Motorcycle riders face unique insurance challenges that standard auto policies simply don’t address. At Leslie Kay’s, Inc., we know that motorcycle insurance for riders requires specialized coverage tailored to the specific risks you encounter on the road.

This guide walks you through the coverage types that matter, how they differ from traditional auto insurance, and how to select a policy that matches your riding style and needs.

Why Motorcycle Insurance Costs More and Works Differently

The Real Risk Behind Higher Premiums

Motorcycles carry substantially higher injury and fatality rates than cars, which directly translates to insurance premiums that reflect actual risk data. The National Highway Traffic Safety Administration reports that motorcyclists are 28 times more likely to die in a crash than passenger vehicle occupants, and five times more likely to be injured. This isn’t abstract risk-it’s the reason insurers price motorcycle policies differently and require coverage types that auto policies simply don’t offer. Riders lack the protective shell of a vehicle, so medical expenses and liability exposure climb dramatically after an accident. Additionally, theft rates for motorcycles run higher than for cars in most regions, making comprehensive coverage essential rather than optional.

Weather exposure, visibility challenges, and the physics of two-wheeled riding create loss patterns that auto insurers have studied for decades, resulting in specialized underwriting that goes far beyond standard auto formulas.

Custom Parts and Equipment Protection

The coverage gap between motorcycle and auto insurance reflects these realities in concrete ways. Auto policies don’t address custom parts and equipment, which riders often invest thousands into upgrading their bikes. You’ll need an accessories endorsement to protect chrome, saddlebags, and performance modifications. Progressive and GEICO both offer these endorsements, allowing you to add coverage up to $30,000 for aftermarket equipment. Without this protection, your custom investments remain uninsured if theft or damage occurs.

Medical Payments and Injury Coverage

Medical payments coverage takes on greater importance for motorcycle riders since a crash can leave you with hospital bills that health insurance alone won’t fully cover. Some states allow riders to stack medical payments across multiple policies for added protection. This coverage pays your medical costs regardless of fault, addressing the reality that motorcycle accidents produce more severe injuries than typical auto collisions.

Uninsured Motorist Protection

Uninsured motorist coverage becomes genuinely critical for riders because you’re more exposed on the road and face higher injury risk from other drivers. This coverage pays your medical costs if an uninsured driver hits you, protecting you against drivers who carry insufficient or no insurance at all. Many riders choose uninsured and underinsured motorist limits that match or exceed their liability limits for comprehensive protection.

Liability Limits and Asset Protection

Liability limits also require closer attention for motorcycle riders. If you cause a serious accident, your personal assets become exposed, so many riders choose limits well above their state’s minimum requirement. A standard auto policy adapted for a motorcycle leaves dangerous gaps in protection. The specialized coverage structures that carriers like Progressive and GEICO offer account for these distinct exposures, but the key insight is that you need a policy built for motorcycle risks rather than forced into a generic framework designed for four-wheeled vehicles. Understanding these coverage differences positions you to make informed decisions about which protections matter most for your riding style and circumstances.

