Your boat represents a significant investment, and standard insurance policies simply don’t protect it adequately. Water-based risks are fundamentally different from road hazards, which is why a comprehensive boat insurance plan is essential.

At Leslie Kay’s, Inc., we’ve seen too many boat owners discover coverage gaps only after an incident occurs. This guide walks you through what real boat insurance covers, why it matters, and how to select the right protection for your vessel.

What Boat Insurance Actually Covers

Boat insurance operates in two distinct parts: physical damage coverage and liability protection. Physical damage covers your hull, engine, onboard equipment, and accessories when things go wrong-whether that’s a collision with a submerged log, theft from your mooring, fire damage, or weather-related destruction. Most policies offer all-risk coverage, meaning losses are covered unless explicitly excluded in your contract. The critical distinction is how insurers value your boat when a total loss occurs. Agreed value policies pay a fixed amount you’ve established upfront, while actual cash value policies pay current market value minus depreciation.

For boats older than five years, agreed value makes more sense because it protects against steep depreciation hits.

Understanding Your Liability Exposure

Liability coverage is where many boat owners underestimate their exposure. This protection covers bodily injury and property damage you cause to others-including medical expenses, legal defense costs, and damages if you’re sued. Under the Oil Pollution Act of 1990, you could face cleanup liability if your boat causes an environmental spill, which is precisely why liability limits matter. Standard limits range from $100,000 to $500,000, but if you have substantial assets, carrying $1 million in liability protection is worth the modest premium increase.

Medical Payments and Uninsured Boater Protection

Medical payments coverage handles injuries to you, your family, and passengers aboard your boat with no deductible. Most policies let you choose per-person limits ranging from $500 to $5,000, and this coverage applies whether someone is boarding, on the water, or being towed. Uninsured and underinsured boater coverage protects you when another operator causes injury or damage but lacks adequate insurance-a realistic scenario since only three states legally require boat insurance.

