Buying your first motorcycle is exciting, but protecting it with the right insurance shouldn’t be an afterthought. At Leslie Kay’s, Inc., we know that motorcycle insurance for beginners can feel overwhelming with all the coverage options and state requirements to navigate.

This guide breaks down everything you need to know in plain language, from legal requirements to choosing the right policy for your riding style.

Why Motorcycle Insurance Matters

Motorcycle insurance legally required by state-it’s the law in almost all states. Only New Hampshire allows riders to skip it, but even there you remain financially liable for any damage you cause, which means one serious accident could wipe out your savings. Most states require at least liability coverage, with minimum limits that vary by state. A common format is 25/50/10, meaning $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $10,000 for property damage. These minimums sound substantial, but a single crash involving another vehicle or multiple people can easily exceed them, leaving you personally responsible for the difference. Authorities can fine you hundreds to thousands of dollars for riding without insurance, suspend your license, and create legal problems that follow you for years.

What Happens Without Coverage

A motorcycle accident differs dramatically from a fender-bender. National average motorcycle insurance costs around $500 to $1,500 per year, or roughly $40 to $125 monthly. That sounds manageable until you face what happens without it. If you cause an accident and injure someone, medical bills can reach tens of thousands of dollars. If you hit a parked car or property, repair costs add up fast. Without insurance, these bills come directly out of your pocket. Creditors can garnish your wages, and your assets become vulnerable. A used motorcycle costing $8,000 might seem cheap, but one uninsured accident could cost you ten times that amount in liability claims alone.

Medical Payments Coverage Protects You and Your Passengers

Liability coverage protects the other person, but medical payments or personal injury protection covers you. This coverage pays your medical costs after a crash, regardless of who caused it. If you ride with a passenger, verify that passenger medical coverage is included in your policy, since coverage varies by state. Young riders especially should prioritize this protection-riders under 25 face significantly higher injury risk and medical expenses. A helmet helps, but it won’t cover hospital bills, surgery, or rehabilitation costs. Medical payments coverage typically costs a small fraction of your overall premium but can save you from massive out-of-pocket expenses if injury occurs.

Understanding Your State’s Minimum Requirements

Each state sets its own liability minimums, and you must meet them to ride legally. Some states require uninsured or underinsured motorist coverage as well, adding another layer of protection. Your insurer can tell you exactly what your state mandates, and you should verify these requirements before you purchase a policy. Riding across state lines means you need to understand the rules in each state you visit. What satisfies one state’s requirements might fall short in another, leaving you exposed to fines or legal liability. Taking time to confirm your state’s specific minimums prevents costly mistakes down the road.

Types of Motorcycle Insurance Coverage Explained

Liability Coverage: Your First Line of Defense

Liability coverage forms the foundation of every motorcycle insurance policy, and it’s non-negotiable. This coverage splits into two parts: bodily injury liability pays for injuries you cause to other people, while property damage liability covers damage to their vehicles, homes, or fences. Neither has a deductible, so the full amount goes toward the claim. A standard format like 25/50/10 means $25,000 per person and $50,000 per accident for bodily injury, plus $10,000 for property damage. According to the Insurance Information Institute, these minimums exist in almost every state, but they’re often too low. A serious crash involving multiple vehicles can exceed these limits within seconds. Raising your limits to 50/100/25 or higher costs little extra monthly but protects your assets significantly. If you own a house, savings, or a car, higher limits are worth the investment because a judgment against you can follow you for years.

Collision and Comprehensive: Protecting Your Bike

Collision and comprehensive coverage protect your motorcycle itself, not the other person. Collision pays for repairs or replacement if you crash, while comprehensive covers theft, vandalism, weather damage, and fire. Both require a deductible-typically $250, $500, or $1,000-which you pay before insurance kicks in. A higher deductible lowers your monthly premium, but only if you can afford to pay it out of pocket after a loss. According to the National Insurance Crime Bureau, more than 40 percent of stolen motorcycles are recovered thanks to law enforcement efforts. If you park on the street or in an unsecured location, comprehensive coverage becomes essential. Storing your bike in a locked garage or adding security devices like a disc lock or GPS tracker can qualify you for discounts with many insurers. For financed motorcycles, lenders require both collision and comprehensive, so you have no choice there.

