ATV riders who cross state lines face a confusing patchwork of insurance requirements. Each state sets its own liability minimums, coverage rules, and registration standards, leaving many riders underprotected when they venture beyond their home territory.

At Leslie Kay’s, Inc., we’ve seen firsthand how multistate ATV insurance gaps leave riders vulnerable. This guide walks you through the coverage differences, protection options, and common policy exclusions you need to know before hitting trails across multiple states.

Understanding State-by-State ATV Insurance Requirements

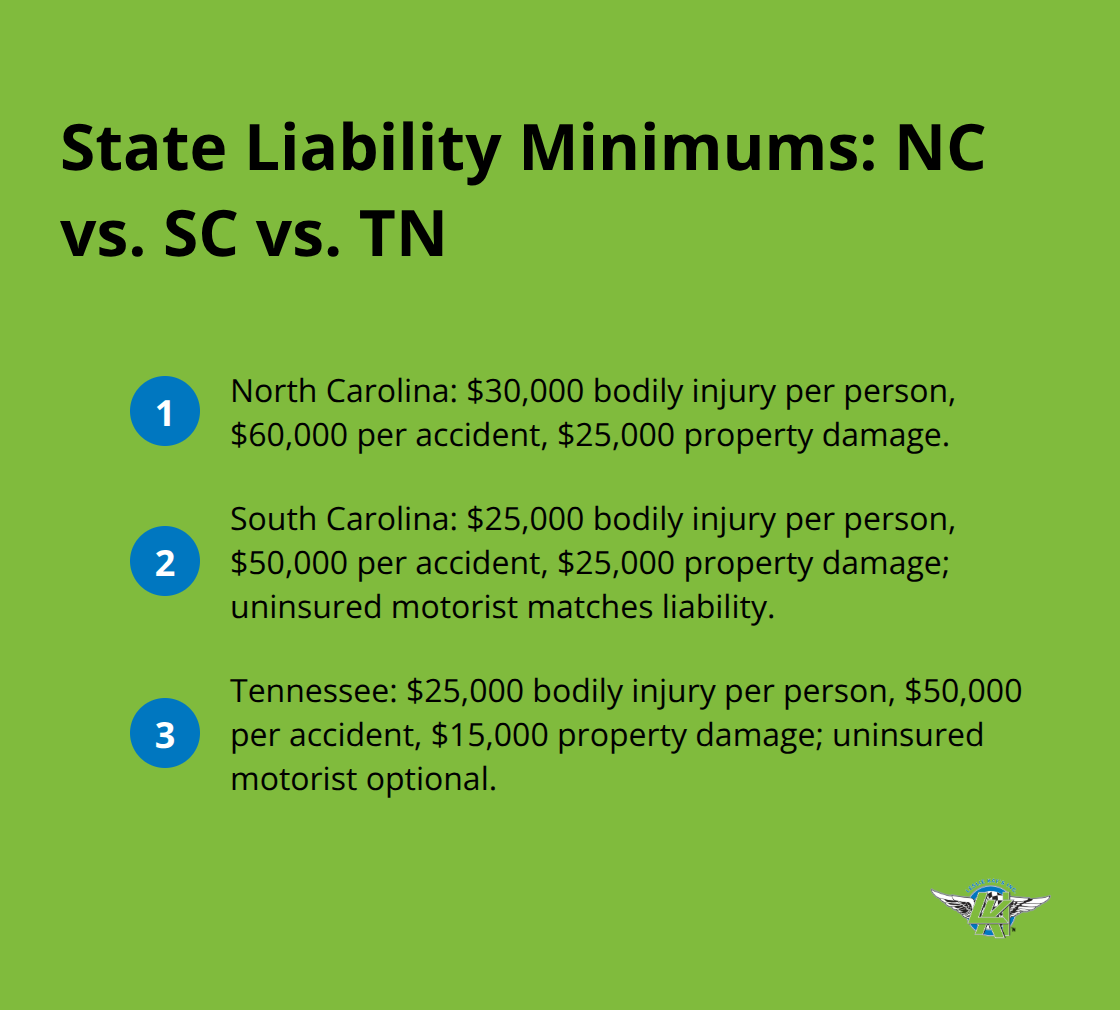

North Carolina Sets the Highest Bar

North Carolina demands the most aggressive liability minimums in the Southeast: bodily injury coverage of $30,000 per person and $60,000 per accident, plus property damage of $25,000. If you ride into NC from another state, your home policy must meet these thresholds or you face serious legal exposure. Many riders assume their home state coverage travels automatically-it doesn’t. If you’re based in South Carolina and ride into North Carolina, your SC minimums leave you $5,000 short on bodily injury per person, a gap that could cost you thousands out of pocket if you cause an accident.

South Carolina and Tennessee: Lower Minimums, Same Risk

South Carolina takes a lighter approach with bodily injury minimums of $25,000 per person and $50,000 per accident, property damage at $25,000, and uninsured motorist coverage matching your liability level. Tennessee sits in the middle at $25,000 per person bodily injury, $50,000 per accident, and $15,000 property damage, though uninsured motorist coverage remains optional. The practical solution is straightforward: adopt the highest liability limits of any state you plan to visit.

We recommend carrying at least $100,000 per person and $300,000 per accident in bodily injury liability if you cross state lines regularly, which exceeds all three states’ minimums and protects your assets in worst-case scenarios.

Registration and Permit Rules Vary Widely

Registration and permit requirements vary just as much as liability rules. North Carolina requires ATVs used on public roads to meet motorcycle-style insurance and safety standards, while private property operation often requires nothing. South Carolina mirrors this split, with recreational private use typically uninsured and road use demanding motorcycle coverage. Tennessee follows the same pattern. Before any multistate trip, contact the specific trails or parks you plan to visit-many private operations require proof of liability coverage as a condition of access, and some public lands impose their own area-specific requirements that your standard policy may not cover.

Prepare Your Documentation for Cross-State Rides

Carry a digital copy of your current insurance card, vehicle registration, and valid license on your phone to eliminate delays at checkpoints or claim time. The gap most riders miss is comprehensive and collision coverage, which protects against theft, vandalism, weather damage, and accidents on unfamiliar terrain where you’re far from home repair shops. This coverage becomes essential when you cross state lines into rugged or unfamiliar regions. As you plan your multistate adventures, understanding these coverage options becomes your next critical step.