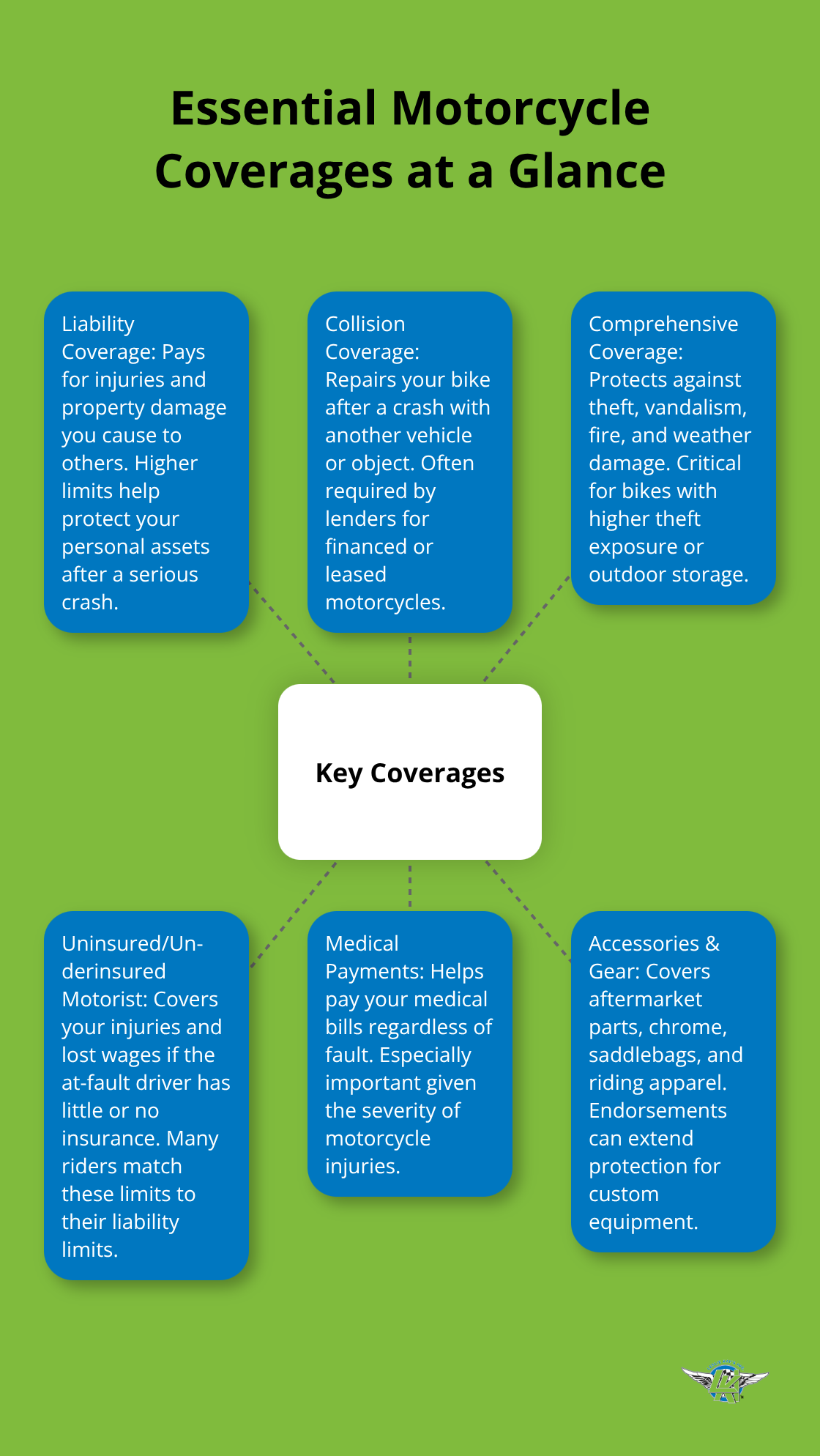

Essential Coverage Types for Motorcycle Riders

Liability Coverage: Your First Line of Legal Protection

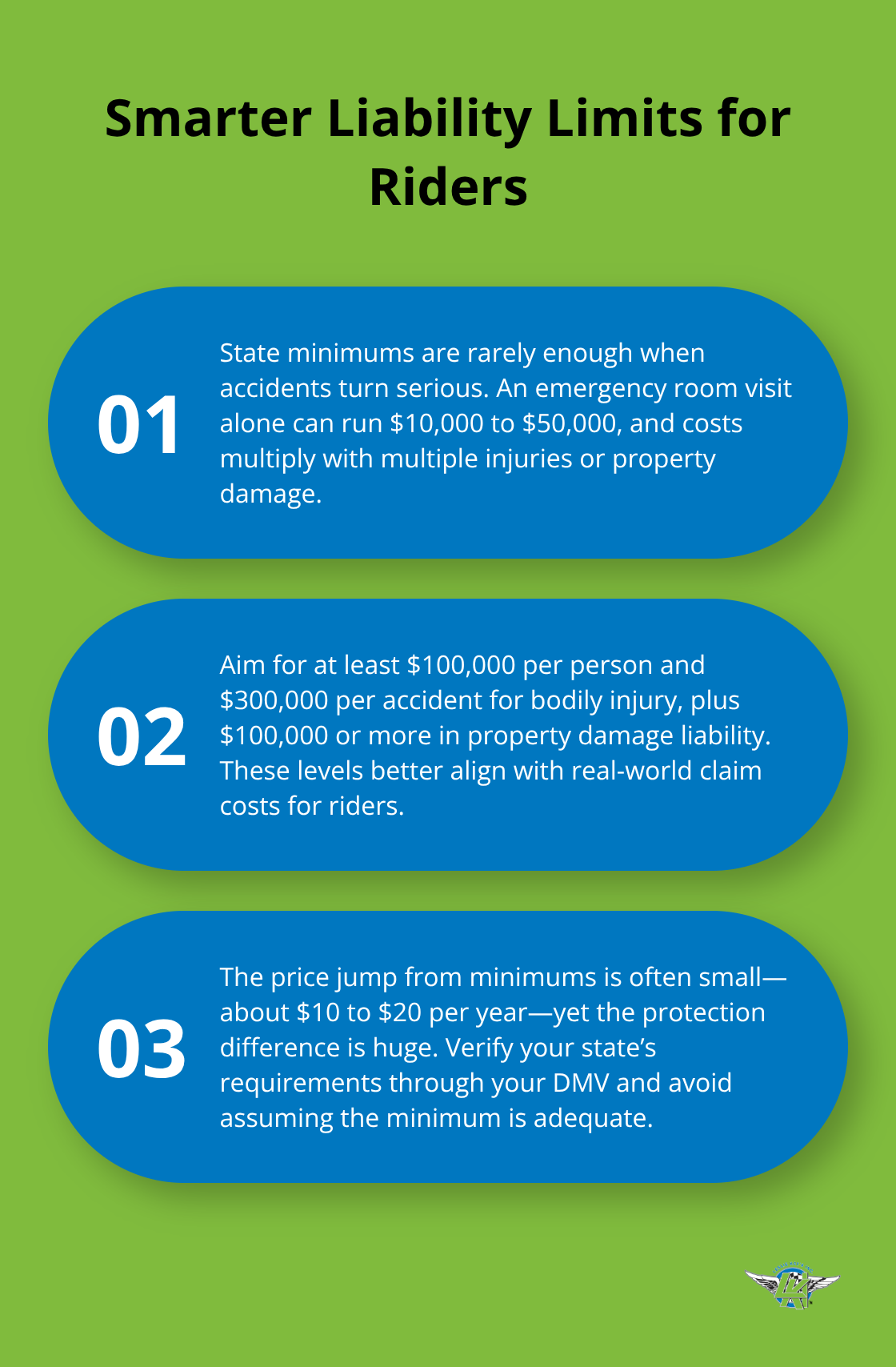

Liability coverage is mandatory in nearly every state, and the minimum limits your state requires are almost certainly too low. Most states set minimum bodily injury liability at $15,000 to $25,000 per person, which sounds adequate until you’re responsible for a serious accident. A single emergency room visit can cost $10,000 to $50,000, and if you injure multiple riders or cause property damage, those minimums evaporate instantly. We recommend carrying at least $100,000 per person and $300,000 per accident for bodily injury liability, with property damage liability of $100,000 or higher. These higher limits cost only marginally more than minimums-often $10 to $20 extra per year-but they shield your personal assets if you’re found at fault in a serious crash. Check your state’s specific requirements through your DMV, but never assume the minimum is enough.

Collision and Comprehensive: Protecting Your Bike

Collision coverage pays for damage to your motorcycle when you hit another vehicle or object, while comprehensive coverage protects against theft, vandalism, fire, and weather damage. The critical decision here involves your deductible: a $500 deductible costs more monthly than a $1,000 deductible, but you’ll pay out of pocket for smaller claims. If you financed or leased your bike, your lender requires both collision and comprehensive coverage, so that decision is made for you. For bikes worth under $5,000, liability-only coverage might tempt you financially, but one accident wipes out that savings and leaves you unprotected. Progressive and GEICO both use original equipment manufacturer parts for repairs when you carry collision and comprehensive, which matters because aftermarket parts lower your bike’s resale value and durability.

Uninsured Motorist Coverage and Medical Protection

Uninsured and underinsured motorist coverage is where riders face genuine exposure that auto drivers don’t fully appreciate. You’re far more vulnerable on a motorcycle when another driver hits you, and many drivers carry minimal or no insurance at all. This coverage pays your medical bills and lost wages if an uninsured driver causes your accident, protecting you regardless of that driver’s ability to pay. Many riders match their uninsured motorist limits to their liability limits, so if you carry $100,000 in liability, you’d carry $100,000 in uninsured motorist protection. Medical payments coverage adds another layer by covering your treatment costs regardless of fault, and some states allow you to stack this across multiple policies for additional protection.