Uninsured and Underinsured Motorist Coverage

Uninsured and underinsured motorist coverage protects you when the other driver lacks insurance or insufficient coverage. This coverage pays your medical bills and bike repairs when an uninsured driver causes the accident. Some states require it; others don’t. If you live in an area with high uninsured driver rates, this coverage is practical protection. The cost is modest compared to the risk of facing medical bills and repair expenses with no way to recover them from the at-fault driver. Your next step involves comparing quotes from multiple insurers to find the right balance of coverage and cost for your specific situation.

How to Choose the Right Motorcycle Insurance Policy

Assess Your Riding Habits and Risk Factors

Your age, where you live, and how often you ride create vastly different insurance needs. An 18-year-old on a high-powered sportbike in Michigan will pay substantially more-around $500 extra annually-than a 30-year-old on the same bike in Iowa, according to the Insurance Information Institute. This isn’t theoretical; it’s the reality you face when you buy your first policy. Start by assessing your situation honestly. Do you commute daily on city streets, or do you ride weekends on rural roads? Will you carry a passenger regularly? Do you own a house or significant assets that need protection? These questions determine whether you need minimum liability or comprehensive coverage.

Young riders under 25 should expect higher premiums regardless of bike choice, but selecting a smaller or older motorcycle cuts costs dramatically. A five-year-old sportbike costs over 50% less to insure than a new model, and used cruisers run 30–40% cheaper, according to Progressive. This means your first bike choice directly impacts what you’ll pay monthly. If you finance the motorcycle, the lender will require full collision and comprehensive coverage, removing the decision-making burden but increasing your premium. Track days and off-road riding require special coverage that standard policies don’t provide, so confirm with your insurer whether your riding plans fall outside typical road use.

Compare Quotes From Multiple Insurers

Premiums vary wildly between carriers for identical coverage-this makes comparing quotes non-negotiable. Enter your ZIP code and specific bike model into at least three insurers’ quote tools; the same 25-year-old rider on a Honda CB500F might pay $450 annually with one insurer and $650 with another. The Insurance Information Institute reports that national averages run $500 to $1,500 yearly, but your actual quote depends entirely on your location and bike. Iowa consistently offers the lowest rates around $200–$350 annually, while Michigan tops the expensive list at $1,000–$2,500 or more. Remember that the lowest rate doesn’t always mean the best value-focus on finding the right combination of rate, coverage, and service.

Review Coverage Limits and Deductibles

Once you have quotes, compare deductibles carefully. A $500 deductible costs less monthly than a $250 deductible, but only choose the higher amount if you can actually pay it after an accident without financial hardship.

