Your ATV riding schedule shifts with the seasons, and your insurance should too. At Leslie Kay’s, Inc., we know that seasonal ATV insurance coverage needs to match when and where you actually ride.

Paying for full coverage during months your quad sits in storage wastes money. The right policy adjusts with your adventure calendar, protecting you when it matters most while keeping costs down.

Why Your ATV Coverage Needs Shift with the Seasons

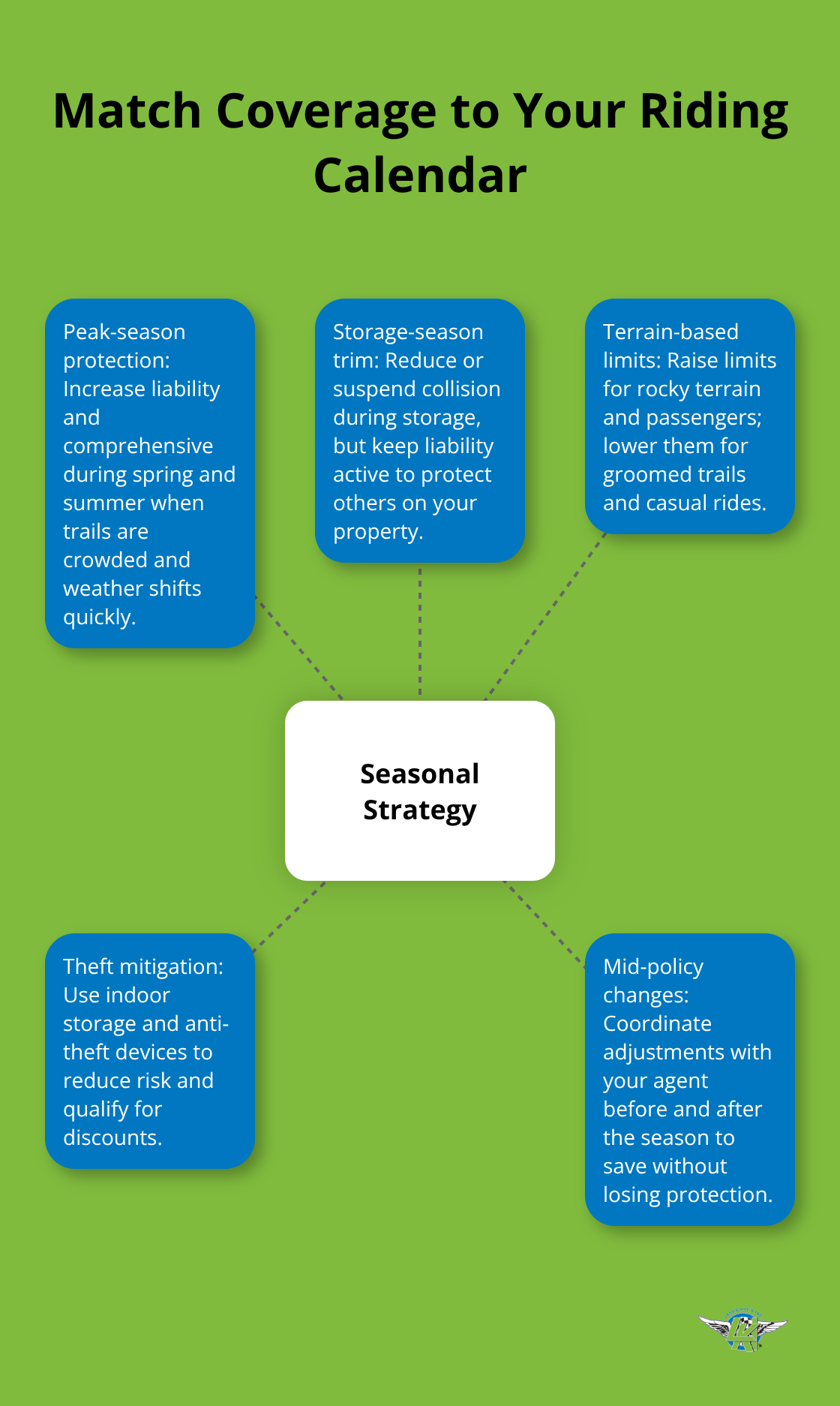

Spring and summer bring peak ATV riding season, and your exposure to risk climbs sharply during these months. More hours on trails mean higher chances of collision, theft from campsites, and damage from weather events you encounter on longer trips. Winter storage creates a different risk profile-your ATV sits vulnerable to theft, pest damage, and mechanical issues from sitting idle. Riders often waste hundreds annually by maintaining the same coverage year-round instead of adjusting for actual usage patterns. Your policy should reflect reality: maximum protection during peak months, streamlined coverage during storage periods, and strategic adjustments based on where and how often you actually ride.

