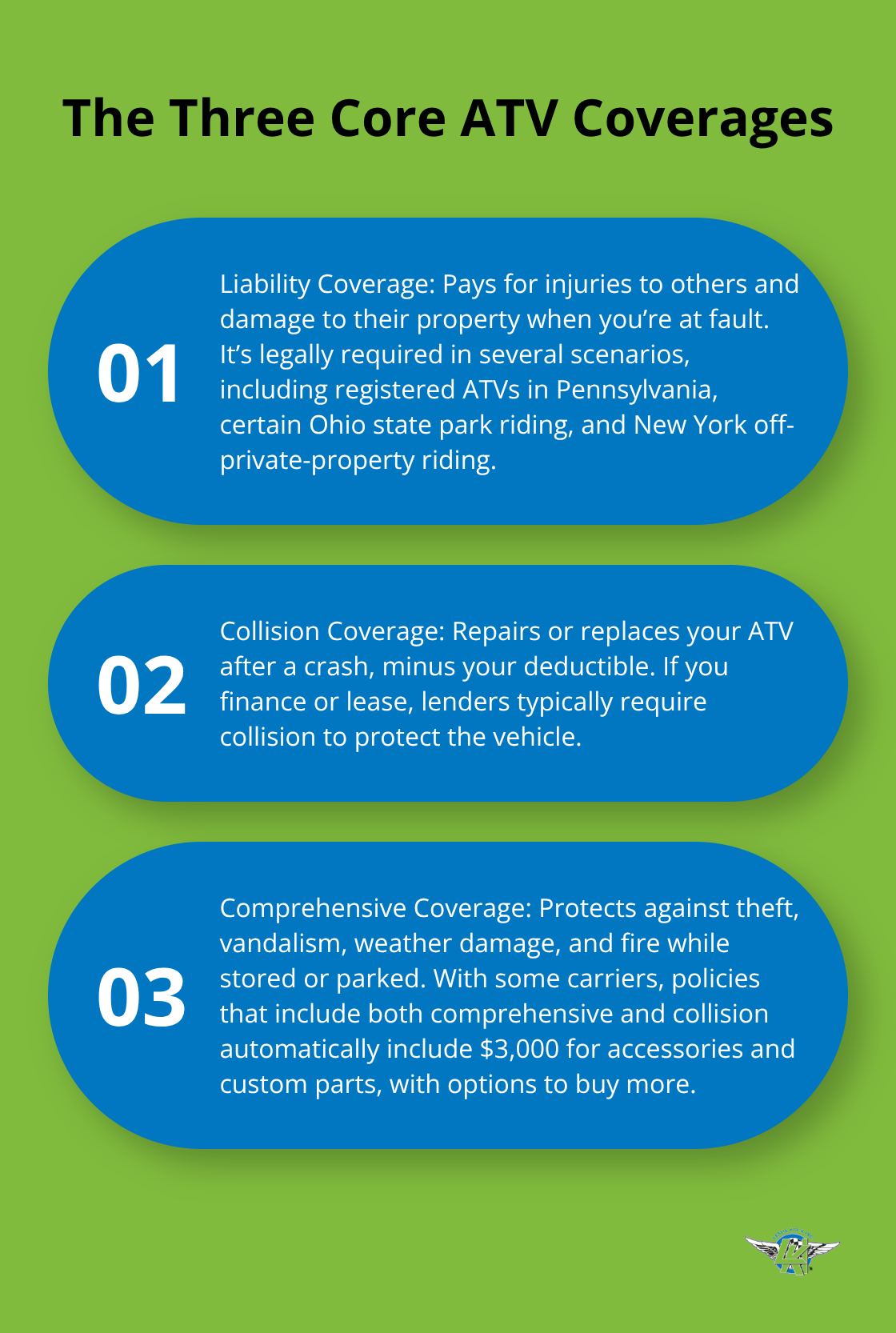

Liability Coverage: Your Legal Foundation

Liability coverage is non-negotiable if you ride anywhere near public land or someone else’s property. This coverage pays for injuries you cause to others and damage to their property, and it’s legally required in Pennsylvania for all registered ATVs, in Ohio when you ride state parks, and in New York for any off-private-property riding where minimums hit $25,000 for bodily injury and $10,000 for property damage. Many states also enforce liability requirements at specific parks and trail systems, so you must check local rules before you ride rather than guess. The U.S. Consumer Product Safety Commission reports that ATVs account for over 100,000 emergency room visits annually, which means medical bills and property damage claims spike fast when accidents happen.

A liability-only policy typically costs between $80 and $135 monthly, making it the baseline protection that keeps you from facing hundreds of thousands in personal liability. If you finance or lease your ATV, your lender will demand comprehensive and collision coverage to protect their investment in the vehicle itself.