Coverage That Travels With You Across State Lines

Liability Protection Forms Your Foundation

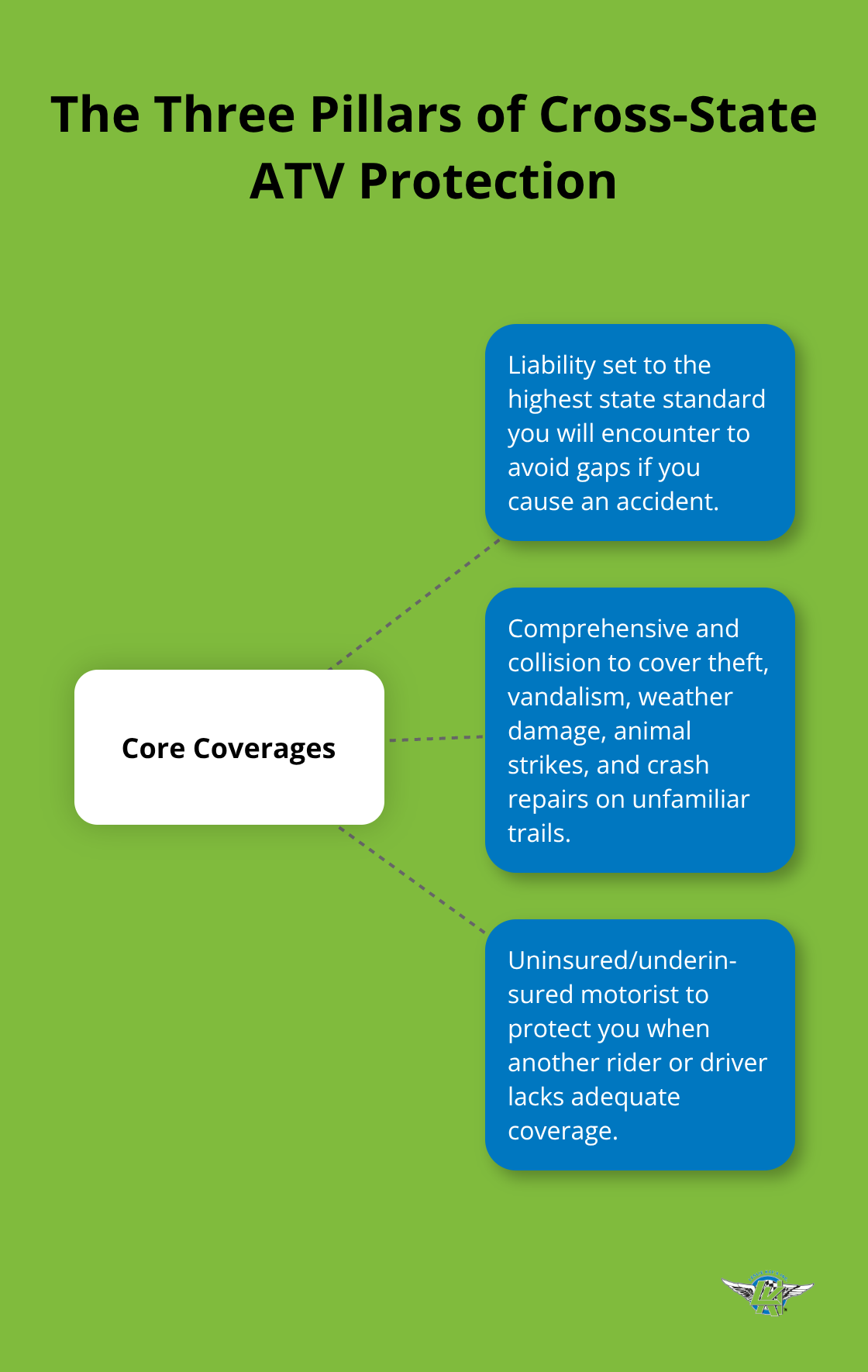

Liability protection forms your foundation, but it only works if your policy actually follows you across state lines. Many standard auto policies won’t cover off-road ATV use in other states, leaving you exposed the moment you cross a border. You need a multistate ATV policy that explicitly covers recreational off-road use in every state you plan to visit. North Carolina’s $30,000 per person bodily injury minimum should be your baseline if you ride there, but that’s only the start. If you cause an accident in North Carolina and your South Carolina policy tops out at $25,000, you’re personally liable for the $5,000 gap plus any damages beyond that threshold. The practical solution is carrying $100,000 per person and $300,000 per accident in bodily injury liability across all states you frequent. This exceeds every state’s minimum and protects your personal assets in serious accidents.

Property damage liability follows the same logic-North Carolina requires $25,000, so match or exceed that floor everywhere you ride. When you shop for multistate coverage, ask your insurer directly whether liability extends to all states where you’ll ride, not just your home state, and whether they cover trail riding specifically or only on-road use.

Comprehensive and Collision Coverage Protects Against Unfamiliar Terrain

Comprehensive and collision coverage becomes your safety net on unfamiliar terrain where repair costs spike and you’re far from trusted shops. Comprehensive covers theft, vandalism, weather damage, and animal strikes-critical protection when you store your ATV in different states or ride in remote areas. Collision pays for accident repairs regardless of fault, which matters when you hit a hidden rock or tree on an unfamiliar trail. Progressive includes automatic $3,000 coverage for aftermarket parts and upgrades, with the option to increase up to $30,000 depending on your ATV’s make and model. If you’ve invested in a winch, GPS system, or upgraded racks, document those parts with receipts and photos so your claim processes smoothly if damage occurs out of state.