When Your Risk Profile Changes Most

Your liability exposure peaks during spring and summer when trails are crowded and group rides happen frequently. Riding with passengers increases medical liability risk substantially, yet many riders don’t add passenger coverage until an accident forces the issue. Winter storage introduces different threats-theft rates spike in December and January according to property crime data, and ATVs stored improperly develop mechanical problems that comprehensive coverage can address. Collision and comprehensive coverage matter most during active riding months when you tackle variable terrain and weather conditions. If you ride year-round in mild climates, your needs stay constant; but if you store your ATV for three to five months, maintaining full collision coverage during storage wastes money you could redirect elsewhere. The key is matching your coverage intensity to your actual riding calendar, not a generic annual policy that assumes consistent usage.

Adjusting Coverage Without Losing Protection

Seasonal riders should reduce or suspend collision coverage during storage months while keeping liability active-liability protects others even when your ATV isn’t being ridden, especially if someone accesses your property. Many insurers allow mid-policy adjustments without penalties, so contact your agent before storage season to lower premiums on coverages you don’t need. Anti-theft devices and secure, indoor storage lower your theft risk significantly and often qualify you for premium reductions. If you ride high-risk terrain during peak season, increase your comprehensive limits then; if you stick to groomed trails, lower limits during those months work fine. Store your ATV in a garage rather than outdoors-the difference in theft exposure alone justifies the effort. Spring maintenance before riding season starts prevents mechanical failures that might otherwise trigger claims, and a quick pre-season inspection of brakes, battery, and fluids costs far less than collision repairs from preventable accidents.

Strategic Coverage Adjustments for Peak Season

As riding season approaches, you’ll want to review what coverage gaps exist in your current policy. Liability limits that worked for casual weekend rides may fall short when you tackle challenging terrain or ride with multiple passengers. Comprehensive coverage becomes especially valuable during spring and summer when weather patterns shift rapidly and theft from popular trailheads increases. Consider adding passenger coverage if your rides include friends or family members-medical expenses from passenger injuries can exceed your standard liability limits quickly. Your agent can help you identify which coverages to activate before peak season and which ones you can safely reduce during storage months, ensuring you pay only for protection you actually need.

Liability, Comprehensive, and Collision Coverage Across Seasons

Liability coverage forms the foundation of any ATV policy, and seasonal riders must understand how terrain and usage patterns affect their exposure. Spring and summer riding on crowded trails or through populated areas increases your liability risk substantially compared to winter storage months when your ATV sits stationary. Liability limits of $25,000 per person and $50,000 per accident work for casual weekend riders on groomed trails, but if you tackle rocky terrain, ride with passengers, or access areas near property lines, those limits fall dangerously short. A single accident involving a passenger injury can easily exceed $100,000 in medical costs, making higher liability limits essential during peak season.

Why Liability Stays Active Year-Round

Many seasonal riders make the mistake of maintaining minimum liability during storage months when they could safely reduce other coverages while keeping liability active. Liability protects others even when your ATV sits idle in your garage or driveway. If someone accesses your property and gets injured on your ATV, your liability coverage responds regardless of whether you were riding. This protection matters year-round, so you should never suspend liability entirely-only adjust other coverages based on your actual riding schedule.