Essential Add-On Coverage Options

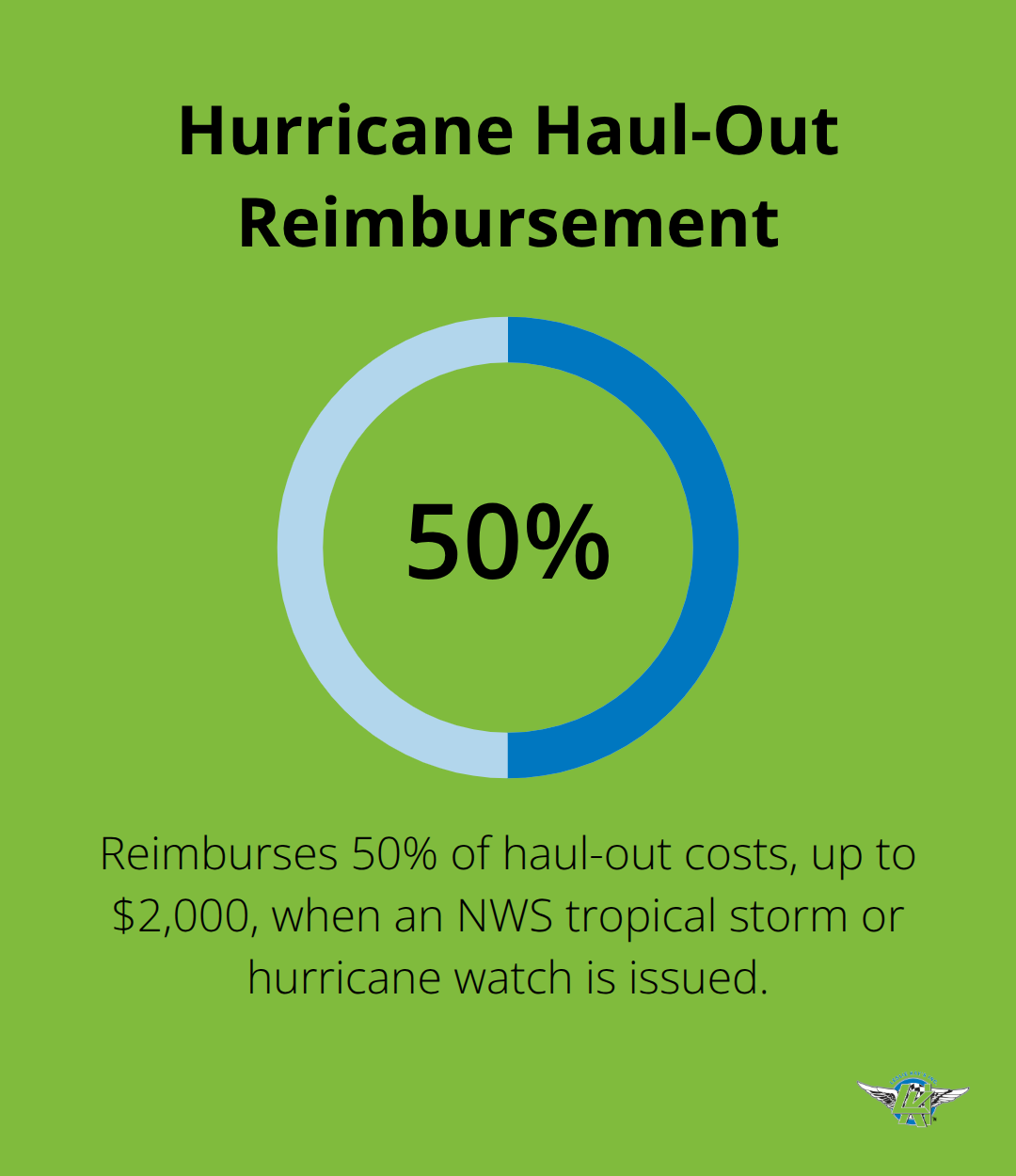

Additional coverage options address real expenses that occur regularly in boating. Emergency towing and assistance typically costs $38 to $100 annually and covers on-water towing, soft groundings, jump starts, and fuel delivery. Wreck removal coverage handles the legally required costs of removing a sunken vessel, which can easily exceed $10,000. Personal effects coverage protects fishing equipment, electronics, and clothing up to $10,000 with replacement cost value, meaning you receive what it costs to replace items today, not depreciated amounts. Hurricane haul-out coverage reimburses 50 percent of costs, up to $2,000, to move your boat to safety when the National Weather Service issues a tropical storm or hurricane watch.

These protections form the foundation of comprehensive boat insurance, but selecting the right combination for your specific vessel and boating habits requires careful evaluation of your actual usage patterns and risk exposure.