Uninsured Motorist Coverage Fills Critical Gaps

Uninsured and underinsured motorist protection fills the gap when another rider or driver lacks adequate coverage. North Carolina requires this coverage, South Carolina requires uninsured motorist matching your liability limits, and Tennessee recommends it strongly. Across multistate riding, this coverage protects you if an uninsured ATV rider hits you on a trail in Tennessee or an underinsured driver causes an accident on a public road in South Carolina. These three coverage types-liability meeting the highest state standard, comprehensive and collision for damage protection, and uninsured motorist for gap coverage-form the core shield for cross-state riders. Bundle them together on a policy designed specifically for off-road use, and you eliminate the state-by-state guessing game. Your next step involves identifying which additional coverages address the specific gaps that standard policies leave exposed.

Where Standard Policies Fall Short

Off-Road Exclusions Leave You Unprotected Across State Lines

Your standard motorcycle or auto insurance won’t protect your ATV across state lines. Standard policies explicitly exclude off-road ATV use or limit coverage to your home state, leaving you unprotected the moment you cross into unfamiliar terrain. When you ride into North Carolina from South Carolina with a basic auto policy, you’re technically uninsured for trail use, even if your liability limits technically meet NC’s minimums. The insurer can deny your entire claim based on the off-road exclusion, leaving you to pay repair costs and medical bills out of pocket.

Many riders discover this gap only after an accident occurs. Trail operators and park rangers increasingly require proof of liability coverage before granting access, and standard policies won’t satisfy those requirements because they don’t explicitly cover recreational trail riding. You need a policy specifically written for ATV use across multiple states, not a generic auto or motorcycle policy. Ask your current insurer directly whether your policy covers trail riding in every state you plan to visit. If the answer is anything less than a clear yes, you have a gap that could cost thousands.

Comprehensive and Collision Coverage Restrictions Create Blind Spots

Comprehensive and collision coverage creates another critical blind spot for multistate riders. Many policies include these coverages only if you register your ATV in your home state, then restrict coverage to riding within that state or nearby regions. Once you venture into unfamiliar terrain in another state, the coverage becomes conditional or disappears entirely. Weather damage, theft from unfamiliar parking areas, and collision with hidden obstacles on remote trails all fall outside coverage if your policy wasn’t designed for cross-state adventures.

Aftermarket parts and upgrades present a separate problem. Without documentation of your parts and their cost, you cannot claim the full value after an accident in another state.

Uninsured Motorist Protection Gaps Vary by State

Uninsured motorist coverage varies dramatically across states, and many riders carry the bare minimum required in their home state, then ride in states where that minimum is inadequate. Tennessee doesn’t require uninsured motorist coverage, so a Tennessee-based rider might carry zero UM protection, then face serious financial exposure if hit by an uninsured ATV rider on a North Carolina trail. This exposure multiplies when you cross multiple state lines on a single trip.