Comprehensive Coverage During Storage and Active Seasons

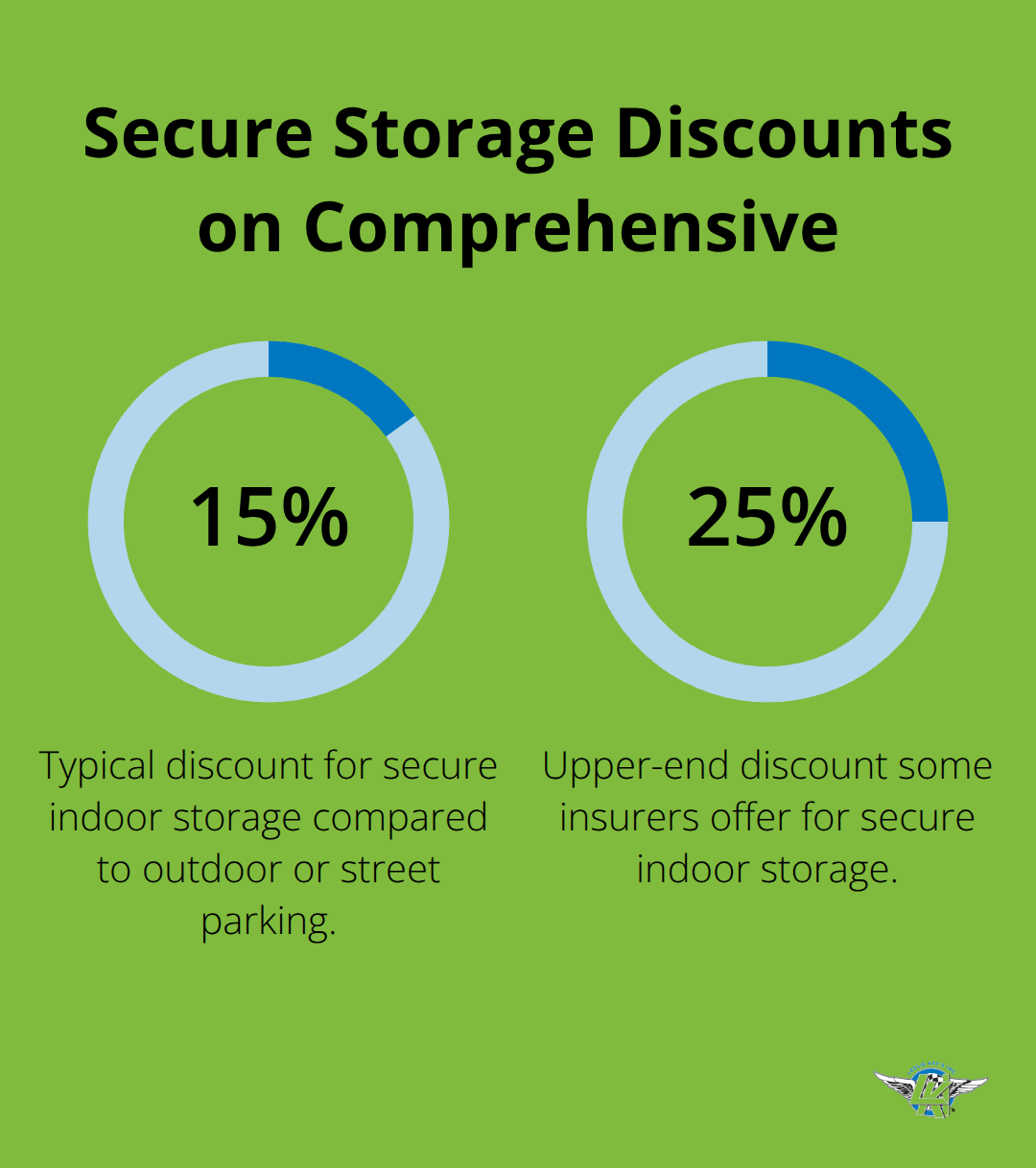

Comprehensive protection covers theft, vandalism, fire, hail, and weather damage regardless of who caused it, making it valuable year-round but especially critical during storage when theft rates peak in December and January according to property crime data. Indoor garage storage with a quality cover reduces theft risk dramatically, and insurers often offer 15 to 25 percent discounts for secure storage compared to outdoor or street storage. If you store your ATV outdoors or in an unsecured location, comprehensive coverage becomes non-negotiable since theft and vandalism claims spike during winter months when thieves target stored equipment.