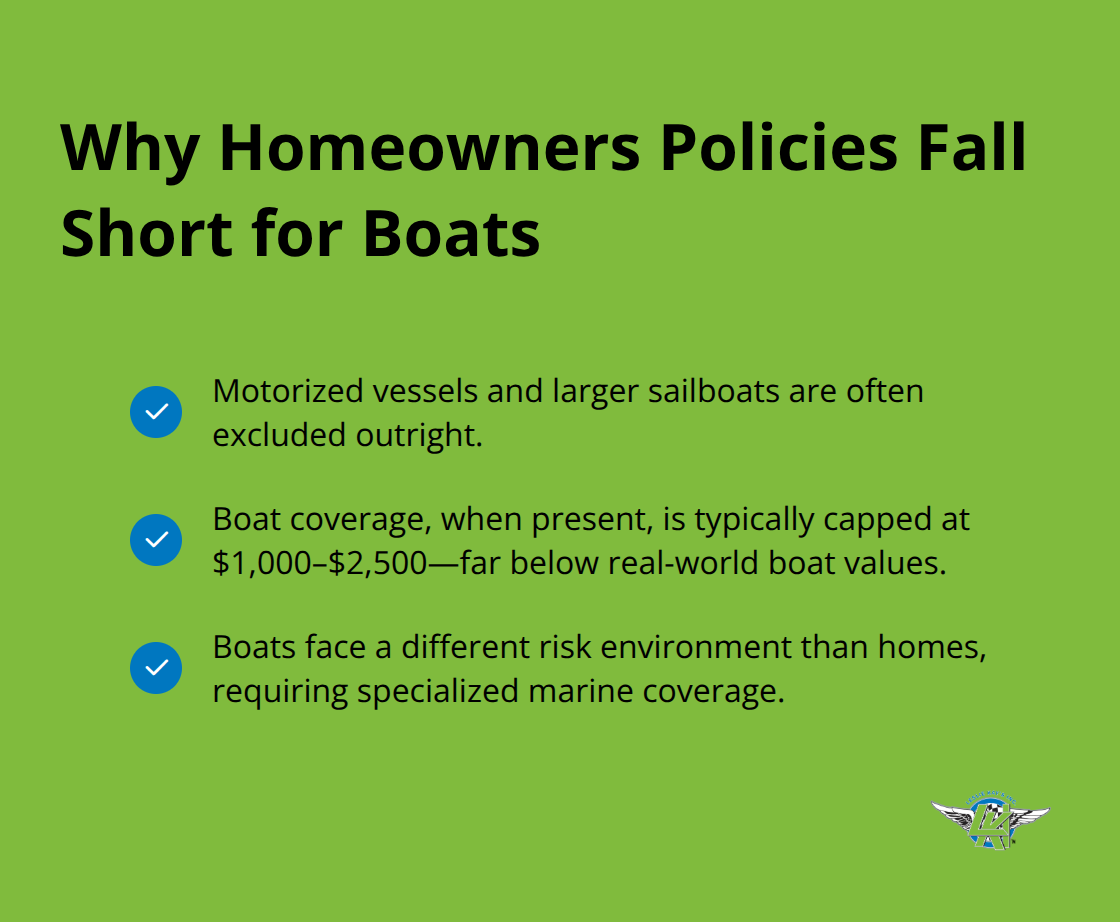

Why Your Homeowners Policy Won’t Cover Your Boat

Your homeowners insurance policy treats your boat as a minor afterthought, if it covers it at all. Most standard homeowners policies explicitly exclude motorized vessels and larger sailboats, leaving you with zero protection when your boat needs it most. Even policies that mention boats typically cap coverage at $1,000 to $2,500 for small vessels-which covers nothing when you’re dealing with a $50,000 fishing boat or a $200,000 cruiser. The exclusion exists because boats operate in a completely different risk environment than homes.

Why Water-Based Risks Demand Specialized Coverage

Water introduces saltwater corrosion, fuel spill liability, environmental cleanup costs, and collision scenarios that homeowners policies simply weren’t designed to handle. Insurance carriers that write homeowners coverage lack the marine expertise to price these risks accurately, so they avoid them entirely. This gap leaves boat owners dangerously exposed, thinking they’re protected when they’re actually one accident away from catastrophic out-of-pocket costs.

Environmental Liability Gaps That Homeowners Policies Ignore

Water-based liability creates exposures that land-based policies ignore entirely. If your boat causes an environmental spill under the Oil Pollution Act of 1990, you could face cleanup liability with no homeowners coverage whatsoever. Guest injuries from water sports like wakeboarding or tubing aren’t covered under homeowners policies, but specialized boat insurance includes water sports liability as a standard or add-on option.

Regulatory Requirements Your Homeowners Policy Can’t Meet

State and local boating regulations compound this problem because they vary dramatically across jurisdictions. Only three states legally require boat insurance, but marinas in coastal areas almost universally demand liability coverage before granting dock access, making your homeowners policy completely irrelevant to their requirements. Lenders financing boat purchases also mandate full coverage including collision and comprehensive protection, which homeowners policies cannot provide.

Finding Coverage That Matches Your Boating Reality

Specialized boat insurance addresses these specific water-based exposures, giving you protection that actually matches your boating reality rather than forcing you into an inadequate homeowners framework that was never intended for watercraft. The right marine policy covers your actual liability exposure, protects your vessel from water-specific hazards, and satisfies lender and marina requirements-something no homeowners policy can accomplish. Understanding these gaps sets the stage for evaluating what comprehensive boat insurance actually delivers and how to select the right coverage limits for your specific vessel and boating habits.