Collision and Comprehensive: Protecting Your Machine

Collision coverage repairs or replaces your ATV after a crash, minus your chosen deductible, while comprehensive protection covers theft, vandalism, weather damage, and fire when your machine sits in storage or parked at a trailhead. Progressive automatically includes $3,000 of accessories and custom parts coverage on policies with both comprehensive and collision, and you can purchase additional coverage up to $30,000 if you’ve invested in upgrades or modifications.

A full coverage package combining liability, comprehensive, and collision typically costs $800 or more annually, though new or heavily modified machines can push toward $1,600 per year depending on engine size and your riding frequency.

Uninsured Motorist Protection: Covering the Gaps

Uninsured motorist protection covers you and your passengers if another rider causes injury without adequate insurance, which matters because not everyone riding carries the coverage they legally should. Engine size, vehicle age, location, and whether you’ve modified your ATV all drive your premium up or down, so you should obtain quotes from multiple carriers to reveal where you’ll pay less for the same protection level. Your next step involves understanding which specific factors most impact your rates-information that helps you make smarter choices about coverage limits and deductibles.

What Really Drives Your ATV Insurance Premium

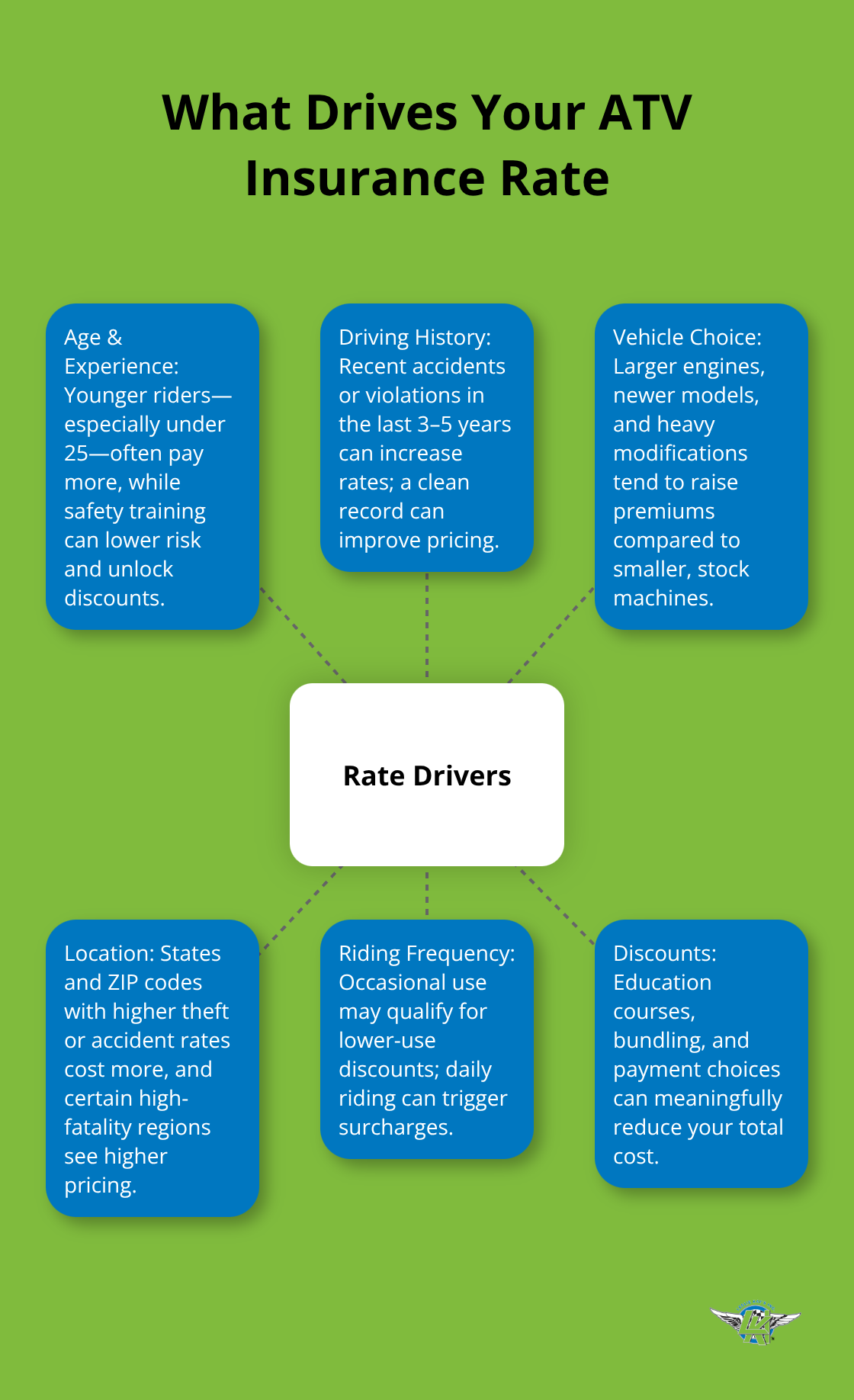

Rider Age and Experience Shape Your Costs Most

Your riding experience matters far more than insurance companies admit publicly. A new rider with a clean record pays significantly less than someone with recent accidents, but the real penalty hits riders under 25 without formal ATV safety training. Taking an ATV driver education course reduces your likelihood of accidents, and many insurers recognize this by offering discounts if you completed an approved course within the past three years through your state’s DMV.