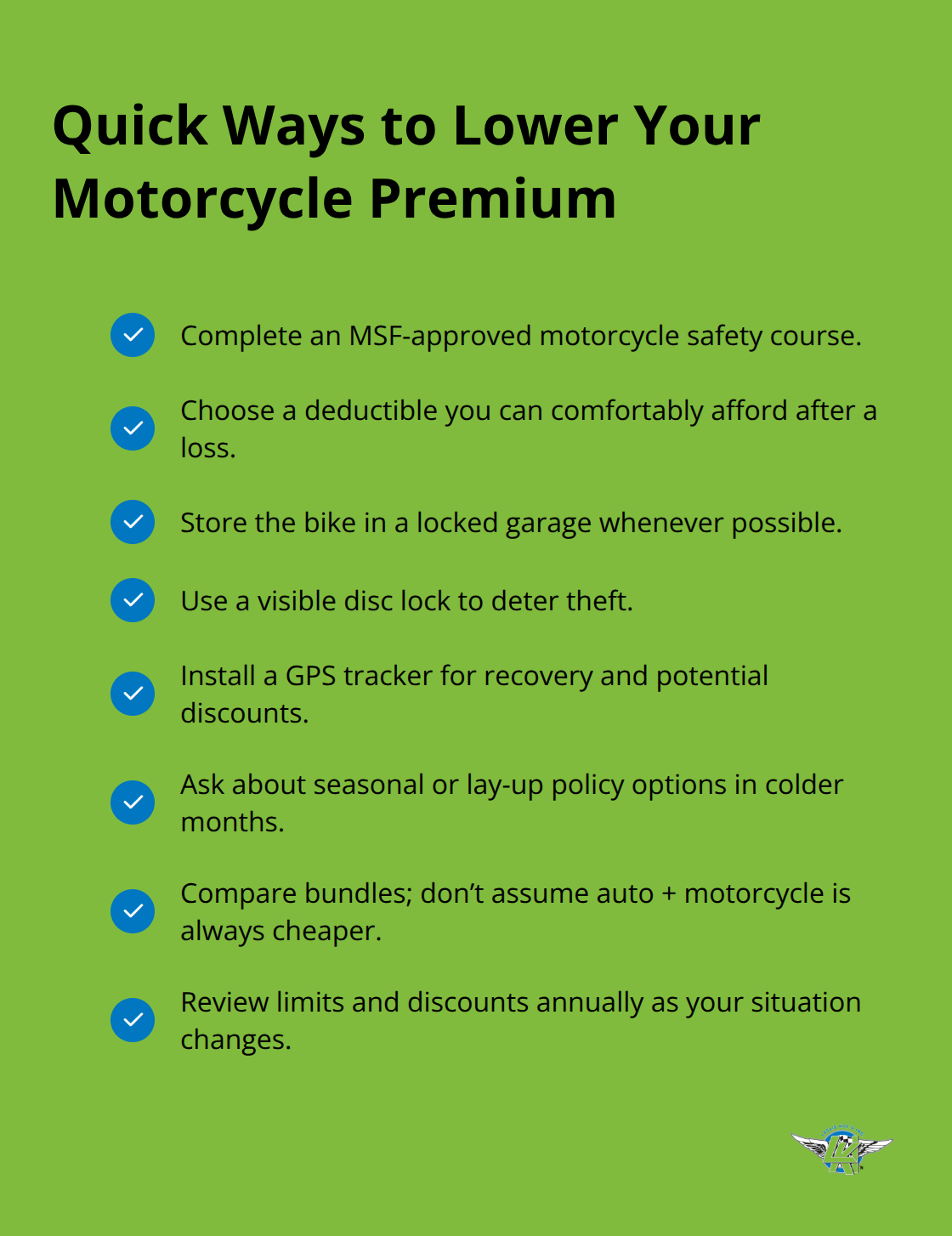

Completing a motorcycle safety course earns you a discount with most insurers, making the course investment worthwhile immediately. Adding security measures like storing your bike in a locked garage, installing a disc lock, or using a GPS tracker qualifies you for further discounts.

Some insurers offer seasonal or lay-up policies that reduce premiums when you’re not riding during winter months, cutting annual costs for riders in cold climates. Don’t bundle motorcycle insurance with auto insurance automatically-shop for the best combination of rate, coverage and service across separate carriers, since bundling isn’t always cheaper.

Final Thoughts

Liability coverage protects you legally in nearly every state, and one accident without it costs tens of thousands in medical bills and property damage. Collision and comprehensive coverage shield your motorcycle itself, while uninsured motorist protection safeguards you against drivers who lack adequate insurance. These protections prevent financial catastrophe and let you ride with confidence.

Your first action should be to request quotes from at least three insurers using your specific bike model and ZIP code, since premiums vary dramatically between carriers. A motorcycle safety course pays for itself through insurance discounts (typically 10–15% off), and secure storage in a locked garage or security devices like disc locks qualify you for additional savings. Young riders under 25 should prioritize smaller or used bikes to keep motorcycle insurance for beginners manageable, since a five-year-old sportbike costs over 50% less to insure than a new model.

We at Leslie Kay’s, Inc. shop multiple carriers to deliver competitively priced policies with hands-on support seven days a week. Get a quote from Leslie Kay’s in minutes to see exactly what protection costs for your situation.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.