Three Actions Close the Coverage Gaps

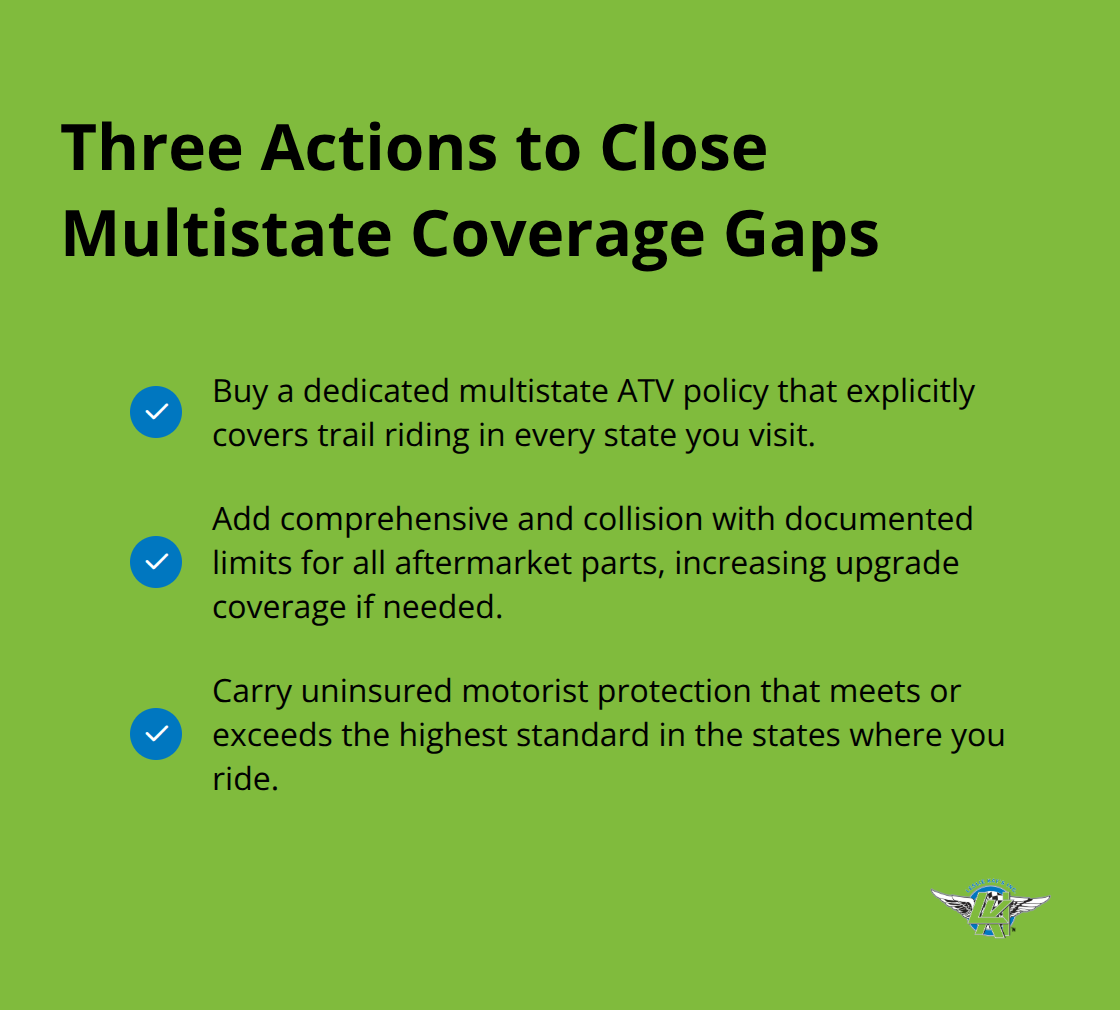

Purchase a dedicated multistate ATV policy that explicitly covers trail riding across every state you plan to visit, not a standard auto or motorcycle policy. Add comprehensive and collision coverage with documented limits for all aftermarket parts you own, increasing upgrade coverage beyond the automatic amount if necessary. Carry uninsured motorist protection matching or exceeding the highest standard in any state where you ride, regardless of your home state’s requirements. At Leslie Kay’s, we specialize in multistate ATV coverage designed specifically for riders who cross state lines, shopping multiple carriers to match your actual riding patterns and protection needs.

Final Thoughts

Multistate ATV insurance protects you where standard auto or motorcycle policies fail. Your liability limits must match the highest state standard you’ll encounter-North Carolina’s $30,000 per person bodily injury minimum sets the floor, but $100,000 per person and $300,000 per accident shields your assets far better when accidents happen on remote trails. Comprehensive and collision coverage travels across state lines only if your policy explicitly covers trail riding everywhere you ride, and uninsured motorist protection fills the gap when other riders lack adequate coverage.

When you shop for coverage, ask your insurer directly whether your policy covers trail riding in every state you plan to visit, not just on-road use in your home state. Verify that comprehensive and collision apply across state lines without restrictions tied to your home state registration, and confirm that uninsured motorist protection meets the highest standard in any state where you ride. Document all aftermarket parts with receipts and photos so claims process smoothly if damage occurs out of state.

We at Leslie Kay’s, Inc. specialize in multistate ATV insurance designed specifically for riders who cross state lines. We shop multiple carriers to match your actual riding patterns and protection needs, then provide hands-on support when claims arise far from home. Contact us with your riding plans today-we’ll build a policy that protects you everywhere your trails lead.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.