Roadside Assistance and Gear Protection

Towing and roadside assistance costs roughly $19 per year through carriers like Progressive but can save you hundreds if your bike breaks down miles from home. Finally, consider coverage for safety apparel-helmets, jackets, and boots get damaged in crashes and can cost $2,000 to $5,000 to replace. This coverage pays replacement costs minus your deductible, protecting gear that regular policies ignore entirely. Document your accessories and gear with receipts and photos before you need a claim, because insurers require proof of value when processing these claims. Once you understand what coverage protects you, the next step involves comparing quotes from multiple carriers to find the policy that matches both your budget and your riding patterns.

How to Choose the Right Motorcycle Insurance Policy

Match Coverage to Your Riding Habits

Your riding habits determine which coverage matters most and where you can safely reduce costs. A weekend cruiser rider who logs 2,000 miles annually faces different risk than a commuter covering 12,000 miles yearly through heavy traffic. Start by assessing your riding habits and risk factors when requesting quotes from carriers. Usage-based or telematics programs reward safe riders with discounts tied to actual riding behavior rather than assumptions. If you ride infrequently, a pay-as-you-ride discount can cut your premium significantly compared to standard pricing. Conversely, high-mileage commuters need robust collision and comprehensive coverage since exposure increases with every mile.

Account for Storage and Location Factors

Your storage location influences pricing substantially-bikes stored in secure garages cost less to insure than those parked on the street in high-theft areas. When you contact insurers for quotes, provide consistent information across all carriers: your bike’s year, make, model, and VIN; all regular riders; your state’s address; and your actual annual mileage. This approach ensures apples-to-apples comparisons rather than inflated quotes based on assumed usage.

Shop Multiple Carriers Aggressively

Getting quotes from at least three carriers reveals price variations that often exceed $300 annually for identical coverage. Most online quoting takes fifteen minutes and applies discounts automatically. Don’t accept the first quote-shop aggressively because carriers price risk differently based on their claims data and target customer profiles. When you compare quotes from multiple insurers, ensure deductibles, liability limits, and coverage types match exactly across quotes, then note the price difference. The average cost of motorcycle insurance for a standard bike is $68 per month for minimum coverage and $148 for full coverage.