Collision Coverage Timing and Adjustments

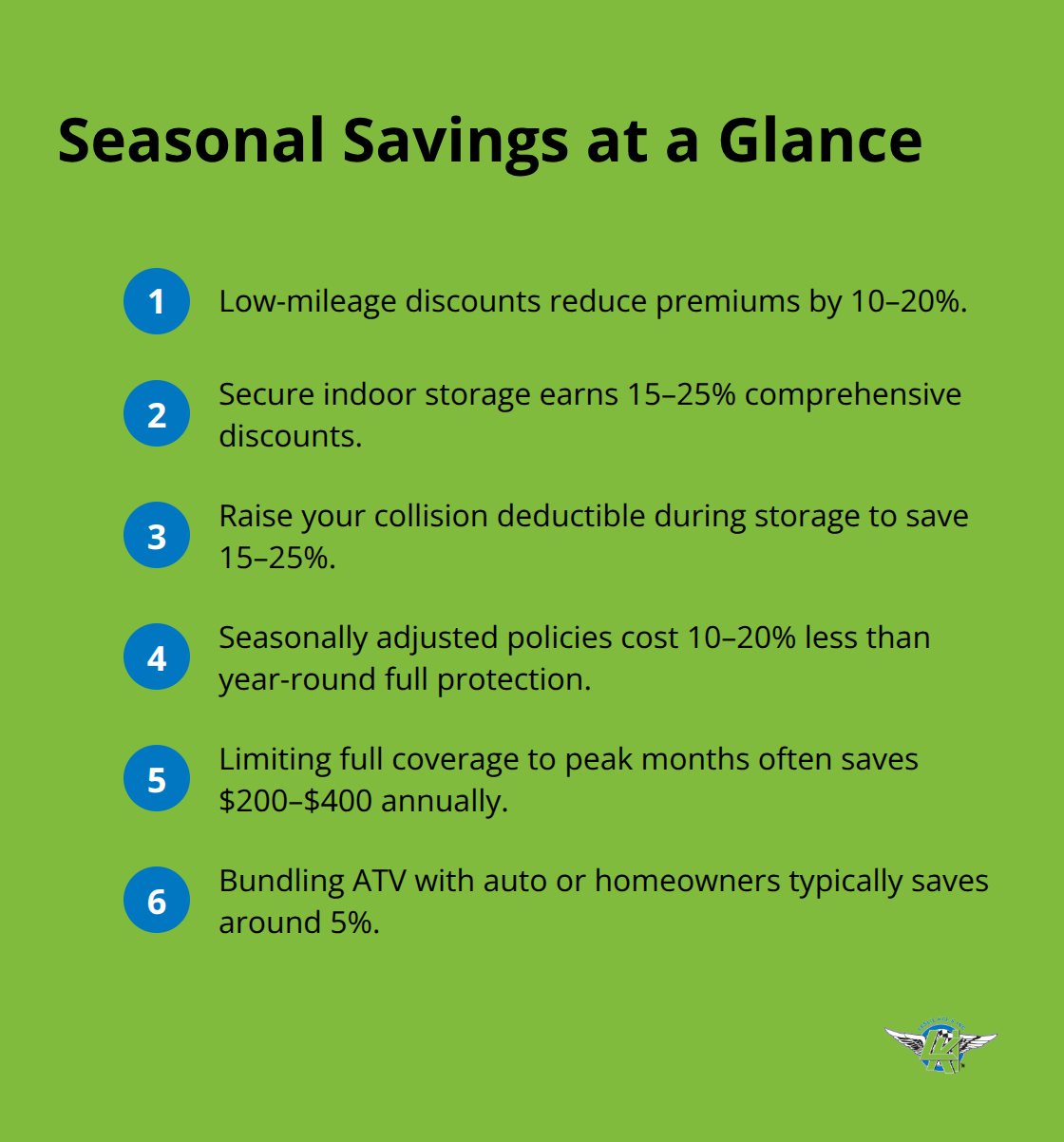

Collision coverage pays for damage from accidents and rollovers, which happens most frequently during spring and summer when you actually ride. During winter storage, collision coverage becomes unnecessary if your ATV sits in a garage, allowing you to suspend it entirely and reactivate it when riding season begins. Many insurers charge 10 to 20 percent less for policies that adjust coverage seasonally rather than maintain full protection all year. This flexibility means you can redirect savings toward other priorities without sacrificing protection when you need it most.

Protecting Custom Parts and High-Value Modifications

Accessories and custom parts coverage protects upgrades like upgraded seats, racks, lighting, and aftermarket tires, with automatic inclusion of $3,000 in coverage that you can increase up to $30,000 depending on your customizations. If your ATV has high-value modifications, document them with photos and receipts before storage season begins, then notify your agent about the upgrades so your policy reflects the actual replacement cost. Total loss coverage makes sense for newer ATVs, paying the full MSRP if your vehicle is totaled within one or two model years of purchase depending on whether you’re on a new or renewal policy. Seasonal riders who own high-performance or customized ATVs should review coverage limits before peak season since standard policies may undervalue heavily modified machines.