Conversely, riders aged 16 and under face the steepest rates because nearly 300 deaths were among children under the age of 16. Your driving history in the past three to five years determines whether you qualify for lower rates or face increases that linger for years.

Vehicle Choice Amplifies Your Premium

Your vehicle choice amplifies these age-based costs dramatically. Larger engines cost more to insure than smaller ones, newer machines cost more than older models, and heavily modified ATVs with custom parts push premiums toward $1,600 annually compared to stock vehicles at $800 or less per year. Engine size, vehicle age, and whether you’ve added aftermarket parts all drive your premium up or down.

Location and Riding Frequency Create Pricing Variations

Location creates the final pricing shock. If you ride in Kentucky, one of the top five states for average ATV fatalities according to ATVSafety.gov, your insurer charges more because the diverse terrain of ridge tops and river bottoms increases accident risk. Your ZIP code itself matters because urban areas with higher theft rates spike your comprehensive coverage costs, while rural areas with active trail systems may see different pricing based on local accident frequency. How often you actually ride determines whether you qualify for lower-use discounts or face surcharges for daily recreational riding.

Discounts That Actually Reduce Your Bill

Annual payment discounts shave money off your total, and bundling your ATV policy with homeowners, auto, or motorcycle coverage under the same insurer typically reduces your year-round cost substantially. One insurer might heavily penalize your age while another rewards your safety course completion, which means getting quotes from three to five different companies reveals how dramatically rates vary for identical coverage. The most expensive mistake riders make involves choosing liability-only coverage to save $50 monthly, then facing a collision that totals a $5,000 machine they now cannot replace. Obtaining quotes from multiple carriers shows you where you’ll pay less for the same protection level-information that directly impacts which policy you select and how much you actually spend protecting your machine.

How to Choose the Right ATV Insurance Policy

Map Your Actual Riding Patterns

Start by mapping exactly how you ride. Daily commuting across rural trails demands different coverage than occasional weekend trips to a local park, and your answers determine whether you genuinely need collision coverage or can safely skip it. If you ride on private property only, liability becomes optional in most states, which means you could theoretically carry comprehensive alone to protect against theft and weather while stored. However, that strategy collapses the moment you cross onto public land or someone else’s property-one uninsured accident can obliterate years of savings.