Matching Your Boat to the Right Coverage

Start with an honest assessment of how you actually use your boat, not how you think you use it. A fishing boat that stays within 50 miles of your home port requires different coverage than a cruiser making coastal runs from Florida to the Carolinas. Most carriers price policies based on navigation territory, so limiting coverage to a smaller area near your home port can reduce your annual premium significantly. If you fish inland lakes during summer months and store the boat for six months, a longer lay-up period matching your actual off-season generates discounts that can cut 10 to 20 percent from your annual cost.

Vessel Type and Operator Experience

Boat type matters enormously-a 20-foot pontoon costs far less to insure than a 35-foot speedboat with twin outboards, primarily because performance boats accumulate claims at higher rates. Your age and boating experience factor in as well; operators under 25 typically pay higher premiums, while completing an approved boating safety course like Boat-Ed can lower your rate by 5 to 15 percent depending on the carrier. Document your vessel’s exact specifications-length, horsepower, year, hull material, and whether it’s freshwater or saltwater-because misrepresenting these details voids coverage when claims occur.

Liability Limits and Asset Protection

Liability limits and asset protection should reflect your actual liability exposure and net worth. Most boat owners carry $100,000 to $500,000 in liability limits, but this proves genuinely inadequate if you have a home, retirement savings, or income worth protecting. Consider higher limits to shield substantially more of your assets, as the cost difference between moderate and comprehensive coverage is often minimal.

Deductibles and Valuation Methods

Deductibles typically run 1 to 5 percent of your boat’s insured value; raising your deductible from $500 to $1,000 or $2,500 reduces premiums by 10 to 25 percent if you have cash reserves to cover that amount. Choose agreed value rather than actual cash value for boats older than five years-agreed value eliminates depreciation disputes and pays a fixed amount you’ve established upfront for total losses.

Strategic Add-On Coverage Selections

Emergency towing with on-water assistance costs $38 to $100 annually and covers on-water towing, soft groundings, jump starts, and fuel delivery with zero out-of-pocket costs since the dispatch center pays the tow operator directly. Water sports liability protection matters if guests ever participate in wakeboarding, tubing, or knee boarding-standard boat policies exclude these activities unless you specifically add coverage. Fishing equipment coverage pays replacement cost value up to $10,000, covering your rods, reels, electronics, and carry-on items at today’s replacement cost rather than depreciated amounts. Hurricane haul-out coverage reimburses 50 percent of moving costs (up to $2,000) when the National Weather Service issues a tropical storm or hurricane watch, protecting your investment when severe weather threatens coastal areas.

Final Thoughts

Comprehensive boat insurance protects your investment in ways that standard homeowners policies simply cannot match. Boats operate in a fundamentally different risk environment than homes or vehicles, and your protection must reflect that reality. Physical damage coverage shields your hull and equipment from collisions, theft, and weather damage, while liability protection covers the injuries and property damage you cause to others-including environmental cleanup costs that can reach hundreds of thousands of dollars. Medical payments and uninsured boater coverage handle the human costs when accidents occur.

Selecting adequate protection requires you to assess your vessel type, navigation territory, and actual usage patterns rather than guessing at coverage needs. Compare liability limits and deductible options against your net worth and assets, since most boat owners carry $100,000 to $500,000 in liability limits but higher coverage costs surprisingly little more. Evaluate add-on coverage for towing, water sports liability, fishing equipment, and hurricane haul-out protection based on how you actually use your boat.

The cost of a comprehensive boat insurance plan is far lower than most boat owners expect, with annual premiums typically running 1 to 5 percent of your boat’s value. Bundling boat insurance with auto or homeowners policies generates additional savings, and completing an approved boating safety course reduces premiums by 5 to 15 percent while improving your skills on the water. Contact us at lesliekays.com to get quotes and secure the comprehensive boat insurance protection your investment deserves.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.