Your coverage choices during storage months set the stage for how well you’re protected when riding season arrives. The next section walks you through how to adjust your specific coverage limits based on the terrain you tackle and the frequency with which you actually ride.

Matching Coverage Limits to Your Actual Riding Habits

Your liability and collision limits should shift based on the terrain you tackle and how often your ATV leaves the garage. A rider who takes weekend trips on groomed trails in spring and summer needs different limits than someone who tackles rocky mountain passes with multiple passengers. Start by honestly assessing your peak season usage: how many days per month do you actually ride, what terrain dominates your trips, and how many passengers typically join you.

Setting Liability Limits That Match Your Terrain

Liability limits of $25,000 per person work for low-risk casual riding, but increase to $50,000 or $100,000 if you ride challenging terrain, carry passengers regularly, or access areas near private property. A single accident involving a passenger injury can easily exceed $100,000 in medical costs, making higher liability limits essential during peak season. If you ride year-round in mild climates, your limits stay constant throughout, but seasonal riders in cold climates should activate higher limits in spring and reduce them by mid-fall before storage begins.

Adjusting Collision Deductibles for Peak and Off-Seasons

Collision coverage deductibles deserve careful attention when you adjust your policy seasonally. A $500 deductible makes sense during peak season when you ride frequently and can absorb smaller repairs, but consider raising it to $1,000 during storage months if you maintain collision coverage, which saves 15 to 25 percent on premiums. Your agent can model different scenarios: full coverage for three months of peak riding costs substantially less than carrying identical limits year-round, and the savings often reach $200 to $400 annually depending on your ATV’s value and your location.

Capitalizing on Low-Mileage Discounts

Low-mileage discounts apply directly to seasonal riders since you accumulate fewer annual miles than full-time riders, yet many seasonal ATV owners never mention this to their agents. If you ride 500 to 1,500 miles annually during peak season, you qualify for discounts that can reduce premiums by 10 to 20 percent depending on your insurer. Insurers track mileage through declarations and claims history, so accurate reporting matters-underreporting mileage creates claim complications, while overreporting costs you unnecessary premiums.

Document your riding patterns for the past two years (mileage logs, trip dates, and terrain types) and share this data when requesting quotes, since insurers price policies based on actual usage, not worst-case assumptions.

Selecting Specialized Coverage for Your Season

Winter or summer specialized coverage depends entirely on your specific adventures: if you ride through snow or ice, add comprehensive coverage and consider uninsured motorist protection since winter conditions increase accident frequency; if you summer-camp with your ATV, add gear and equipment coverage for your camping setup and personal belongings, with coverage limits matching the actual value of items you carry on trips. Many riders add passenger medical payments coverage only during peak season when friends join rides, then remove it during storage months-this targeted approach cuts costs without eliminating protection when you need it. Spring maintenance prevents mechanical failures that could trigger claims, so inspect brakes, battery, and fluids before reactivating your policy each year. Contact your agent six weeks before peak season begins to activate seasonal coverage increases, and notify them two weeks before storage season to reduce unnecessary protections.

Final Thoughts

Seasonal ATV insurance coverage that matches your riding calendar protects you when it matters most while eliminating wasted premiums during storage months. Activate higher liability and comprehensive limits during peak riding season, reduce collision coverage when your ATV sits idle, and adjust passenger protection based on who actually rides with you. Your terrain and frequency determine the specific limits you need-rocky mountain passes demand higher liability than groomed trail weekends, and year-round riders maintain constant coverage while seasonal riders gain flexibility to adjust quarterly or monthly.

Getting the right protection without overpaying requires honest conversations with your agent about actual usage patterns. Document your riding days, mileage, and terrain type for the past two years, then share this data when reviewing your policy. Low-mileage discounts apply directly to seasonal riders, often reducing premiums by 10 to 20 percent, yet many owners never mention their limited annual miles, and bundling your ATV with auto or homeowners coverage typically saves around 5 percent on your overall policies.

Finding an agency that understands your ATV lifestyle means working with professionals who specialize in off-road vehicles and recognize that seasonal riders have different needs than full-time enthusiasts. At Leslie Kay’s, Inc., we work with multiple carriers to deliver customized seasonal ATV insurance coverage built specifically for your adventures, with hands-on claims support and seven-day-a-week service across multiple states. Contact us six weeks before peak season begins to adjust your coverage to match your actual riding calendar while keeping your premiums competitive-visit https://lesliekays.com to get started.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.