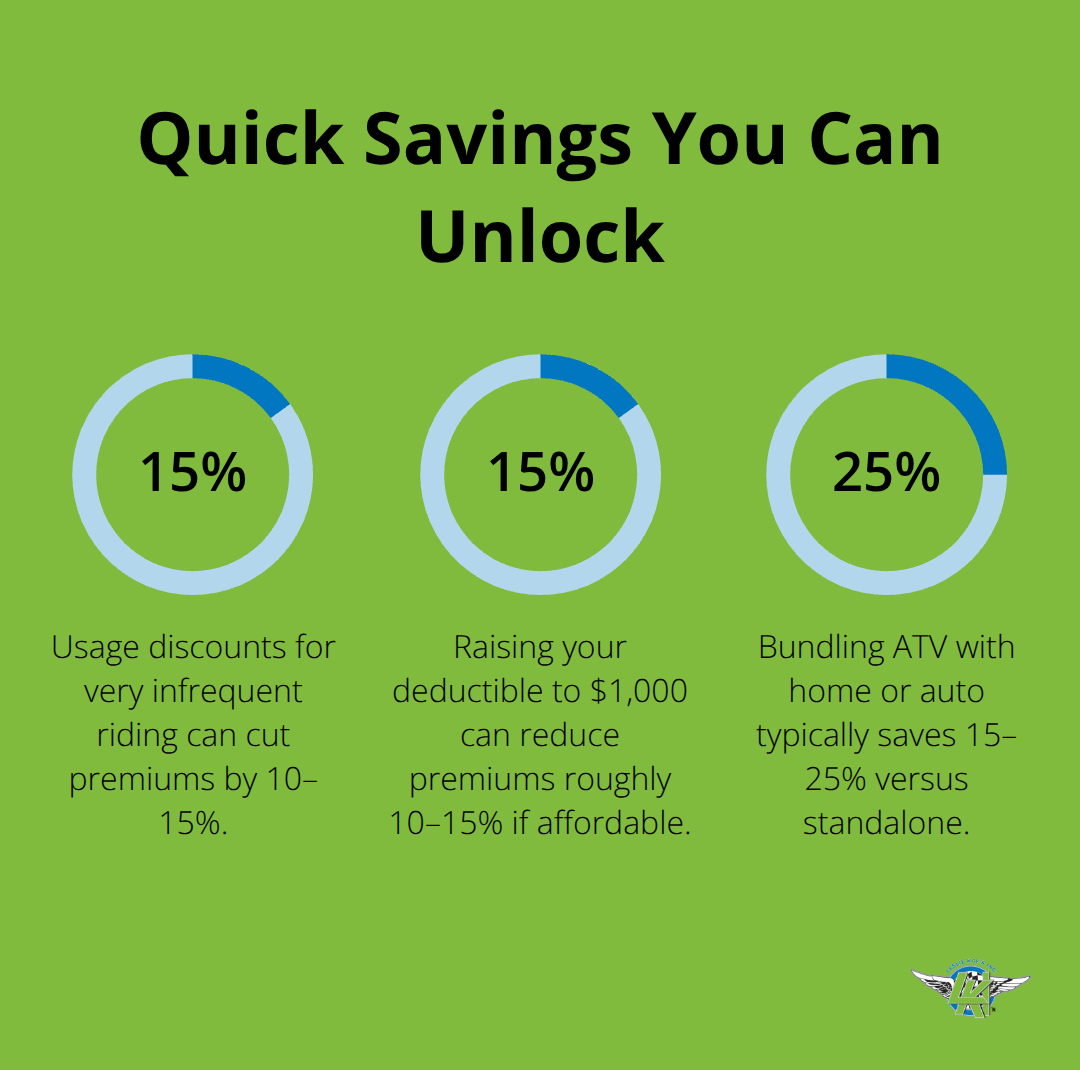

Assess whether you carry passengers (most ATVs aren’t designed for them, but many riders do anyway), whether your machine has $8,000 in custom parts, and whether you ride in Kentucky or other high-fatality states where insurers charge premiums reflecting elevated risk. Your riding frequency matters enormously: someone who rides five times yearly might qualify for usage discounts that cut premiums by 10-15%, while daily riders face surcharges.

Evaluate Your Coverage Needs Honestly

Once you answer these questions honestly, you’ll know whether a $1,000 annual policy with full coverage or an $80 monthly liability-only coverage actually fits your situation. The most expensive mistake riders make involves choosing liability-only coverage to save money, then facing a collision that totals a machine they now cannot replace. That math fails the moment an accident happens and you face replacing equipment from your own pocket.

Compare Multiple Carriers for Real Savings

Comparing carriers reveals stunning price variations for identical coverage. Progressive, GEICO, Liberty Mutual, and Foremost each price ATVs differently based on their underwriting models, and quotes from at least three carriers show you where you’ll save hundreds annually. When comparing, note which coverages come automatically included-Progressive includes $3,000 of custom parts coverage with comprehensive and collision, while other carriers force you to purchase that separately-because automatic inclusions can swing your true cost by $200 or more per year.

Optimize Deductibles and Bundling Discounts

Try setting your deductible at $500 if you can afford it; raising it to $1,000 cuts your premium roughly 10-15%, but only if you actually have $1,000 sitting aside for accidents. Review whether you qualify for bundling discounts by adding ATV coverage to existing homeowners or auto policies with the same insurer, which typically saves 15-25% compared to standalone ATV policies. When shopping for the best combination of rate, coverage and service, we help you match your actual riding needs and budget constraints.

Final Thoughts

ATV insurance protects you from financial ruin when accidents happen, and the right policy depends on three core factors: the coverage types you select, the rate drivers that affect your premium, and how honestly you assess your riding patterns. Liability coverage forms your legal foundation and is required in Pennsylvania, Ohio, New York, and at many public trails nationwide. Collision and comprehensive protection guard your machine against crashes and theft, while uninsured motorist coverage fills gaps when other riders lack adequate insurance.

Your age, riding experience, vehicle choice, location, and how often you ride all shape what you’ll pay annually, with rates ranging from $80 monthly for liability-only policies to $1,600 yearly for full coverage on new or heavily modified machines. One uninsured collision can total a $5,000 machine you cannot replace, or worse, leave you personally liable for another rider’s medical bills that exceed $100,000. The U.S. Consumer Product Safety Commission data showing over 100,000 ATV-related emergency room visits annually proves that accidents happen to real riders on real trails.

All terrain vehicle insurance quotes take minutes to obtain and cost nothing. Visit Leslie Kay’s, Inc. today to compare quotes from multiple carriers and protect your next adventure.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.