Optimize Deductibles and Liability Limits

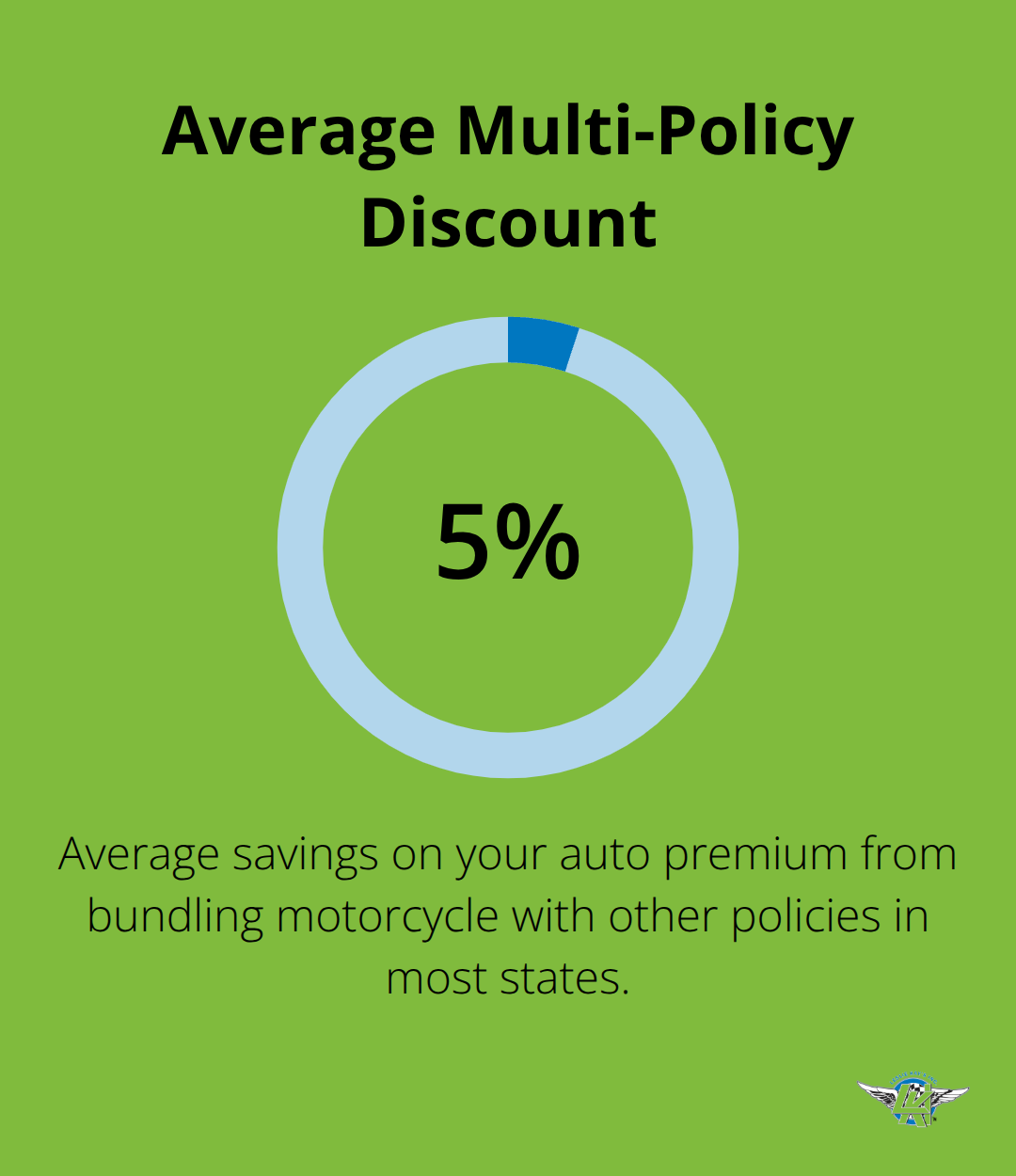

A $1,000 deductible versus $500 typically saves $100 to $200 yearly, but only choose higher deductibles if you can comfortably cover that out-of-pocket cost after a claim. State minimum liability limits vary significantly, so verify your state’s requirements through your DMV before selecting limits. Most riders benefit from carrying limits at least double the state minimum since the marginal cost remains minimal. Try bundling your motorcycle policy with auto, homeowners, or renters coverage to capture multi-policy discounts averaging around 5% on your auto premium in most states. Independent agencies and major carriers all offer these bundling savings automatically when you quote multiple products.

Review and Update Annually

Review your policy annually or after major changes to your bike or riding habits, since coverage that protected you last year might leave gaps now. This practice keeps your protection aligned with your current situation and riding patterns.

Final Thoughts

Motorcycle insurance for riders succeeds when it matches your actual riding patterns, bike value, and risk exposure rather than forcing you into a generic policy designed for cars. The coverage types we’ve outlined-liability, collision, comprehensive, uninsured motorist protection, and specialized add-ons like gear coverage-work together to address the genuine vulnerabilities riders face on the road. Your state’s minimum liability limits exist as a legal floor, not a protection ceiling, and carrying limits well above those minimums costs surprisingly little while shielding your personal assets from serious accidents.

Gathering quotes from at least three carriers using identical information about your bike, riding habits, and desired coverage levels reveals price variations that often exceed $300 yearly for the same protection. Resist the temptation to strip coverage to bare minimums just to lower your monthly payment, since one accident can erase years of premium savings and leave you financially exposed. Your deductible choices, storage location, and annual mileage all influence which coverage matters most for your situation.

We at Leslie Kay’s, Inc. specialize in motorcycle insurance and understand that riders need more than generic quotes and standard policies. Whether you ride weekends or commute daily, own a cruiser or sport bike, or carry custom equipment worth thousands, we shop multiple carriers to find customized coverage that protects your specific riding style and adventures. Contact us today to explore policies that deliver the protection you actually need without paying for coverage you don’t.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.